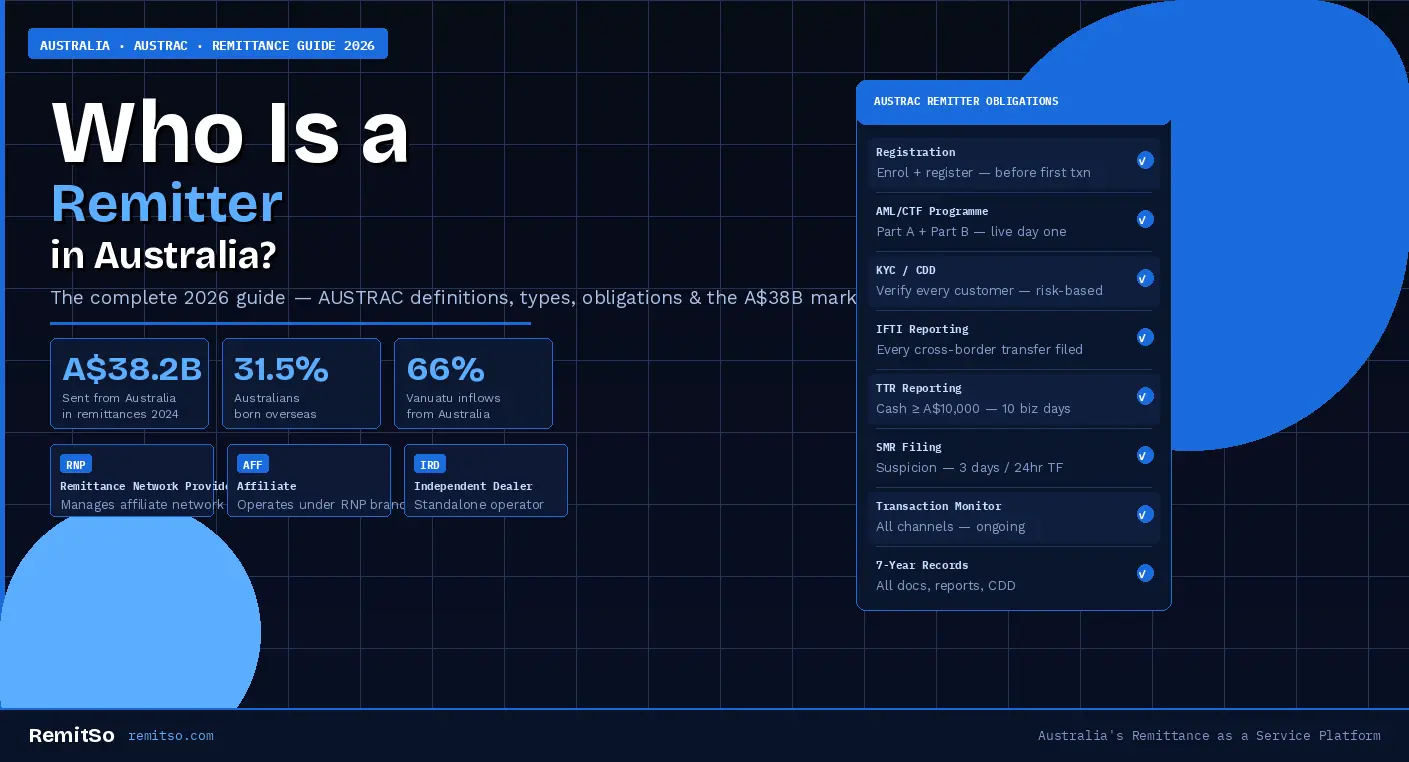

Australia is one of the world's most significant remittance-sending nations. In 2024, a record A$38.2 billion was sent from Australia to family members, communities, and economies across the globe — from A$7.3 billion flowing to India and A$5.35 billion to China, to the Pacific Island nations that depend on Australian remittances for between 35% and 66% of their total inbound transfer income. Behind every one of these transfers is a remitter. But the word "remitter" means different things in different contexts — it can refer to the individual who sends the money, to the business that processes the transfer, or to a specific category of legally registered service provider under Australia's AML/CTF regulatory framework. This guide explains all three — who remitters are, what they do, how Australia's regulatory system classifies and governs them, and what the obligations are for businesses operating in this space.

In This Article

The term "remitter" carries two distinct meanings in the Australian context, and understanding which one is being used in any given situation matters significantly — particularly for anyone operating in or entering the cross-border payments space.

In the everyday, colloquial sense, a remitter is any person who sends money to someone in another location — typically from Australia to a recipient overseas. This is the most common use of the word and covers the millions of Australians who send money to family members abroad, pay overseas suppliers, support communities in their countries of origin, or transfer funds internationally for any other personal or business purpose. In this sense, anyone who makes an international money transfer is a remitter.

In Australia's regulatory framework, however, "remitter" has a specific legal meaning. Under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act) and the rules administered by AUSTRAC, a remittance service provider — commonly referred to as a remitter — is an individual, business, or organisation that accepts instructions from customers to transfer money or property to a recipient in another location, as a service provided to others. This is the provider, not the sender. A remitter in the regulatory sense is the business or individual who operates the money transfer infrastructure through which individual senders make their transfers. This distinction matters because it determines who has legal obligations under Australian financial crime law.

Australia's remittance market is large, growing, and deeply connected to the country's demographic reality. With 31.5% of Australia's population of 27.4 million born overseas — the highest proportion since 1891 — the ties between Australian residents and their countries of origin are stronger than at any point in the nation's modern history. Those ties express themselves financially in the form of remittances, and the numbers are striking.

Figure 1: Key statistics defining Australia's remittance market in 2024–2026 — sources: World Bank, Australian Bureau of Statistics, Money Transfer Australia analysis

India receives the largest single share of Australian remittances at A$7.3 billion annually, though this represents only 3.8% of India's global inbound total — reflecting how large India's overall remittance economy is. China is the second largest recipient at A$5.35 billion, representing a far more significant 12.1% of China's total inbound remittances. The Philippines, Vietnam, and the United Kingdom complete the top five sending corridors from Australia. For Pacific Island nations — Vanuatu, Tuvalu, the Solomon Islands, and Fiji — Australian remittances represent between 35% and 66% of their total inbound transfer income, making Australia's remittance market not just economically significant domestically but critical to the financial stability of entire Pacific economies.

The World Bank and KNOMAD data that underpins these figures also confirms a longer-term trend: since 2000, remittances from Australia have grown faster than the global average, and the trajectory is expected to continue as net overseas migration remains elevated. For businesses operating as remitters in Australia — or considering entering the market — this trajectory represents a substantial and growing commercial opportunity in a regulated, transparent, and increasingly digitalised sector.

Understanding who participates in Australia's remittance market requires distinguishing between different types of participants — from individual senders to large commercial operators — and understanding how each is positioned within the regulatory framework.

Figure 2: Four types of participants in Australia's remittance market — individual senders, business senders, licensed operators, and informal operators

For businesses that operate as remittance service providers in Australia, AUSTRAC's regulatory framework recognises three distinct registration categories. Each category has different characteristics, different obligations, and a different relationship with the regulator. Understanding which category applies to a given business model is the first step in structuring a compliant Australian remittance operation.

| Category | Who They Are | Key Characteristic | Registration Renewal |

|---|---|---|---|

| Remittance Network Provider (RNP) | A business that allows affiliates to use its brand, products, platforms, or systems to provide remittance services to customers | Responsible for AML/CTF obligations on behalf of its entire affiliate network — including SMR filing unless a written agreement assigns this to the affiliate | Every 3 years — and must renew affiliates' registration simultaneously |

| Affiliate | A business with a formal agreement with an RNP — uses the RNP's brand, platform, or systems to deliver remittance services to end customers | Operates under the RNP's compliance umbrella — but may also register independently as an independent remittance dealer if providing services outside the RNP network | Every 3 years — renewal managed by the RNP on behalf of its affiliates |

| Independent Remittance Dealer (IRD) | A business that provides remittance services independently — without operating under an RNP's brand or systems | Bears the full suite of AML/CTF obligations independently — AML/CTF programme, KYC, monitoring, IFTI/TTR/SMR reporting, and recordkeeping without the support of an RNP compliance framework | Every 3 years — independently managed |

Figure 3: AUSTRAC's three registered remittance provider categories — their definitions, key characteristics, and registration renewal requirements under the AML/CTF Act

The distinction between RNP and IRD is particularly important for new operators deciding how to enter the Australian remittance market. An RNP model — where a licensed network operator supports a network of affiliates — allows individual affiliate operators to deliver remittance services to customers while leveraging the network's existing compliance infrastructure, brand, and systems. This significantly reduces the compliance burden on the affiliate compared to operating independently as an IRD. The RNP model is how most large global remittance networks — including operators using white-label technology platforms — structure their Australian operations.

Under the AML/CTF Amendment Act 2024, effective from 31 March 2026, remittance service providers must both enrol with AUSTRAC and apply for registration — and cannot commence providing services until registration is approved. AUSTRAC scrutinises registration applications and will only approve applications where it is satisfied the operator is appropriate to provide remittance services, having regard to their compliance history, beneficial ownership, and the ML/TF risks their business model presents.

Understanding why individual remitters send money is commercially important for remittance operators — it determines the corridors that matter, the amounts and frequencies typical of different customer segments, and the product features that will resonate with specific communities. It is also important for compliance purposes: a customer's stated purpose for sending money is part of the information that helps operators assess transaction risk and identify patterns that deviate from established norms.

The motivations behind Australia's A$38.2 billion in annual outbound remittances are more varied than the simple "migrants sending money home" narrative suggests. Family financial support — covering daily living expenses, healthcare, education costs, and housing for relatives overseas — remains the single largest driver, particularly among the large Indian, Chinese, Filipino, and Vietnamese diaspora communities. But the picture is considerably more nuanced across different communities and corridors.

Figure 4: Seven primary motivations behind Australian outbound remittances — each has distinct size, frequency, and corridor characteristics that inform monitoring and product design

A registered remitter in Australia — whether operating as an RNP, an affiliate, or an independent remittance dealer — bears a comprehensive set of obligations under the AML/CTF Act. These obligations are not merely administrative: they are the legal framework through which Australia prevents its cross-border payment infrastructure from being used for money laundering, terrorism financing, and other serious financial crime. AUSTRAC enforces these obligations actively, and failure to comply carries consequences ranging from civil penalties to criminal prosecution.

| Obligation | What It Requires | When It Applies |

|---|---|---|

| AUSTRAC Registration | Enrol and apply for registration with AUSTRAC before providing any remittance service. From 31 March 2026, registration must be approved before services commence. | Before first transaction |

| AML/CTF Programme | Develop and maintain a written AML/CTF programme (Part A: risk-based controls; Part B: customer identification and verification) tailored to the specific risks of the business. | Before first transaction — continuously maintained |

| Customer Due Diligence (KYC) | Verify the identity of customers before providing services. Enhanced due diligence applies for high-risk customers, PEPs, and customers from high-risk jurisdictions. | Before first transaction per customer — updated on risk triggers |

| IFTI Reporting | File an International Funds Transfer Instruction report with AUSTRAC for every cross-border electronic transfer — inbound or outbound — within 10 business days. | Every cross-border transfer — no minimum amount |

| TTR Reporting | File a Threshold Transaction Report for any cash transaction of A$10,000 or more within 10 business days. | Any cash transaction at or above A$10,000 |

| Suspicious Matter Reports (SMR) | File an SMR within 3 business days (24 hours for TF) of forming a suspicion of ML, TF, or proceeds of crime — regardless of transaction amount. | Any time suspicion is formed |

| Transaction Monitoring | Maintain ongoing, risk-based monitoring across all transaction channels and corridors — actively detecting structuring, velocity anomalies, and suspicious patterns. | Continuously — all transactions |

| Record Retention | Retain all AML/CTF records — CDD, transaction records, reports, monitoring logs — for a minimum of 7 years in an accessible format. | 7 years from transaction or relationship end |

Figure 5: Eight core obligations for registered remitters under Australia's AML/CTF framework — triggers, scope, and timing for each requirement

The pathway to becoming a legally registered remittance service provider in Australia involves a structured sequence of steps — each of which must be completed before the next can proceed, and none of which can be skipped without creating a compliance exposure. The sequence is straightforward in principle but requires careful execution in practice.

The first step is determining which AUSTRAC registration category applies to the intended business model — RNP, affiliate, or independent remittance dealer. This decision affects the compliance obligations that apply, the registration form required, and the ongoing relationship with AUSTRAC. Most new market entrants will operate either as an affiliate within an existing RNP's network (leveraging the RNP's compliance infrastructure) or as an IRD with their own standalone compliance programme.

Once the category is determined, the operator must complete AUSTRAC's online enrolment and registration application through the AUSTRAC Online portal. The application requires detailed information about the business structure, its designated services, its beneficial ownership — including all individuals who own 25% or more of the business — and its key personnel. AUSTRAC scrutinises applications against fit and proper person criteria and will only approve registration where it is satisfied the operator and its key personnel are appropriate to provide remittance services.

Before registration can be activated for operational use, the operator must also have its AML/CTF programme fully developed and ready to implement, its KYC systems operational, its IFTI and TTR reporting workflows configured, and its transaction monitoring active. These are not post-launch items — they are preconditions for operating legally. Businesses that use a purpose-built remittance platform — which includes pre-integrated reporting, monitoring, and KYC infrastructure — can complete this pre-launch compliance setup in a fraction of the time required to build each component independently.

Australia's remittance sector — for both individual senders and registered operators — faces a specific set of challenges that are distinct from those in other major remittance markets. Understanding these challenges helps both senders and operators make better decisions about how they engage with the market.

De-banking — the refusal or withdrawal of banking services by financial institutions from remittance operators — remains one of the most significant structural challenges in Australia's remittance sector. Some Australian banks have historically declined or exited banking relationships with remittance operators, citing the elevated ML/TF risk associated with the sector and the cost of the due diligence required to manage that risk. The consequence is that some registered, fully compliant remittance operators have difficulty obtaining or maintaining the bank accounts essential for their operations. Australia's Council of Financial Regulators, AUSTRAC, the ACCC, and the Attorney-General's Department published joint recommendations in 2022 to address de-banking — including enhanced transparency requirements for banks that exit remittance relationships — but the issue has not been fully resolved. For new operators, securing banking relationships requires a demonstrably strong compliance programme, documented AUSTRAC registration, and transparent beneficial ownership information presented clearly to prospective banking partners.

The global average cost of sending remittances remains above the 3% target set by the United Nations Sustainable Development Goal 10.c.1, standing at approximately 6.4% per USD $200 sent as of late 2023. For Australian senders — many of whom send to Pacific Island nations and lower-income Asian economies — high transfer costs directly reduce the amount received by beneficiaries. Banks typically charge more than specialist remittance providers, both in explicit fees and in exchange rate margins. The Australian Competition and Consumer Commission has noted that Australian remittance consumers are more price-sensitive than the global average, and the competitive pressure from digital-native remittance operators has driven meaningful cost reductions on major corridors over the past decade.

Whether you are an individual looking to understand how remittances work, or a business planning to launch or scale a remittance operation in Australia, the regulatory and operational environment is more demanding in 2026 than at any previous point. AUSTRAC's registration requirements have strengthened, compliance expectations have risen, and the competitive landscape has been reshaped by digital-first operators who have invested heavily in technology and compliance infrastructure simultaneously.

RemitSo's Remittance as a Service platform for Australia is built specifically for registered remitters and aspiring market entrants who need to operate at speed and at scale without building the full compliance and payments stack from scratch. RemitSo provides the technology infrastructure — AUSTRAC-ready IFTI reporting, KYC and CDD tooling, transaction monitoring, sanctions screening, and audit documentation — alongside the white-label front-end that allows operators to deliver a branded, digital remittance experience to their customers. For banks, neo-banks, fintechs, MSBs, credit unions, and exchange houses entering or expanding in Australia's remittance market, RemitSo's platform is the foundation on which compliant, scalable operations are built.

Under AUSTRAC's regulatory framework, a remitter — formally called a remittance service provider — is an individual, business, or organisation that accepts instructions from customers to transfer money or property to a recipient in another location. This definition covers businesses that operate remittance services for others — not individuals who send money for their own personal purposes. Remittance service providers must be registered with AUSTRAC before providing any remittance services in Australia, and must maintain an AML/CTF programme, conduct customer due diligence, file IFTI and TTR reports, and comply with the full suite of AML/CTF Act obligations. AUSTRAC maintains a public Remittance Sector Register of all registered remittance service providers, which can be searched by the public to verify whether a provider is legitimately registered.

No — if you are an individual sending money overseas for personal purposes, you do not need to register with AUSTRAC. The AUSTRAC registration requirement applies to businesses and individuals who provide remittance services to others as a service — accepting instructions from customers and transferring their money internationally. As an individual sender, you use a registered provider (a bank, digital remittance platform, or specialist money transfer operator) that is already registered with AUSTRAC and bears the compliance obligations on your behalf. You will be subject to that provider's KYC identity verification requirements, and may be asked for documentation about the source and purpose of larger or unusual transfers — but these requests come from your provider's compliance obligations, not from any registration requirement that applies to you personally.

A Remittance Network Provider (RNP) is a business that allows other businesses (its affiliates) to use its brand, systems, or platforms to deliver remittance services to customers. The RNP is responsible for the AML/CTF compliance obligations of its entire affiliate network — including ensuring affiliates meet their KYC, monitoring, and reporting obligations, and filing SMRs on behalf of affiliates unless a written agreement specifies otherwise. An Independent Remittance Dealer (IRD), by contrast, provides remittance services independently — without operating under an RNP's brand or systems. An IRD must bear the full suite of AML/CTF obligations on its own, including maintaining its own AML/CTF programme, KYC systems, and reporting workflows. The RNP model is generally better suited to businesses that want to enter the remittance market quickly with lower compliance infrastructure investment, while the IRD model suits operators with distinct brands and the capacity to manage full compliance independently.

Australia sent a record A$38.2 billion in overseas remittances in 2024, according to analysis by Money Transfer Australia drawing on World Bank, ABS, KNOMAD, and DFAT data. India was the largest single recipient at A$7.3 billion, followed by China at A$5.35 billion. The Philippines, Vietnam, and the United Kingdom complete the top five destination corridors. Pacific Island nations are disproportionately dependent on Australian remittances — Vanuatu receives approximately 66% of its total remittance inflows from Australia, with Tuvalu, the Solomon Islands, and Fiji also receiving between 35% and 49% of their total inflows from Australian senders. The volume is expected to grow further in 2025 and 2026 as Australia's overseas-born population — which reached 8.6 million or 31.5% of the total population in 2024 — continues to increase through sustained high net overseas migration.

AUSTRAC maintains a publicly accessible Remittance Sector Register on its website. You can search the register by the provider's legal name, trading name, or ABN/ACN to confirm whether they are registered as a remittance service provider in Australia. The register shows the provider's legal name, trading names, registration status, and registered address. If a provider appears on the register without any conditions noted, they are registered and authorised to provide remittance services. If you see an exclamation mark in a yellow circle against a provider's entry, that indicates conditions have been imposed on their registration — which may limit the services they can provide. Using a provider that is not on the Remittance Sector Register is a significant consumer risk — unregistered providers have no compliance obligations and offer no consumer protection.

Providing remittance services in Australia without AUSTRAC registration is a criminal offence under the AML/CTF Act. Consequences include civil penalties calculated per contravention — which can accumulate rapidly given that each transaction can constitute a separate breach — criminal prosecution with custodial sentences of up to ten years for serious offences, forced business shutdown through cease-and-desist orders, and loss of banking access when financial institutions identify the unlicensed status. AUSTRAC actively detects unregistered operators through IFTI data analysis, bank referrals, ATO data sharing, and law enforcement intelligence. Once enforcement action begins, obtaining registration subsequently becomes significantly more difficult, as AUSTRAC applies enhanced scrutiny to applications from operators with a prior non-compliance history.

The total cost of an international transfer from Australia depends on two components: the explicit fee charged by the provider and the exchange rate margin applied above the interbank (mid-market) rate. Banks typically have lower explicit fees on some transfers but apply exchange rate margins of 2–4% above the interbank rate — which on a A$5,000 transfer represents A$100–$200 in hidden cost that does not appear as a line-item fee. Specialist digital remittance operators generally offer exchange rates closer to the interbank rate and charge lower or zero explicit fees, making them cheaper for most transfer sizes on major corridors. The ACCC has noted that Australian consumers who compare the total cost of transfer — fee plus rate — rather than comparing fees alone consistently get better value from specialist providers. All registered providers — whether banks or specialists — are subject to the same AUSTRAC reporting obligations, so the compliance protection to the sender is equivalent regardless of which channel is used.

De-banking refers to the refusal or withdrawal of banking services — including transaction accounts, merchant services, and payment processing — by financial institutions from remittance operators. Australian banks are themselves subject to AML/CTF obligations and conduct their own due diligence on business customers. When a bank assesses that the compliance risk of maintaining a remittance operator's account is too high relative to the commercial benefit, it may exit the relationship. The consequences for the remittance operator are severe — without bank accounts, transfers cannot be received; without payment processing, digital transactions cannot be executed; without correspondent banking, international settlements cannot be made. Australia's Council of Financial Regulators, AUSTRAC, the ACCC, and the Attorney-General's Department published joint recommendations in 2022 to improve transparency and fairness in de-banking decisions. For remittance operators, the most effective protection against de-banking is a demonstrably strong compliance programme, documented AUSTRAC registration, transparent beneficial ownership, and a proactive relationship with their banking partners.