In today's digital economy, every payment, transfer, booking, or purchase relies on a transaction processing system. Whether it is a retail checkout, a cross-border remittance, or an online subscription renewal, transactions must be processed accurately, securely, and in real time. A transaction processing system is the operational backbone of modern organisations — without it, businesses cannot process payments reliably, update customer data, manage inventory, maintain financial accuracy, or scale digital operations. As global commerce expands and online transaction processing becomes the standard, understanding how TPS systems work is no longer optional. It is strategic.

In This Article

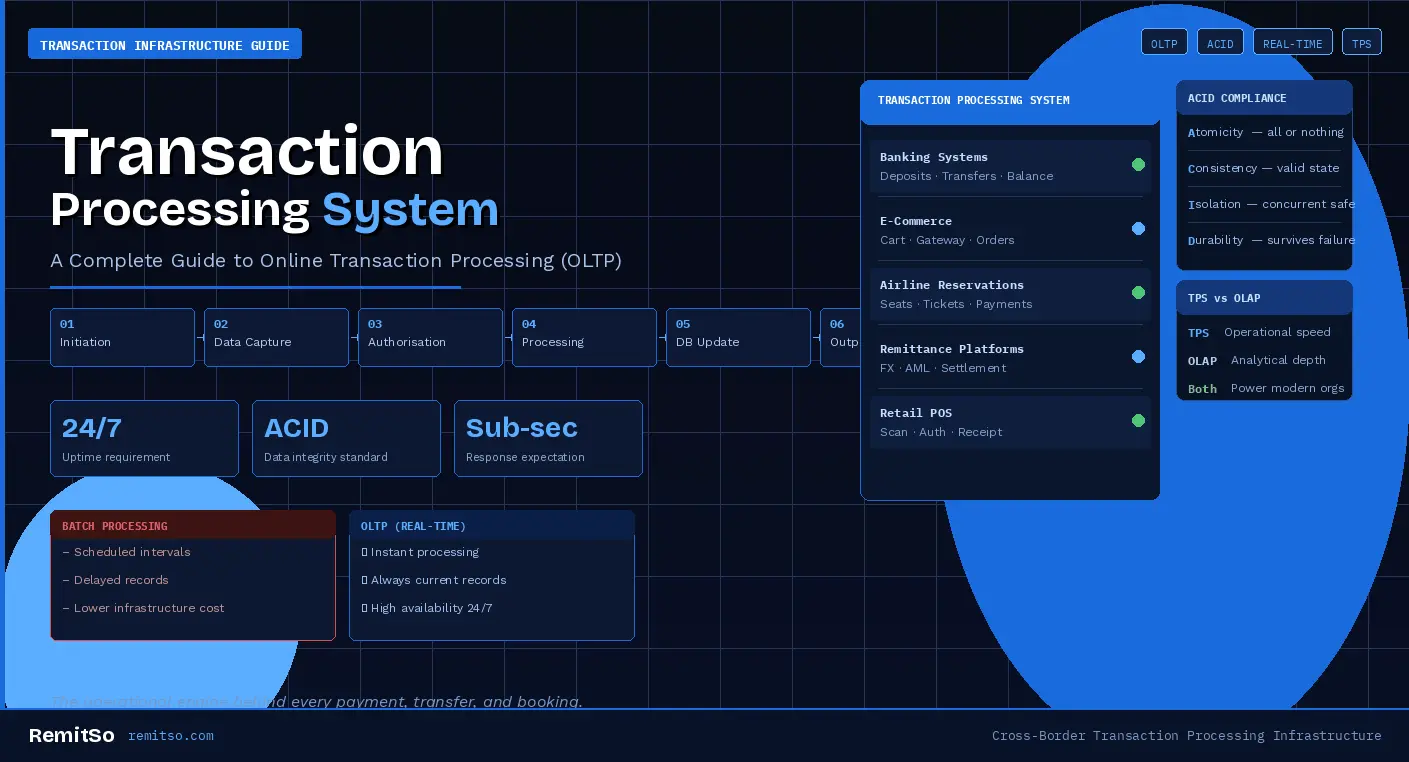

A transaction processing system (TPS) is a specialised information system that captures, validates, processes, and stores transactional data generated by business activities. In simple terms, a TPS ensures that every business transaction is recorded accurately, processed correctly, and stored securely. It operates at the core operational level of an organisation and directly supports day-to-day business functions — from retail checkouts and bank transfers to airline bookings and cross-border remittances.

The process of transaction processing system operations typically follows a consistent sequence: data entry, where transaction information is captured; validation, where accuracy and completeness are verified; processing, where calculations are performed and records are updated; storage, where data is saved permanently to a database; and output generation, where receipts, confirmations, and reports are produced. Each stage depends on the completion of the previous one — errors or failures at any point in the sequence can propagate downstream, which is why reliability and fault tolerance are foundational requirements of every TPS architecture.

Online Transaction Processing (OLTP) refers to real-time transaction processing where data is handled immediately as the transaction occurs. Unlike batch processing — where transactions are collected over a period and processed together at a scheduled interval — OLTP systems process transactions instantly, support high volumes of simultaneous users, maintain data consistency across concurrent operations, and ensure rapid response times that users expect from modern digital services.

An online transaction processing system is essential for e-commerce platforms, banking systems, remittance platforms, payment gateways, and airline booking systems. OLTP systems are designed around three defining characteristics: speed, concurrency, and data integrity. Speed ensures that transactions complete within milliseconds. Concurrency ensures that multiple users can transact simultaneously without one operation corrupting another. Data integrity ensures that the database always reflects a consistent, accurate state — even when failures occur mid-transaction.

Figure 1: Batch processing vs online transaction processing — the operational and architectural differences

The primary function of a transaction processing system is to maintain operational stability while ensuring data accuracy across every transaction the organisation processes. A TPS achieves this through five interconnected functions that together form the complete transaction lifecycle.

The system captures transaction details including customer identity, payment amount, product or service details, date and time, and authorisation status. The quality of data captured at this stage determines the accuracy of every subsequent operation. Modern OLTP systems capture data automatically through digital interfaces — payment terminals, web forms, API integrations — reducing the manual input errors that characterised earlier transaction systems.

Before processing proceeds, the TPS verifies the transaction against a set of business rules: confirming sufficient account balance, validating payment credentials, checking inventory availability, and verifying compliance requirements. Validation is the system's primary error prevention mechanism — catching problems before they create incorrect records that must be reversed or reconciled later.

The processing engine performs the calculations and operations that constitute the transaction: tax computation, currency conversion, fee application, and balance updates. In cross-border payment systems, this stage also includes sanctions screening, AML rule application, and routing logic — the compliance layer that separates a regulated financial TPS from a simple data management system.

Each transaction is securely stored for audit purposes, regulatory compliance, reporting and analytics, and dispute resolution. The storage architecture must guarantee durability — meaning that once a transaction is committed to the database, it cannot be lost even if a system failure occurs immediately afterwards. This guarantee is typically implemented through transaction logs and write-ahead logging mechanisms that allow complete recovery from any point of failure.

The final function produces outputs that confirm the transaction to the parties involved: receipts, payment confirmations, updated account statements, and operational reports. For regulated financial operators, output generation also includes the regulatory reports — suspicious matter reports, threshold transaction reports, and period-end submissions — that satisfy the reporting obligations of the jurisdictions in which the business operates.

Transaction processing systems are broadly classified into two types, distinguished by their approach to timing — whether transactions are handled immediately as they arise or collected and processed together at intervals.

Figure 2: The two primary classifications of transaction processing systems

Batch processing systems collect transactions over time and process them together at scheduled intervals. This approach is cost-efficient and appropriate for use cases where real-time confirmation is not required — payroll processing, utility billing, and end-of-day banking settlements are classic examples. The trade-off is that the database does not reflect the current state of the business at any given moment during the batch window.

Real-time processing systems process each transaction instantly at the moment it occurs. ATM withdrawals, card payments, online purchases, and remittance transfers are all real-time TPS operations — the customer receives a confirmation, and the database is updated, within seconds of the transaction being initiated. Real-time systems require high availability, strong fault tolerance, and the ability to handle concurrent transactions without data conflicts — technical requirements that make them more complex and costly to build and operate than batch systems.

Understanding transaction processing system examples across different industries illustrates the breadth of contexts in which TPS architecture delivers operational value — and the consistent underlying requirements that apply regardless of industry vertical.

| Industry | TPS Application | Core TPS Functions Used |

|---|---|---|

| Retail — POS | Barcode scanning, payment authorisation, receipt generation | Validation, processing logic, inventory update, output |

| Banking | Deposits, withdrawals, fund transfers, balance updates | All five core functions — compliance-grade storage required |

| Airline Reservations | Seat booking, ticket issuance, payment confirmation | Real-time concurrency — seat availability must be locked atomically |

| E-Commerce | Cart processing, payment gateway integration, order management | High-volume OLTP with fraud screening and inventory management |

| Remittance Platforms | Cross-border transfers, currency conversion, compliance checks, settlement tracking | Full lifecycle — AML, FX, payout routing, regulatory reporting |

Figure 3: Transaction processing system examples across industries — and the core TPS functions each relies upon

Remittance platforms represent one of the most demanding TPS environments because they combine the real-time settlement requirements of consumer payments with the multi-currency complexity of FX processing, the compliance obligations of regulated financial services, and the cross-border routing challenges of international payout networks. A remittance TPS must perform sanctions screening, AML rule evaluation, currency conversion, payout partner routing, and settlement confirmation — all within a single end-to-end transaction flow that the customer expects to complete in seconds.

As global digital transactions grow, TPS systems must handle increasingly demanding requirements: high transaction volumes that test infrastructure at scale, multi-currency processing that requires real-time FX rate management, cross-border compliance that varies by jurisdiction and corridor, fraud detection that operates in real time without blocking legitimate transactions, and real-time settlement that satisfies customer expectations shaped by instant digital experiences.

Figure 4: Three non-negotiable requirements of modern transaction processing system infrastructure in the digital economy

The business case for investing in robust TPS infrastructure extends beyond technical capability. The operational and commercial benefits of a well-designed transaction processing system are measurable and directly linked to the financial outcomes that matter most to digital businesses: efficiency, accuracy, compliance, and customer trust.

Figure 5: Six key operational and commercial benefits delivered by a well-designed transaction processing system

The process of transaction processing system operations follows a structured sequence that transforms a customer action — a payment, a transfer, a booking — into a permanent, auditable record. Understanding this flow is essential for anyone building, evaluating, or operating a digital financial platform.

Figure 6: Six-step transaction processing flow in an OLTP system — from customer-initiated event to permanent record and confirmation

Transaction processing systems are frequently confused with analytical systems, but they serve fundamentally different purposes. Online Analytical Processing (OLAP) systems are designed to analyse large volumes of historical data to support strategic decision-making — generating business intelligence, trend analysis, and management reporting. TPS and OLTP systems, by contrast, are designed to process current operational transactions with speed and accuracy.

| Feature | TPS / OLTP | OLAP |

|---|---|---|

| Primary Purpose | Process transactions — operational accuracy | Analyse data — strategic insight |

| Processing Speed | Real-time, sub-second response | Slower — complex queries across large datasets |

| Data Type | Current operational data — live state | Historical aggregated data — trend analysis |

| Primary Users | Front-line staff, customers, automated systems | Analysts, finance teams, management |

| Data Operations | Insert, update, delete — high frequency | Read-heavy queries — low update frequency |

Figure 7: TPS/OLTP vs OLAP — purpose, speed, data type, and user comparison

In practice, mature digital businesses operate both systems. The TPS handles the operational transaction flow — ensuring that every payment, transfer, and booking is processed correctly in real time. The OLAP system draws on the historical transaction data stored by the TPS to generate the business intelligence that informs strategic decisions. The two systems are complementary rather than competing — but they must not be conflated, as the architectural requirements of each are fundamentally different.

A transaction information system operating in a financial services context must address a comprehensive set of security and risk requirements. Data encryption protects transaction data in transit and at rest, ensuring that sensitive financial information cannot be intercepted or accessed by unauthorised parties. Access control restricts which users and systems can initiate, approve, or view transactions — implementing the principle of least privilege across every operational role.

Fraud monitoring applies real-time rules to detect and flag suspicious transaction patterns — velocity checks, unusual amounts, atypical geographic patterns — before they complete and cause financial loss. Disaster recovery ensures that the TPS can restore to a consistent, accurate state following any failure — whether hardware, software, or infrastructure — without data loss or corruption. Cybersecurity frameworks from institutions such as NIST provide the technical standards against which financial TPS infrastructure should be designed and periodically tested.

A transaction processing system is not merely a software application. It is the operational engine of digital business. From online transaction processing in e-commerce to cross-border remittance platforms, TPS systems ensure the speed, accuracy, reliability, security, and compliance that digital organisations and their customers depend on. As digital payments expand globally, businesses must invest in scalable, secure, and automated transaction infrastructure that can meet the demands of growing volume, increasing regulatory expectations, and evolving customer requirements simultaneously.

If you are building or scaling a cross-border payment or remittance operation, RemitSo's platform is designed to streamline transaction processing, improve operational visibility, and manage complex cross-border workflows within a secure, scalable infrastructure. Rather than requiring businesses to build TPS architecture from scratch — with all the engineering effort, compliance integration, and ongoing maintenance that entails — RemitSo provides pre-built transaction lifecycle management, compliance controls, and multi-currency processing as an integrated operational layer that operators can deploy and scale rapidly.

A transaction processing system (TPS) is a specialised information system that captures, validates, processes, and stores transactional data generated by business activities. It ensures that every business transaction — whether a payment, booking, transfer, or purchase — is recorded accurately, processed correctly, and stored securely. TPS systems operate at the core operational level of an organisation, directly supporting day-to-day business functions. They are the operational backbone of digital commerce, banking, remittance platforms, and any other business that processes transactions at volume.

Online transaction processing (OLTP) refers to real-time transaction handling where data is processed immediately as the transaction occurs — as opposed to batch processing, where transactions are collected and processed at intervals. OLTP systems are defined by three characteristics: speed, meaning transactions complete in sub-second timeframes; concurrency, meaning multiple users can transact simultaneously without data conflicts; and data integrity, meaning the database always reflects a consistent, accurate state. OLTP systems are essential for e-commerce platforms, banking systems, payment gateways, remittance platforms, and any digital service where customers expect immediate transaction confirmation.

The primary function of a transaction processing system is to maintain operational stability while ensuring data accuracy across every transaction the organisation processes. This is achieved through five interconnected functions: data collection and input, which captures the transaction details; data validation, which verifies accuracy and compliance before processing proceeds; processing logic, which performs the calculations and operations that constitute the transaction; data storage, which commits the completed transaction to permanent, durable records; and output generation, which produces confirmations, receipts, and reports for users and regulatory purposes. Together these functions ensure operational continuity and financial accuracy at scale.

Transaction processing system examples span virtually every industry that handles commercial activity at volume. Retail point-of-sale systems process barcode scans, payment authorisations, inventory updates, and receipt generation in real time. Banking systems handle deposits, withdrawals, fund transfers, and balance updates. Airline reservation systems manage seat bookings, ticket issuance, and payment confirmation with strict concurrency requirements. E-commerce platforms process shopping cart operations, payment gateway integrations, and order management. Remittance platforms — among the most complex TPS environments — handle cross-border transfers, currency conversion, AML compliance checks, payout partner routing, and settlement tracking within a single end-to-end transaction flow.

The process of a transaction processing system follows six sequential stages. Transaction initiation occurs when a customer or system triggers an event. Data capture collects all relevant transaction information via API, terminal, or web interface. Authorisation check validates the transaction against business rules, compliance requirements, and balance conditions — only transactions passing all checks proceed. Processing engine execution performs calculations, applies fees, converts currencies, and updates records atomically. Database update commits the completed transaction to permanent storage, ensuring durability. Confirmation output delivers receipts and acknowledgements to users while writing internal logs and triggering any required regulatory notifications.

TPS and OLTP systems process current operational transactions with speed and accuracy — they handle the day-to-day business activity that keeps the organisation running. OLAP systems analyse large volumes of historical data to support strategic decision-making — they generate business intelligence, trend analysis, and management reporting. The two systems serve complementary roles: the TPS creates and stores the operational transaction record, while OLAP analyses that record to extract strategic insight. Their architectures are fundamentally different: TPS systems are optimised for fast, concurrent read-write operations on current data; OLAP systems are optimised for complex analytical queries across historical aggregates.

ACID stands for Atomicity, Consistency, Isolation, and Durability — the four database properties that every financial transaction processing system must satisfy to guarantee data integrity. Atomicity means a transaction either completes entirely or is rolled back entirely — there is no partial completion. Consistency means every transaction brings the database from one valid state to another — no transaction can violate the defined business rules. Isolation means concurrent transactions execute as if they were sequential — each transaction sees a consistent view of the database regardless of other transactions in progress. Durability means once a transaction is committed, it is permanently stored and survives any subsequent system failure.

TPS systems are important for online businesses because they enable the fast, secure, and accurate handling of high transaction volumes that digital commerce and financial services require. Without a robust TPS, an online business cannot process payments reliably, update customer data accurately, manage inventory in real time, or maintain the financial accuracy that regulatory compliance requires. As digital transaction volumes grow, the TPS becomes increasingly central to operational continuity — any degradation in TPS performance translates directly into failed transactions, damaged customer trust, and regulatory exposure. The more digital an organisation becomes, the more critical its TPS infrastructure becomes to its commercial and compliance outcomes.