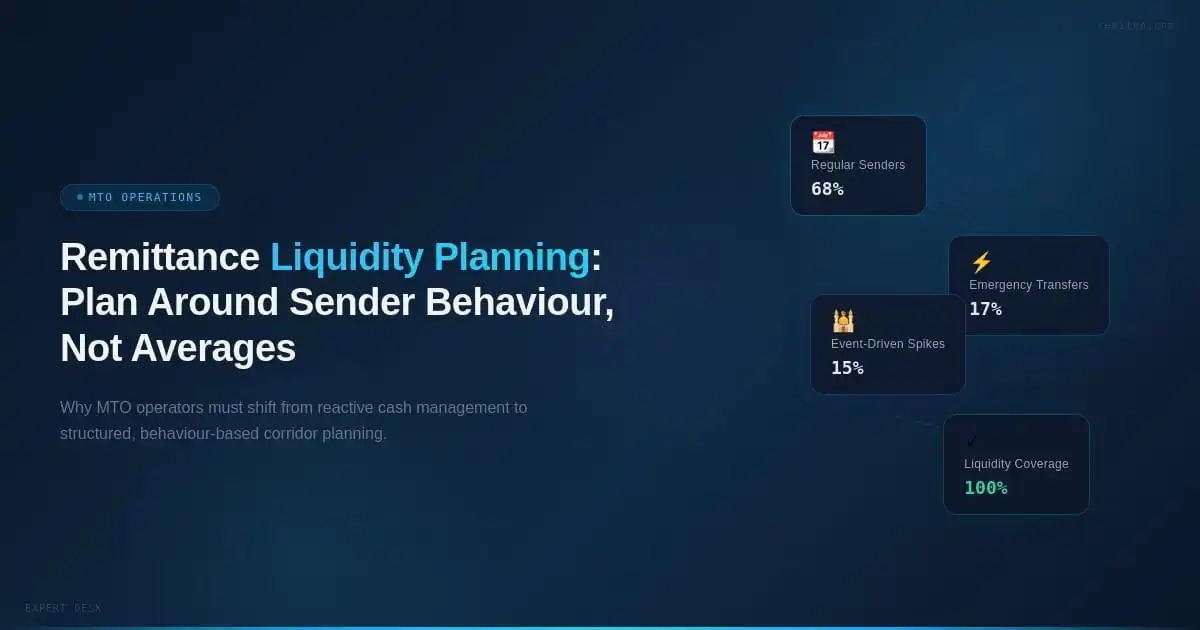

Every modern financial operation — whether payments, cross-border transfers, marketplaces, or digital financial services — relies on one critical backbone: the transaction lifecycle. As transaction volumes increase and regulatory expectations tighten, manual or semi-automated workflows become a hidden liability. Delays, reconciliation gaps, inconsistent compliance checks, and rising operational costs all stem from fragmented transaction handling. Automating the transaction lifecycle is no longer about speed alone. It is about control, resilience, trust, and long-term scalability. Organisations that adopt end-to-end automation early are better equipped to handle growth, regulatory scrutiny, and customer expectations in a global digital economy.

In This Article

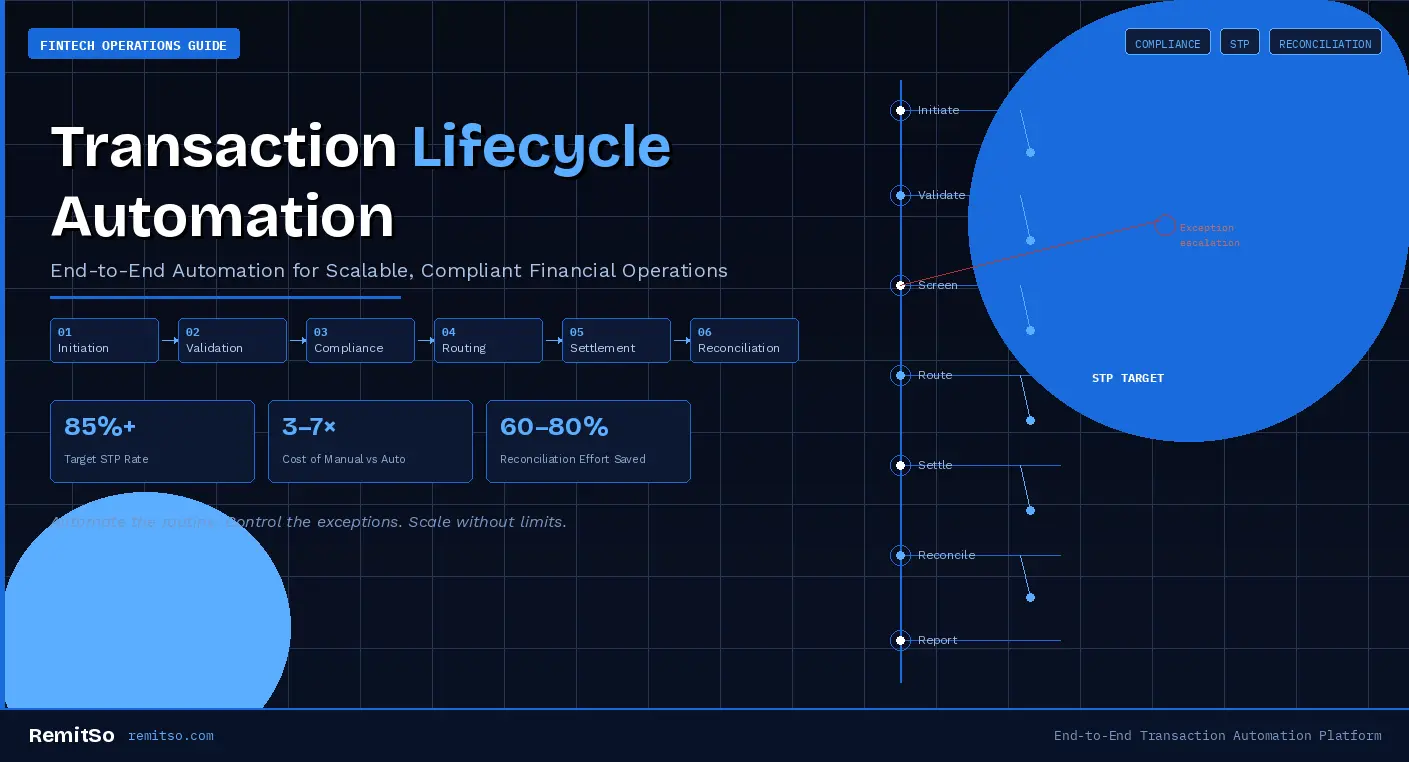

Transaction lifecycle automation is the use of rule-based digital systems to manage every stage of a transaction — from initiation and validation to settlement and reconciliation — without manual intervention, except for defined exceptions. In practice, it replaces disconnected processes with a single, intelligent flow governed by predefined logic and real-time data.

This definition matters because the scope of "automation" is frequently misunderstood. Many organisations consider themselves automated simply because they use software to process transactions. True transaction lifecycle automation is end-to-end: every stage from the moment a customer initiates a transfer to the moment funds are reconciled in the ledger is handled by the system without a human touching it — unless the system has been specifically configured to escalate an exception. Partial automation, where some stages are managed by software and others require manual handoff, still creates the friction, delay, and error risk that full automation is designed to eliminate.

Before automation can be effective, it is important to understand the full scope of the transaction lifecycle. Each stage depends on the accuracy and completion of the previous one. When handled manually or across siloed systems, even minor errors at one stage cascade into operational and regulatory issues several stages later — by which point they are far more expensive to resolve.

Figure 1: The six sequential stages of the transaction lifecycle — each depends on accurate completion of the previous

Manual transaction handling fails at scale because it introduces human error, delays approvals, weakens audit trails, and increases compliance risk — making operations expensive and unreliable as transaction volumes grow. This is not a failure of people or effort. It is a structural incompatibility between human-speed processing and the volume, speed, and complexity that modern financial operations require.

Global financial institutions, including the IMF and World Bank, consistently emphasise the importance of automation and standardised processes to reduce systemic operational risk. Their frameworks for payment system oversight explicitly identify manual intervention as a risk multiplier — particularly in cross-border and multi-currency environments where the consequences of processing errors extend across jurisdictions and regulatory boundaries.

Figure 2: Four structural failure modes of manual transaction handling that end-to-end automation systematically eliminates

Straight-Through Processing (STP) refers to transactions moving from initiation to completion without manual touchpoints — unless predefined exceptions are triggered. It is the operational gold standard for transaction-based financial businesses, and the metric that most directly reflects the maturity and efficiency of an operator's automation infrastructure.

True STP requires four foundational capabilities: centralised data, so every system in the lifecycle works from the same transaction record; rule-based decisioning, so every routing, approval, and compliance determination is made by the system according to pre-configured logic; automated validations, so data quality and format compliance are enforced at entry rather than discovered at settlement; and integrated settlement logic, so the completion of processing triggers settlement automatically without a manual release step.

Figure 3: The operational difference between partial automation and true straight-through processing

Automated transaction initiation ensures that data is captured once, validated instantly, and reused throughout the lifecycle — reducing errors and eliminating repetitive manual entry. Transactions can be initiated via web portals, mobile applications, or APIs and partner integrations. Customer and transaction data is stored centrally, forming a single source of truth that every subsequent stage reads from — ensuring that information used for compliance screening, routing, settlement, and reconciliation is identical to the data captured at initiation.

Once initiated, transactions are automatically validated against format and completeness checks, business rules, and threshold limits. This ensures only valid transactions proceed further, reducing downstream failures. Automated authorisation frameworks also support tiered approvals, customer segmentation rules, and platform-specific logic — so that validation applied to a high-value transfer is appropriately different from that applied to a standard consumer transaction, without requiring any manual differentiation by operations staff.

Automated risk and compliance controls apply consistent, rule-based checks across every transaction — ensuring regulatory adherence while allowing legitimate transactions to proceed without delay. Modern systems enforce KYC and customer risk profiling, AML transaction monitoring, sanctions and watchlist screening, and velocity and behaviour analysis. This approach aligns with global regulatory guidance from institutions such as the UN and IMF, which promote risk-based, proportionate controls as the standard for responsible payment system design.

After validation, transactions move automatically into processing. Automation enables dynamic routing based on currency, corridor, or payment method — selecting the optimal processing path and applying failover handling for disruptions. By removing manual routing decisions, organisations reduce delays and improve success rates. In cross-border contexts, intelligent routing is particularly valuable: the system evaluates available payout partners, their current success rates, and cost structures in real time, selecting the optimal route without human intervention.

Automated settlement ensures transactions are completed as soon as predefined conditions are met — reducing delays and improving predictability for both businesses and end users. Settlement logic can define instant versus batch execution parameters, conditional release rules, and retry and fallback mechanisms. Real-time status updates improve transparency across operations teams and customer-facing channels simultaneously — eliminating the status enquiry calls and manual tracking that consume significant operations capacity in less automated environments.

Reconciliation is one of the most operationally intensive stages when handled manually. Automation enables real-time matching across systems, exception-based investigation rather than line-by-line review, and automated ledger updates. Detailed audit logs support internal reviews and regulatory reporting — reducing audit preparation time significantly and providing the immutable, timestamp-anchored transaction records that regulators increasingly require as evidence of operational control.

The operational benefits of transaction lifecycle automation are measurable improvements in the metrics that determine whether a financial operation is viable at scale. Automation simultaneously addresses efficiency, accuracy, cost, compliance, and visibility — five dimensions that manual operations consistently trade off against each other as volume grows.

Figure 4: Key operational metrics improved by transaction lifecycle automation — industry benchmarks

Beyond the quantitative metrics, automation creates a qualitative shift in how operations teams work. Rather than processing individual transactions, staff focus on exception management, partner relationship oversight, and strategic improvements to the automation logic itself. This is not a reduction in the value of human judgement — it is a reallocation of that judgement to the decisions where it creates the most value.

One of the most critical advantages of transaction automation is non-linear scalability. With manual systems, growth requires proportional increases in staff — adding headcount to handle additional transaction volume. With automated systems, volume increases with minimal operational impact. The system processes 10,000 transactions with the same infrastructure it uses to process 1,000. This non-linear relationship between volume and operational cost is the foundational economics of scalable financial operations.

This scalability is essential for businesses operating across multiple markets, currencies, or regulatory environments. Each additional corridor or jurisdiction a manual operator enters requires additional compliance expertise, additional reconciliation capacity, and additional operational management. An automated operator adds a corridor primarily through configuration — updating rules, adding payout partner integrations, and adjusting compliance parameters — rather than through headcount growth.

Figure 5: Five-step framework for building a scalable automated transaction operation

A common concern about transaction automation is that removing human review reduces control. In practice, the opposite is true. Automation does not reduce control — it strengthens it, by making control systematic, consistent, and auditable rather than dependent on individual attention and judgement.

Modern automated platforms are designed with role-based access controls that restrict what each user can see and do within the system. Immutable audit trails record every transaction event, every rule applied, and every exception triggered — creating a permanent record that satisfies both internal governance requirements and external regulatory examination. Security best practices outlined by NIST emphasise controlled automation as a key pillar of resilient financial systems — explicitly noting that well-designed automation reduces the attack surface associated with human error and privilege abuse.

| Security Layer | Manual System | Automated Platform |

|---|---|---|

| Access Control | Inconsistent — relies on individual discipline | Enforced — role-based, system-controlled |

| Audit Trail | Incomplete — dependent on manual logging | Immutable — every action timestamped and recorded |

| Compliance Consistency | Variable — depends on staff knowledge and capacity | Uniform — same rules applied to every transaction |

| Fraud Detection | Reactive — identified after the fact | Proactive — velocity and behaviour rules in real time |

| Disaster Recovery | Fragile — dependent on staff availability | Resilient — redundancy and failover by design |

Figure 6: Security and control comparison between manual transaction systems and automated platforms

Three misconceptions consistently slow adoption of transaction lifecycle automation — particularly among operators who have built their businesses on manual or semi-manual processes and are concerned about what full automation means for their operations and their teams.

The first misconception is that automation removes human oversight. In reality, it shifts humans to exception handling and strategic decision-making. Automation processes the routine; people handle the edge cases and the judgement calls. This is a better use of human expertise — not a replacement of it.

The second misconception is that automation is only for large enterprises. Cloud-based platforms have fundamentally changed this. A fintech startup or early-stage MTO can access the same quality of automation infrastructure as a large bank — through a well-designed platform — at a fraction of the cost of building it from scratch. Scale is no longer a prerequisite for automation maturity.

The third misconception is that compliance requires manual review. This was accurate in an earlier era of financial regulation. It is no longer the case. Risk-based automation is now the global standard endorsed by FATF, the IMF, and national regulators across major markets. Automated, proportionate controls are not just permitted — they are actively preferred by regulators who understand that consistent automated enforcement is more reliable than inconsistent manual review.

Building transaction lifecycle automation internally requires significant engineering effort, ongoing compliance updates, and complex integrations with payout partners, KYC providers, and banking infrastructure. Unified platforms that provide pre-built automation workflows, configurable lifecycle rules, and integrated compliance and reporting allow businesses to focus on growth rather than infrastructure.

If you are looking to start or scale a transaction-driven or cross-border business, RemitSo's platform is designed as a comprehensive transaction lifecycle solution — providing centralised transaction management, configurable lifecycle states, automated compliance and risk controls, integrated payment and settlement workflows, and real-time tracking and reconciliation. By bringing customer experience and back-office operations into a single system, RemitSo helps organisations reduce operational friction while maintaining regulatory readiness across markets.

Transaction lifecycle automation is the use of rule-based digital systems to manage every stage of a transaction — from initiation and validation to settlement and reconciliation — without manual intervention, except for defined exceptions. It replaces disconnected, siloed processes with a single intelligent flow governed by predefined logic and real-time data. The result is a transaction operation that is faster, more accurate, more consistent, and more auditable than any manual equivalent — and one that scales with volume rather than requiring proportional increases in operational headcount.

Automation allows transaction volumes to grow without increasing operational complexity or staffing costs — enabling non-linear scalability. With manual systems, each additional transaction requires proportional human effort. With automated systems, the same infrastructure handles 10,000 transactions as efficiently as 1,000. For businesses operating across multiple markets, currencies, or regulatory environments, this scalability is essential: new corridors or jurisdictions are added through configuration rather than headcount, and compliance is enforced consistently regardless of volume.

No — automation improves compliance by enforcing consistent rules and maintaining detailed, immutable audit trails across all transactions. Manual compliance processes are inherently variable: different staff members apply rules differently, review queues create delays during high-volume periods, and audit trails depend on the quality of manual logging. Automated compliance controls apply exactly the same rules to every transaction, record every decision with a timestamp, and flag exceptions instantly. Regulators including FATF, the FCA, and FinCEN increasingly recognise risk-based automated controls as the preferred standard over manual review.

Yes — and cloud-based platforms have made this genuinely accessible. A fintech startup or early-stage MTO no longer needs to build automation infrastructure from scratch to achieve enterprise-grade transaction management. Well-designed white label and SaaS platforms provide pre-built automation workflows, configurable compliance controls, and integrated settlement and reconciliation at a cost structure that suits early-stage businesses. Launching with automated infrastructure from day one avoids the technical debt and operational friction that companies face when they try to automate systems originally built for manual operation.

Automated reconciliation matches transactions across systems in real time — flagging exceptions instantly rather than accumulating discrepancies for periodic manual review. This eliminates the month-end closing burden that is a consistent pain point in manually operated financial businesses, where reconciliation can consume days of staff time and still produce gaps that require further investigation. Operators migrating from manual to automated reconciliation typically report 60–80% reductions in reconciliation effort, alongside significantly more reliable audit trails for regulatory reporting purposes.

When designed correctly, automated transaction systems are significantly more secure than manual equivalents. Role-based access controls restrict what each user can see and do. Immutable audit trails record every action with a timestamp — providing forensic-quality evidence for both internal governance and regulatory examination. Disaster recovery and redundancy ensure operational continuity when individual components fail. NIST security frameworks for financial systems explicitly identify controlled automation as a key pillar of resilient, secure financial operations — noting that well-designed automation reduces the attack surface associated with human error and privilege misuse.

Any organisation processing recurring or high-value transactions at meaningful volume gains measurable benefits from lifecycle automation. This includes payment platforms, cross-border remittance operators, fintech startups, digital marketplaces, exchange houses, neo-banks, and traditional financial institutions modernising their payment infrastructure. The benefits are most pronounced in cross-border and multi-currency environments, where the complexity of compliance requirements, routing decisions, and reconciliation across multiple systems makes manual handling particularly expensive and error-prone.

Implementation timelines vary significantly depending on approach. Building automation infrastructure from scratch typically takes 12–24 months for a production-ready, compliant system — requiring specialist fintech engineering, compliance architecture, and extensive testing. Deploying on a well-designed white label or SaaS platform that provides pre-built automation workflows significantly reduces this timeline: operators can be live with full transaction lifecycle automation in 4–8 weeks. The platform approach not only accelerates deployment — it also reduces ongoing maintenance burden, since the provider manages compliance updates and infrastructure improvements as part of the service.