There is a conversation that repeats inside remittance operations teams more than it should. "We're short on the corridor again." And when you trace back to when it happened — it's end of month. Or Eid week. Or a Friday afternoon with three large emergency transfers arriving simultaneously. The same situations. Every year. Treated each time as if they were entirely unpredictable. The truth is they were never unpredictable. They were simply unmeasured. Your customers are not sending randomly. They follow patterns that are largely consistent and largely knowable — if you study behaviour rather than aggregate monthly volume. This guide explains how MTO operators can move from reactive liquidity management to a structured, behaviour-based planning model that eliminates the shortfall before it happens.

In This Article

Most money transfer operators plan liquidity the same way. They look at last month's total volume in a corridor, divide by the number of days, and use that daily average to set pre-funding levels. It feels like a rational approach. It is also consistently wrong — and wrong at the worst possible moments.

The daily average is a mathematical abstraction that describes almost no actual day in a corridor. Real transaction flow doesn't distribute evenly across a month. It clusters. It spikes. It follows patterns driven by salary cycles, cultural calendars, family emergencies, and seasonal events — none of which respect the arithmetic convenience of a monthly average.

The consequence of average-based planning isn't just operational inconvenience. It's a trust problem. When a customer initiates a transfer and it's delayed because the operator is short on corridor liquidity, that customer doesn't frame it as a systemic planning failure. They frame it as unreliability. In a category where word-of-mouth referral is the primary acquisition channel — particularly in diaspora communities — a single liquidity-related failure can propagate through a network of potential customers before the operator has even resolved the underlying shortfall.

Figure 1: How average-based and behaviour-based liquidity planning approaches differ in practice

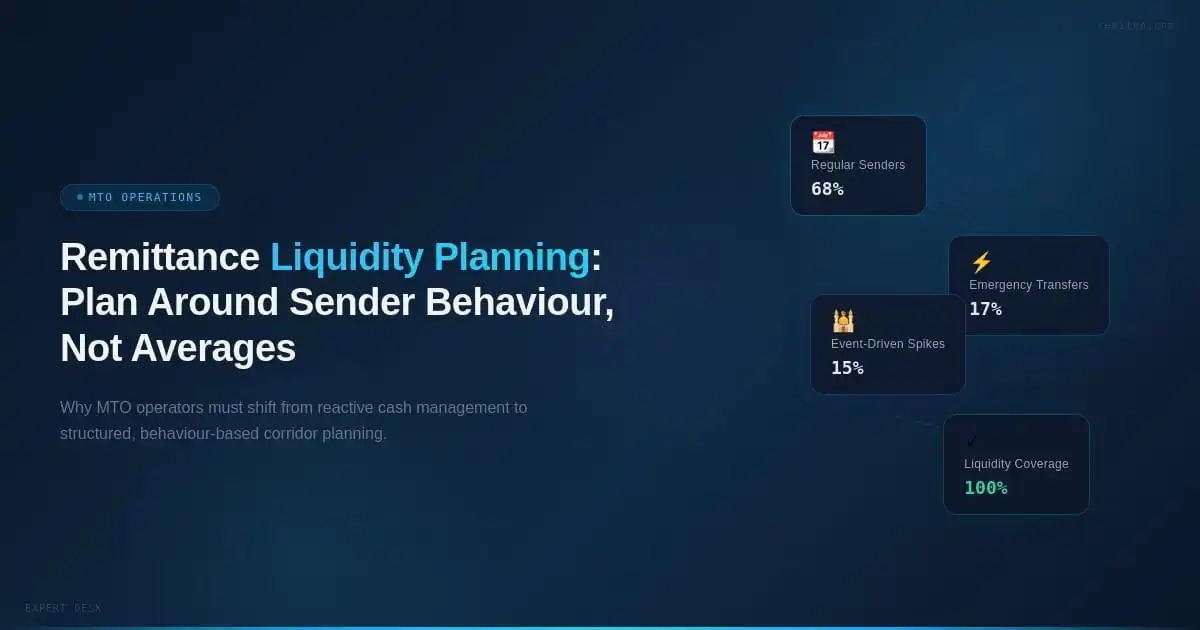

The starting point for any serious liquidity planning model is the recognition that "senders" is not a homogeneous category. The aggregate volume flowing through a corridor is the sum of several distinct sender behaviours — each with a different timing pattern, a different transaction value profile, and a different set of consequences if service fails.

Understanding your corridor at this level of granularity is not a sophisticated analytics exercise reserved for large operators. It is the basic operational discipline that any MTO running a profitable, reliable corridor needs to formalise. The three sender types that drive the majority of liquidity planning complexity are the regular monthly sender, the emergency sender, and the event-driven sender. Each creates a materially different liquidity demand — and each requires a different planning response.

Figure 2: Three distinct sender types and the unique liquidity planning challenge each creates

The regular monthly sender is the backbone of most remittance corridors. This is the customer who sends a fixed or near-fixed amount to family in their home country, timed around salary receipt. In corridors serving labour-sending economies — the UK to South Asia, the Gulf to Southeast Asia, Europe to sub-Saharan Africa — this sender type often represents the majority of transaction volume.

What makes this sender type operationally challenging is not unpredictability — it is concentration. These customers don't distribute their transfers evenly across the month. They send when salary lands, which in most markets means the last three to five working days of the month, or the first two to three days of the new month. In corridors where the majority of senders share a salary cycle — construction workers in the Gulf, NHS employees in the UK, garment workers in Southeast Asia — this concentration effect is extreme. A corridor that processes £500,000 in a typical month may see £150,000 of that within a 72-hour window at month-end.

The planning correction for the regular monthly sender is not complex in principle. It requires moving from monthly average pre-funding to day-of-week and day-of-month-weighted pre-funding. By analysing 12 months of historical transaction data at the day level rather than the month level, most MTOs can identify the concentration window in each corridor with reasonable precision. The pre-funding model is then adjusted to ensure liquidity headroom of 150–200% of average daily volume during that window, rather than 100% of average daily volume applied uniformly.

The emergency sender is the most operationally demanding customer type in any remittance corridor. This is the customer transferring because a family member is ill, has died, has been hospitalised, or is facing an acute financial crisis. The transfer is urgent, the transaction value is often higher than average, and the customer's tolerance for delay is zero.

What makes the emergency sender particularly significant from a liquidity planning perspective is the timing. Emergency transfers, by definition, don't cluster predictably. They arrive outside salary cycles, outside business hours, and often in multiples — a sudden cluster of emergency transfers from the same diaspora community responding to the same event. A single major event in a receiving country can generate a surge of high-value emergency transfers within hours, creating an unplanned liquidity demand in a specific corridor that far exceeds normal daily capacity.

The planning response for the emergency sender is a dedicated emergency liquidity reserve — a corridor-level buffer that sits outside the normal pre-funding calculation and is earmarked specifically for unscheduled demand. The appropriate size of this reserve varies by corridor characteristics: the stability of the receiving country, the demographic profile of the sender community, and the average transaction value for that corridor's emergency transfer history. For corridors serving markets with elevated political or economic risk, this reserve needs to be sized more generously and reviewed quarterly.

Critically, the emergency sender is also the customer who defines your brand in the moments that matter most. This customer is not comparing your exchange rate. They are trusting you at a moment of acute stress and vulnerability. A failure here — a delay, a hold, an inability to execute because liquidity is exhausted — is rarely forgiven, and rarely kept private within the community the customer belongs to.

The event-driven sender transfers around cultural and religious events — Eid al-Fitr, Eid al-Adha, Diwali, Christmas, Lunar New Year, and a range of national and regional holidays that vary by corridor. These are, without exception, the most predictable volume spikes in the remittance calendar. The dates are known months or years in advance. The corridors affected are known. The approximate magnitude of the volume increase is estimable from prior-year data. And yet, year after year, operators find themselves underprepared for these windows as if they arrived without warning.

The operational failure here is not a lack of information — it is a lack of institutionalised planning process. Liquidity uplift for known cultural windows is not embedded into the annual planning cycle with enough lead time for pre-funding to be arranged, payout partner capacity to be confirmed, and FX hedging positions to be adjusted. Instead, the spike arrives, creates pressure, and is resolved reactively — with higher FX costs, partner escalation fees, and the operational friction that comes from urgently acquiring liquidity that should have been arranged weeks earlier.

There is a compounding dynamic at work during major remittance events that most MTOs understand intuitively but manage poorly in practice. During Eid, Diwali, Christmas, and similar windows, two things happen simultaneously: transaction volume in affected corridors increases significantly, and FX volatility in the relevant currency pairs tends to increase as well.

The reason for this collision is straightforward. Major remittance events create increased demand for the destination currency. That demand is not generated only by MTOs — it flows through multiple channels, including bank transfers, informal networks, and mobile money platforms. The aggregate demand signal creates price pressure in the spot market for the relevant currency pair. At the same time, the liquidity conditions in receiving markets during major holiday periods can be thinner than normal, amplifying the spread on FX execution.

The practical consequence for an MTO is that their margin is under maximum pressure precisely when their volume is at its highest. The FX spread they capture on each transaction is narrower because the market rate is moving against them, while the volume of transactions — each potentially impacted by that margin compression — is elevated. For operators who haven't pre-positioned their FX exposure ahead of the event window, the cost of acquiring rate during the peak itself is materially higher than if they had hedged or pre-purchased in the preceding period.

Figure 3: The compounding impact of volume spikes and FX volatility on MTO margin during seasonal peaks

The FX planning discipline required to protect margin during event windows is an extension of the liquidity planning discipline described above. MTOs that treat the two as separate functions — treasury managing FX independently from operations managing liquidity — consistently underperform during peak periods compared to those who coordinate pre-funding decisions with FX pre-positioning in a single planning cycle.

Moving from average-based to behaviour-based liquidity planning requires a structured framework that can be maintained operationally without becoming a full-time analytical function. The goal is not to build a perfect predictive model — it is to institutionalise enough visibility into sender behaviour patterns that the most costly and avoidable shortfalls are systematically eliminated.

Figure 4: Five-step framework for building a behaviour-based liquidity planning model in remittance operations

The abstract framework above becomes operational when it is applied at corridor level with specific numbers and specific calendar dates. Here is what corridor-level liquidity modelling looks like for an MTO running a UK-to-Pakistan corridor — one of the highest-volume remittance corridors globally and one where all three sender types are present in significant proportions.

In this corridor, the regular monthly sender cluster is concentrated in the final five working days of each month, reflecting the UK salary cycle. Historical data shows that approximately 35% of monthly volume transacts in this window. The emergency sender represents roughly 8–12% of transactions but a higher share of value, with spikes observable in the data following significant events in Pakistan. The event-driven sender creates the two largest volume windows of the year: the 10 days before Eid al-Fitr and the 10 days before Eid al-Adha.

| Planning Window | Sender Type | Pre-Funding Tier |

|---|---|---|

| Days 1–22 of month | Mixed / baseline | Baseline — standard daily pre-fund |

| Days 23–28 of month | Regular monthly sender | Elevated — 150% of baseline, triggered day 20 |

| Eid al-Fitr window (10 days prior) | Event-driven sender | Peak — 220% of baseline, triggered 14 days prior |

| Eid al-Adha window (10 days prior) | Event-driven sender | Peak — 220% of baseline, triggered 14 days prior |

| Any time — unscheduled | Emergency sender | Reserve — dedicated buffer, replenished within 48hrs |

Figure 5: Illustrative corridor liquidity planning model showing tiered pre-funding triggers for a UK-to-Pakistan corridor

This model is not operationally complex to maintain once it is set up. It requires a quarterly review to validate that the historical patterns are holding, an annual refresh of the cultural calendar, and a standing process for replenishing the emergency reserve within 48 hours of any draw. What it eliminates is the reactive scramble — the end-of-month call about being short on the corridor, treated as if it were a surprise.

One of the structural barriers to implementing behaviour-based liquidity planning is the absence of transaction-level data visibility in a format that makes sender behaviour analysis straightforward. Many MTOs have the data somewhere — in their core platform, in payout partner reports, in customer records — but not consolidated in a way that supports the kind of day-level, sender-type-level analysis described in this article.

If you're building or scaling a money transfer operation and want the operational infrastructure to manage liquidity as a structured discipline rather than a reactive function, RemitSo's platform is designed specifically for regulated MTOs who need corridor-level visibility across transaction data, payout performance, and operational metrics — the foundation on which a real liquidity planning model can be built.

Remittance liquidity planning is the process by which a money transfer operator ensures it has sufficient pre-funded capital in each active corridor to meet customer transfer obligations as they arise — without delay, shortfall, or reliance on emergency funding. It matters because liquidity failures translate directly into customer-facing delays, which in a referral-driven industry create reputational damage that extends far beyond the individual transaction. Effective liquidity planning is also a regulatory requirement under frameworks like the UK Payment Services Regulations 2017, which mandate that MTOs maintain adequate payment resources at all times.

Average-based liquidity planning divides total monthly volume by the number of days to produce a uniform daily pre-funding target. The problem is that remittance transaction flow is never uniformly distributed. It clusters around salary cycles at month-end, spikes during cultural and religious event windows, and surges unpredictably in response to emergencies in receiving countries. An average-based model funds every day at the same level and therefore systematically underfunds the days when actual demand is highest — precisely the days when a shortfall causes the most customer impact.

The three sender types that create distinct liquidity demands in remittance corridors are: the regular monthly sender, who transfers around the same time each month after salary receipt — predictable but concentrated into a narrow window; the emergency sender, who transfers in response to an urgent family or personal crisis — unpredictable in timing but carrying zero tolerance for delay; and the event-driven sender, who transfers ahead of major religious or cultural events like Eid, Diwali, or Christmas — highly predictable in timing but consistently under-planned for by most MTOs.

MTOs should treat Eid, Diwali, Christmas, Lunar New Year, and other high-volume cultural windows as scheduled operational events requiring advance liquidity uplift. The recommended approach is to set a pre-funding trigger date 10–14 business days before each event window opens, at which point corridor liquidity is increased to a peak tier — typically 200–250% of the baseline daily pre-fund. FX pre-positioning should be executed at the same time to avoid acquiring currency during the peak window when market spreads are wider. This process should be embedded in an annual cultural calendar built at the start of each financial year.

The emergency sender is transferring because something serious has happened — a family illness, a bereavement, an acute financial crisis. This customer is not comparing exchange rates. They are trusting your service at their most vulnerable moment. Their tolerance for delay is zero, and their transaction value is often above the corridor average. A failure to execute an emergency transfer because corridor liquidity is exhausted is one of the most damaging events an MTO can create — both for the individual customer relationship and for the wider diaspora community in which word of the failure will spread rapidly. A dedicated emergency liquidity reserve, sized and maintained specifically for this sender type, is essential infrastructure for any serious MTO operation.

During major remittance event windows, elevated demand for destination currencies — from MTOs, banks, and informal transfer channels simultaneously — creates price pressure in the relevant currency pairs. This tends to widen the FX spread available to MTOs acquiring rate in the spot market during the event itself. At the same time, liquidity in receiving-country markets may be thinner during holiday periods, amplifying spread further. The net result is that MTO margin per transaction is compressed exactly when transaction volume is highest — a double squeeze on corridor profitability that can only be mitigated by pre-positioning FX exposure ahead of the event window.

Building a behaviour-based liquidity model requires at minimum 12 months of transaction-level data for each active corridor, with timestamps granular enough to analyse by day of month and day of week. From this data, the operator should be able to identify the salary cycle concentration window, any recurring event-driven spikes, and the historical profile of emergency transfer surges. This data is typically held within the MTO's core platform but often not surfaced in a format that supports this type of analysis without additional reporting work. MTOs that lack this visibility at corridor level are operating with a material blind spot in their financial planning.

A corridor liquidity planning model should be reviewed at three intervals: quarterly, to validate that historical transaction patterns are holding and adjust pre-funding tiers if corridor behaviour has shifted; annually, to refresh the cultural calendar for the coming year and recalibrate the emergency reserve size based on updated corridor risk profiles; and event-triggered, whenever a significant change occurs in the corridor — a new payout partner, a change in the receiving country's economic or political stability, or a major unexpected volume event that reveals a gap in the existing model.