Here is a question every growing remittance operator will face: when is the right time to launch a new corridor? The instinctive answer focuses on demand — customer requests, diaspora population data, competitive gaps. But that answer misses the real bottleneck entirely. The operators who expand fastest are not the ones who identify demand first. They are the ones whose infrastructure was designed for multi-market operations from day one.

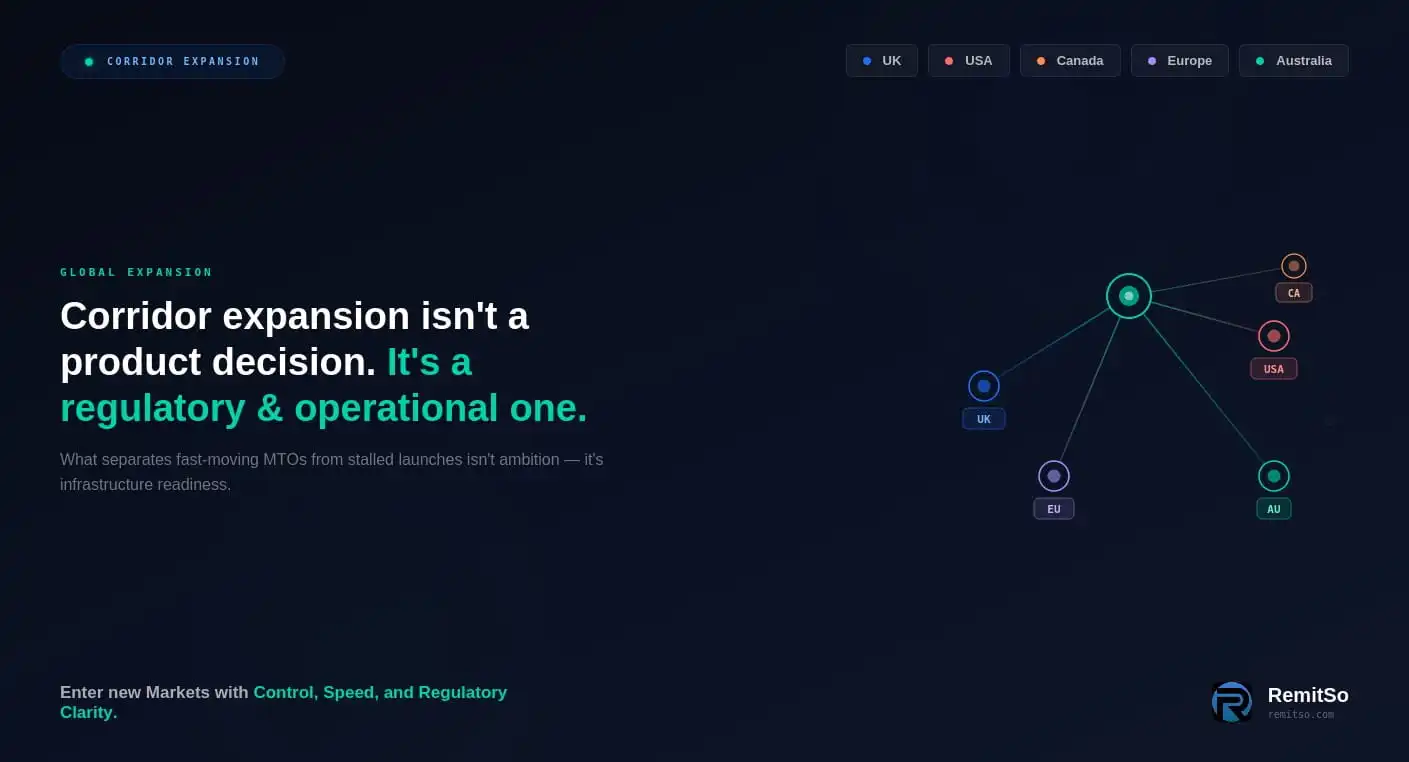

Corridor expansion is not a product decision. It is a regulatory and operational readiness decision. The difference between an operator who launches a new corridor in under 30 days and one who takes 6–12 months is almost never about ambition, funding, or even regulatory complexity. It is about whether the operational infrastructure — licensing, compliance, payout connectivity, settlement, FX orchestration — was built to scale across jurisdictions, or whether each new market requires rebuilding from scratch.

This article examines exactly what slows most corridor launches — in specific operational terms — and how the most disciplined operators in the market have structured their way past each bottleneck. This is not about working harder. It is about building infrastructure that removes the bottleneck before it forms.

In This Article

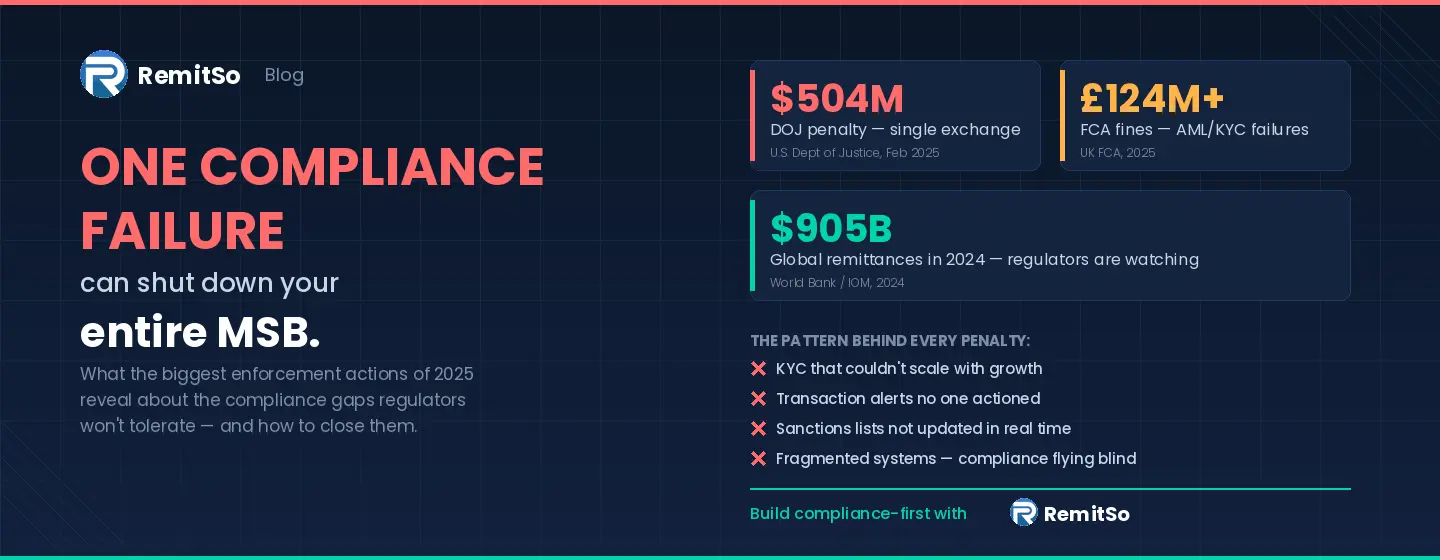

The global remittance industry processed an estimated $905 billion in transfer flows in 2024, according to the World Bank's Migration and Development Brief. Demand for cross-border transfers is not slowing — it is accelerating, driven by labour migration, diaspora growth, and digital-first customer expectations. The corridors with the strongest growth are precisely the ones that operators find hardest to enter: UK to West Africa, USA to South Asia, Canada to the Philippines, Europe to Latin America, Australia to the Pacific Islands.

But here is what the data consistently shows: when remittance businesses stall on expansion — when the next corridor takes 9 months instead of 9 weeks — the cause is rarely a lack of demand or even regulatory hostility. It is the absence of infrastructure that was designed to support multi-market operations. Every new corridor becomes a separate project: new licence applications, new compliance builds, new payout partner negotiations, new settlement arrangements, new FX integrations. Each one starts from zero. Each one takes months. And by the time the corridor is live, the competitive window has often narrowed significantly.

Figure 1: The operational difference between rebuilding infrastructure per corridor and operating on an expansion-ready platform

The failure modes are consistent. Different companies, different corridors, different years — but the same five infrastructure bottlenecks appear repeatedly. Understanding them individually matters because each one has a different root cause, a different cost, and a different solution.

Figure 2: The five infrastructure bottlenecks that cause most corridor launches to stall between 6 and 12 months

When a money transfer operator decides to open a new corridor — say, UK to Nigeria, or USA to India — the product side is usually the least of their worries. The first wall they hit is licensing. The FCA in the United Kingdom, FinCEN and state-level regulators in the United States, FINTRAC in Canada, the EBA and national competent authorities across Europe, AUSTRAC in Australia — each comes with its own application process, capital requirements, ongoing reporting obligations, and timelines that can stretch into months or even years.

For operators with multi-corridor ambitions, this licensing complexity compounds rapidly. A business that wants to serve five send markets is not dealing with one regulatory application — it is managing five separate regulatory relationships, each with different requirements, different timelines, and different ongoing obligations. Without a platform that already operates within these licensed environments, each new corridor starts from the most expensive and time-consuming step: regulatory access itself.

Even after licensing is secured, the compliance infrastructure challenge remains. The KYC workflows, AML monitoring rules, sanctions screening processes, and PEP checking procedures that work in one jurisdiction often need fundamental rethinking for another. Sanctions lists differ between OFAC, the EU Consolidated List, and the UK Sanctions List. PEP definitions vary. The thresholds that trigger Suspicious Activity Reports change from country to country. A compliance framework built for UK operations does not automatically satisfy Canadian or Australian requirements.

Local payout connectivity is one of the most underestimated bottlenecks in corridor expansion. Having a licence to operate does not mean you can actually move money into the destination market. You need established relationships with local banks, mobile money operators, and cash pickup networks — and each of these comes with its own integration timeline, compliance requirements, and settlement arrangements. Negotiating these partnerships takes time, credibility, and usually a local presence. For operators entering a new market, this step alone can add 3–6 months to a corridor launch.

Cross-border settlement is never a copy-paste operation. New corridors mean new currency pairs, new nostro/vostro arrangements, new liquidity management requirements, and new FX risk that all need to be orchestrated in near-real-time. For operators building this from scratch per corridor, the technical complexity is significant — and the operational risk during the early days of a new corridor, before volume stabilises and processes mature, is substantial.

The cumulative cost of per-corridor rebuilding does not appear on a single line of your P&L. It is distributed across categories that look unrelated — regulatory costs, staffing overhead, time-to-market delays, competitive displacement — until you map them back to their root cause: infrastructure that was not designed to scale across markets.

Figure 3: Quantified operational impact of rebuilding infrastructure per corridor — across time, cost, and competitive positioning

The most direct cost of per-corridor rebuilding is time. A corridor that takes 9 months to launch instead of 30 days is not simply delayed — it represents 8 months of revenue that your competitor captured while you were still integrating payout partners and waiting for regulatory approvals. In high-growth corridors, this time advantage compounds. The operator who launches first builds volume, establishes pricing expectations, and locks in customer relationships that are expensive to displace later.

When every corridor requires its own compliance build, its own partner negotiations, and its own settlement configuration, the staffing requirement scales linearly with the number of corridors. This is the operational model of a consulting project, not a scalable technology business. The operators who scale most efficiently have decoupled corridor count from headcount — because the infrastructure handles the per-corridor variation, not the team.

Correspondent banking relationships are under increasing scrutiny globally. Banks conducting due diligence on remittance partners want to see a structured, documented, technology-driven operation — not a patchwork of manual processes that differ by corridor. Operators whose infrastructure is inconsistent across corridors face a higher risk of correspondent banking partner withdrawal, which can shut down an entire corridor overnight regardless of customer demand.

Operational readiness for corridor expansion does not mean more staff, more overhead, or more process. It means that the infrastructure dependencies which block most launches — licensing, compliance, payout connectivity, settlement, and FX — are already resolved at the platform level. Here are the five pillars that differentiate expansion-ready operators from those who rebuild per corridor.

Figure 4: The five infrastructure pillars that separate expansion-ready remittance operators from those who rebuild per corridor

Rather than applying for licences in every jurisdiction independently — a process that can take 12–18 months and cost six figures per country — the right infrastructure partner lets you operate under established licensed environments across the corridors that matter most. This is not a shortcut around regulation. It is the use of a platform that has already completed the licensing work, maintains the ongoing regulatory relationships, and provides the compliance infrastructure that those licences require.

For operators targeting the five major send markets — the United Kingdom, the United States, Canada, Europe, and Australia — this means access to FCA-authorised environments, state-level MSB licensing, FINTRAC registration, EBA-aligned frameworks with EU passporting, and AUSTRAC-registered operations. The licensing groundwork is done. The operator's focus shifts to the decisions that actually differentiate their service: pricing, customer experience, and corridor-specific go-to-market strategy.

This model also solves the ongoing compliance burden. Maintaining licences across multiple jurisdictions requires continuous regulatory monitoring, periodic renewals, capital adequacy management, and regular reporting. On an expansion-ready platform, these obligations are managed at the infrastructure level — not absorbed into the operator's compliance team as additional manual workload per corridor.

Payout connectivity is the most underestimated bottleneck in corridor expansion. An operator can have the licence, the compliance framework, and the customer demand — but without established relationships with local banks, mobile money operators, and cash pickup networks in the destination country, money cannot actually move. Each payout partnership comes with its own integration timeline, compliance due diligence, contract negotiation, and settlement arrangement. For operators entering a new market, this step alone commonly adds 3–6 months to a corridor launch timeline.

Infrastructure-first platforms solve this by providing access to payout networks that are already integrated, tested, and settled. The operator does not need to negotiate individual partnerships from scratch. They configure the corridor, select the payout methods they want to offer — bank deposits, mobile money, cash pickup, wallet-to-wallet — and start processing. The integration work, the due diligence, the settlement arrangements are already in place.

Instead of building bespoke compliance workflows for every new corridor, expansion-ready platforms provide corridor-specific compliance alignment. This means KYC flows, sanctions screening, transaction monitoring, and regulatory reporting that adapt to each jurisdiction's requirements without requiring a ground-up rebuild.

The practical impact is significant. Sanctions screening that automatically applies the relevant list per corridor — OFAC for US-originated transactions, the EU Consolidated List for European corridors, the UK Sanctions List for UK corridors — without manual configuration per transaction. KYC document requirements that adjust based on the send and receive jurisdictions. Transaction monitoring thresholds that reflect the specific regulatory expectations of each corridor. And reporting that generates the format and frequency each regulator requires.

Consumer protection regulations in the European Union (under PSD2), the United Kingdom (FCA Payment Services Regulations 2017), and the United States (Dodd-Frank Section 1073 remittance disclosure rules) all impose corridor-specific disclosure and monitoring requirements. A compliance framework that cannot adapt per corridor is not just inefficient — it is a regulatory liability.

Perhaps the most technically complex part of any new corridor is the settlement and FX layer. New currency pairs, new counterparties, new liquidity requirements — all need to work in real-time with minimal manual intervention. For operators building this from scratch, each new corridor means sourcing FX liquidity, configuring settlement rails, managing nostro positions, and building reconciliation processes — all before a single transaction flows.

Ready-made FX orchestration removes this burden. Pre-configured settlement rails, competitive rate sourcing with defined tolerance bands, automated position management, and real-time reconciliation across payout partners mean the operator can focus on volumes and margins rather than plumbing. Rate management is controlled — not left to per-transaction judgment that creates invisible revenue variance.

For operators serving volatile currency corridors — West Africa, South Asia, Latin America — this infrastructure-level FX management is not optional. Without defined tolerance bands and automated rate controls, the financial exposure from inconsistent FX decisions accumulates silently until it appears as unexplained revenue underperformance in a retrospective analysis.

The compound effect of the first four pillars is a go-live timeline that collapses from months to weeks. When licensing, compliance, payout connectivity, and settlement infrastructure are already in place at the platform level, the operator's work to launch a new corridor reduces to configuration: selecting corridors, setting pricing, defining customer limits, and going live. The infrastructure dependencies that typically consume 80% of a corridor launch timeline are already resolved.

This changes the economics of expansion fundamentally. Corridors that were previously marginal — not enough projected volume to justify a 9-month, six-figure launch investment — become viable when the launch cost is measured in days and configuration effort rather than months and dedicated project teams. The addressable market expands because the cost of entering it drops by an order of magnitude.

| Pillar | Rebuilding Per Corridor | Expansion-Ready Infrastructure |

|---|---|---|

| Licensing | 12–18 months per country — separate applications, legal counsel, capital reserving | Pre-licensed — operate under established environments across 5 key markets |

| Compliance | Rebuilt per jurisdiction — KYC, AML, monitoring all reconfigured from scratch | Adaptive — corridor-specific rules auto-apply per jurisdiction |

| Payout Connectivity | 3–6 months per market — partner negotiation, integration, testing, settlement setup | Pre-integrated — bank, mobile money, cash pickup networks already connected |

| Settlement & FX | Manual — new currency pairs, nostro arrangements, and rate management per corridor | Orchestrated — pre-configured rails, tolerance bands, automated reconciliation |

| Go-Live Timeline | 6–12 months — stacked dependencies, serial execution, project-team staffing | Under 30 days — configure, test, launch |

Figure 5: What each infrastructure pillar looks like when rebuilt per corridor vs. when operating on expansion-ready infrastructure

Moving from per-corridor rebuilding to expansion-ready infrastructure is not a single project. It is a sequenced programme with clear milestones that each build on the previous one. The sequence below reflects the logical dependency structure — each stage enables the next.

Figure 6: A six-stage implementation sequence for moving from per-corridor rebuilding to expansion-ready infrastructure

The operators who have moved to expansion-ready infrastructure report consistent changes in the same areas. Corridor launch timelines compress from months to weeks — not because staff work faster, but because the dependencies that previously required months of work are already resolved. Staffing requirements decouple from corridor count — because per-corridor compliance and integration work is handled at the platform level. Correspondent banking relationships stabilise — because partners can see consistent, documented, technology-driven operations across all corridors. And revenue from new corridors starts flowing months earlier than it would have under the old model.