Here is a question most remittance operators never ask themselves: what actually causes an operation to break down? The instinctive answer is risk — specifically, the risk of the corridors you serve. High-risk markets, volatile currencies, difficult regulatory environments. But that answer is wrong. Or rather, it is incomplete in a way that costs real businesses real money every day.

The corridors you operate in are not the cause of operational failure. They are the environment you operate in. The cause is almost always the same thing, regardless of whether you are sending money to Southeast Asia, Sub-Saharan Africa, or Latin America: unclear, undocumented, unenforced internal operating rules. When your team does not know exactly what the rules are, every decision becomes a judgment call. And when every decision is a judgment call, your operation scales like a house of cards.

This article explains exactly how that failure mode works — in specific operational terms — and how the most disciplined remittance operators in the market have structured their way out of it. This is not about adding more compliance staff. It is about designing risk governance into the operation itself, so the rules work whether anyone is watching or not.

In This Article

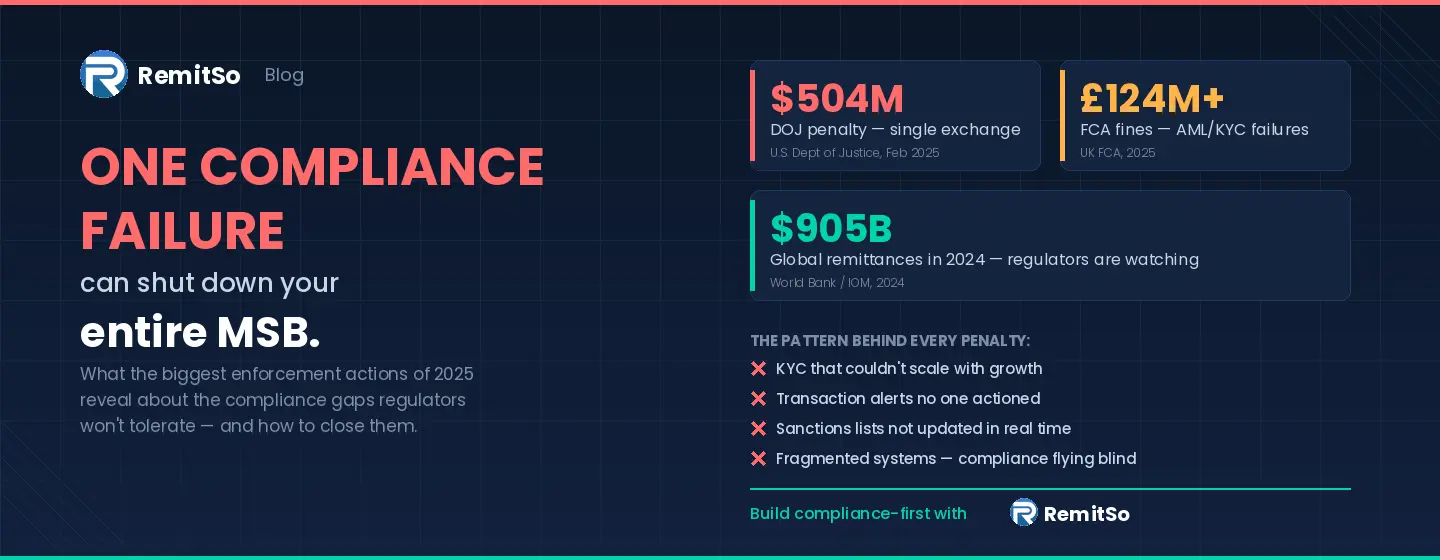

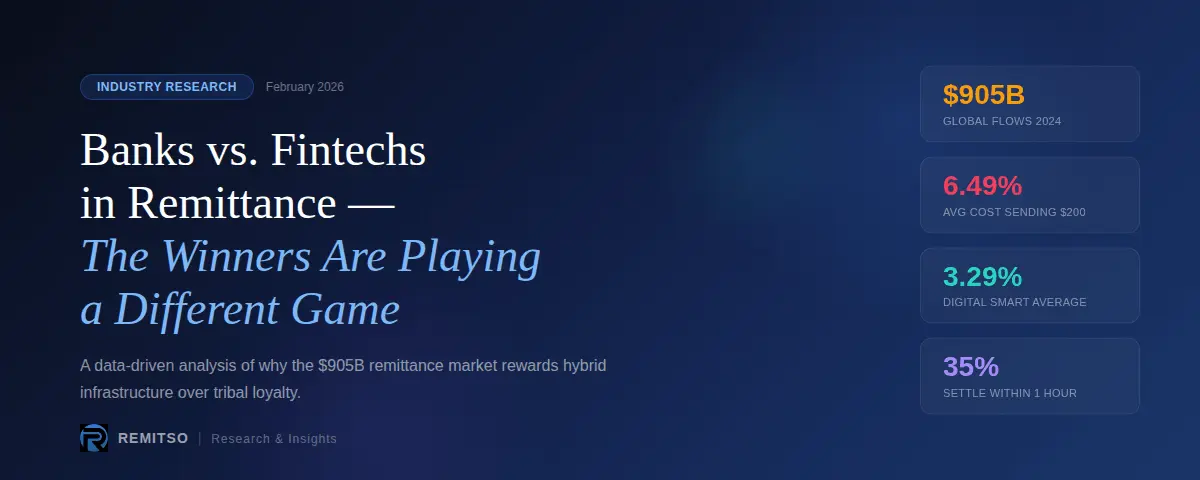

The global remittance industry processed an estimated $905 billion in transfer flows in 2024, according to the World Bank's Migration and Development Brief. A significant portion of that volume flows through precisely the corridors that processors, correspondent banks, and regulators describe as elevated risk: West Africa, South Asia, the Middle East, Latin America. The operators who serve these corridors are not doing something inherently dangerous. They are serving a genuine and massive demand — often from populations with no access to alternative financial services.

But here is what the data consistently shows: when remittance businesses fail operationally — when they face regulatory action, settlement partner withdrawal, or sudden processing interruption — the cause is rarely the corridor itself. It is the absence of structured, documented, enforced operating rules around how that corridor is managed. The Financial Action Task Force (FATF) and FinCEN enforcement actions against money services businesses overwhelmingly cite the same root issues: inadequate transaction monitoring, unstructured approval processes, inconsistent KYC application, and incomplete audit documentation. All of which are symptoms of one thing — rules that exist informally, if at all.

Figure 1: The operational difference between an unstructured and a structured remittance operation — at the decision level

The failure modes are consistent. Different companies, different corridors, different years — but the same four operational breakdowns appear repeatedly. Understanding them individually matters because each one has a different root cause and a different fix.

Figure 2: The four operational failure modes that emerge when remittance operating rules are informal or undefined

In a structured operation, every corridor has defined transaction limits: a single-transaction ceiling, a daily individual limit, and a periodic aggregate threshold. These limits are informed by the corridor's risk profile, the regulatory requirements of the send and receive jurisdictions, and the operator's AML policy. They are documented, programmatically enforced, and regularly reviewed.

In an unstructured operation, limits exist informally — if at all. Staff apply limits based on their own understanding of what is appropriate, which varies by individual, experience level, and what mood they are in when a decision is required. This inconsistency is not just an internal quality problem. It is a regulatory liability. FinCEN and equivalent regulators in the United Kingdom (FCA) and European Union (EBA) expect to see documented, consistently applied transaction limits as a basic component of an anti-money laundering programme. When limits are informal, they are effectively non-existent from a compliance standpoint.

Every organisation has an informal escalation path — a mental model of who gets consulted when a decision is difficult. In early-stage operations, this works well enough. But as transaction volume grows, the informal model breaks. Decisions pile up. The people who get escalated to become bottlenecks. Response times slow. And increasingly, senior staff who should be building the business are instead approving individual transactions one by one.

The structured alternative is a tiered approval framework: clearly defined value thresholds and risk score bands that determine automatically whether a transaction processes, holds for review, or requires a specific level of sign-off. The decision logic is codified, not carried around in someone's head. And critically, it is consistent — the same rule applies whether the transaction comes in at 9 AM or 11 PM on a Saturday.

Foreign exchange rate management is one of the least discussed and most financially significant operational variables for remittance operators. Every transaction involves a spread between the rate you receive from your FX provider and the rate you quote to your customer. When this spread is managed with a defined tolerance band — a maximum acceptable deviation from the mid-market rate per corridor — your revenue is predictable and your exposure is bounded.

When it is managed by individual judgment, neither is true. Staff make rate decisions based on different interpretations of what is acceptable. Some transactions go out at excellent margins. Others go out at minimal margins — or occasionally at a loss — because no one is working from the same framework. In a high-volume operation, this variance compounds into material revenue leakage. The World Bank's Remittance Prices Worldwide database consistently shows that the cost of a typical remittance corridor fluctuates more than operators intend — not because FX markets are volatile, but because internal rate management is inconsistent.

The cumulative cost of unstructured operations does not appear on a single line of your P&L. It is distributed across categories that look unrelated — revenue variance, compliance costs, staffing overhead, settlement partner friction — until you map them back to their root cause.

Figure 3: Quantified operational impact of unstructured internal rules — across transaction speed, revenue, and regulatory risk

The remittance customer does not know or care that your approval process is informal. They sent money that needs to arrive by a specific time. When manual escalation chains slow down transaction processing — because the relevant person is unavailable, or the case is unusual enough that no one is certain how to handle it — the customer experiences an unexplained delay. In a sector where customer acquisition is expensive and churn is high, operational delay is one of the fastest ways to permanently lose a customer relationship that took real effort to build.

Revenue leakage from inconsistent FX decisions is particularly pernicious because it does not trigger an obvious alert. No individual transaction causes a measurable loss. The problem is structural and cumulative — it shows up as unexplained revenue underperformance relative to projected margins when you do a retrospective analysis. By which point it has already been happening for months.

This is the most serious consequence — and the one most operators discover too late. When a regulator or correspondent banking partner conducts an audit of your operation, they will ask for documentation of specific decisions. Why was this transaction processed? What limit applied? Who approved it? What rule governed the FX rate applied? In a structured operation, every one of those questions has a documented, specific answer. In an unstructured operation, the honest answer is: "Someone made a judgment call, and we have no record of it." That answer does not satisfy a regulator. And in a correspondent banking review, it is often the difference between a continued relationship and a sudden termination notice.

Operational maturity in remittance does not mean more staff, more overhead, or more process for its own sake. It means that the decisions which need to be made consistently are governed by documented rules — and that those rules are enforced at the system level rather than relying on individual knowledge or discipline. Here are the five foundational rules that differentiate structurally sound remittance operators from those running on judgment.

Figure 4: The five foundational operating rules that separate structurally sound remittance operators from those running on informal judgment

A corridor risk limit is not simply a maximum transaction amount. It is a layered framework that governs the risk parameters for every transaction flowing through a specific send-and-receive country pair. A well-designed corridor limit framework includes a single-transaction maximum, a daily per-customer aggregate limit, and a rolling periodic threshold that triggers enhanced due diligence when breached. These limits are set based on a formal risk assessment of the corridor — factoring in the FATF risk rating of the relevant jurisdictions, the correspondent banking environment, the typical customer profile, and the operator's own risk appetite.

The limits are not set once and forgotten. They are reviewed on a scheduled basis — typically quarterly or when corridor conditions change materially. And critically, they are enforced at the platform level, not by individual operational judgment. A transaction that exceeds a corridor limit either routes to an enhanced review queue automatically or is declined with a system-generated reason code — not approved or declined based on who happened to be handling the queue that day.

For operators with multi-corridor businesses, this requires a corridor-level risk matrix: a formal document that defines the risk classification, applicable transaction limits, EDD triggers, and review protocols for each send-receive pair the business operates. This document is not just good operational practice. It is the core artefact that compliance examiners request when reviewing an MSB's transaction monitoring programme under BSA, PSD2, or equivalent frameworks.

The concept of rule-based approval tiers is straightforward, but implementation requires deliberate design. The objective is to create a clear decision tree that governs transaction processing without requiring human intervention except at clearly defined thresholds. Transactions below a specified value and risk score process automatically. Transactions that meet specific criteria — value above a threshold, customer with an elevated risk rating, corridor flagged for enhanced monitoring, source of funds requiring clarification — route to a defined review queue with a defined time-to-decision standard. Transactions that trigger regulatory reporting obligations route to a compliance officer review queue.

The key design principle is specificity. Vague criteria — "unusual transactions" or "high-value cases" — do not create a rules-based system. They create a discretionary system with a formal-looking wrapper. The rule must be specific enough that two different staff members applying it independently would reach the same outcome. If two people reviewing the same transaction would make different decisions because the rule is unclear, the rule is not a rule. It is still judgment.

FX rate management is often treated as a treasury or finance function in remittance operations — separate from compliance and operations. This separation is a mistake. FX tolerance bands are fundamentally a risk control, because uncontrolled rate variance creates both financial and consumer protection exposure.

A tolerance band defines the maximum acceptable deviation from the mid-market rate — or from the operator's internal reference rate — for a given corridor at a given time. When a transaction would be priced outside the band, the system requires an explicit override with a documented rationale. This serves two purposes: it prevents ad hoc rate decisions from accumulating into material revenue leakage, and it creates an auditable record of every rate applied and the basis for applying it.

Consumer protection regulations in the European Union (under the Payment Services Directive 2, as enforced by national competent authorities), the United Kingdom (FCA Payment Services Regulations 2017), and the United States (Dodd-Frank Section 1073 remittance disclosure rules) all require remittance providers to disclose the exchange rate applied to a transfer accurately and in advance. When FX decisions are made informally, the risk of a rate being applied that was not properly disclosed in advance — with the regulatory consequence that implies — becomes material. A defined tolerance band is part of the compliance infrastructure that prevents that scenario.

Exceptions are, by definition, cases that do not fit the standard process. Every remittance operation has them. The question is not whether they occur — it is whether they are handled through a defined path or improvised from scratch each time.

An automated exception path is a predefined workflow that activates when a transaction or customer situation falls outside standard parameters. The workflow specifies who reviews the case, what documentation is required before a decision is made, what the time-to-decision standard is, what the escalation path is if the first reviewer cannot resolve it, and how the decision is documented. The path is designed in advance, not invented in the moment.

In practice, this requires categorising the types of exceptions your operation encounters — which, for most remittance businesses, falls into a relatively small number of recurring categories: unusual source of funds, customer-flagged name match, transaction pattern inconsistent with stated purpose, document expiry during a pending transaction, and a handful of others specific to your corridors. Each category has a defined resolution workflow. When a case is categorised, the workflow activates. The exception is handled consistently — not however the available staff member decides to handle it.

An audit trail is not simply a transaction log. It is a contemporaneous record of every decision made — the specific rule applied, the threshold that governed the decision, the identity of the individual or system that made it, and the time at which it was made. A genuine decision audit trail allows any transaction to be reconstructed fully from the record alone, without relying on memory or post hoc explanation.

This matters for three distinct reasons. First, regulatory compliance: FinCEN Regulation 31 CFR Part 1022, the FCA's AML guidance for payment service providers, and FATF Recommendation 10 all require MSBs to maintain records sufficient to allow reconstruction of individual transactions on request. An informal decision process does not create records sufficient for this purpose. Second, internal quality management: without decision records, it is impossible to identify patterns in how decisions are being made — and therefore impossible to identify where the informal process is creating inconsistency. Third, correspondent banking relationships: correspondent banks increasingly conduct detailed due diligence reviews of their remittance business partners, and a business that cannot produce clean decision records on request is unlikely to survive a thorough review.

| Pillar | Without a Rule | With a Rule |

|---|---|---|

| Transaction Limits | Guessed — varies by staff, by day, by instinct | Enforced — same limit applied to every case, always |

| Approval Thresholds | Escalated — queues pile up, decisions get delayed, bottlenecks form | Automated — tier-appropriate decision in real time |

| FX Rate Decisions | Ad hoc — uneven margins, invisible revenue leakage, consumer risk | Bounded — every rate within defined tolerance, deviations documented |

| Exception Handling | Improvised — each case treated as unique, no consistency, no speed | Routed — exception categorised and handled through predefined workflow |

| Decision Records | Missing — undocumented, unauditable, indefensible under examination | Complete — every decision logged with rule, timestamp, and outcome |

Figure 5: What each operating pillar looks like without a defined rule vs. with one — in practical operational terms

Building a structured operating framework for a remittance business is not a single project. It is a sequenced programme with clear milestones that each build on the previous one. The sequence below reflects the logical dependency structure — each stage enables the next.

Figure 6: A seven-stage implementation sequence for building a structured operating rules framework in a remittance business

The operators who have implemented structured rule frameworks report consistent changes in the same areas. Transaction processing times improve — not because staff work faster, but because the decisions that previously required escalation now resolve automatically. Revenue variance narrows — not because FX markets become less volatile, but because internal rate decisions become consistent. Audit readiness improves dramatically — because decision records exist. And correspondent banking relationships stabilise — because partners can see, in documentation, that the business is run by rules rather than by individuals.

If you are building or scaling a remittance operation, RemitSo's white-label infrastructure is designed from the ground up to support structured operational frameworks — with configurable transaction limits, automated approval routing, FX tolerance controls, exception workflow management, and full decision audit logging built into the platform rather than bolted on.