A technical and operational guide to how payment APIs work in cross-border transactions — covering KYC, AML, FX, payout routing, open banking, and the infrastructure choices that define modern global payment platforms.

APIs — Application Programming Interfaces — are the invisible infrastructure underneath every modern international payment. When a customer sends money abroad through a remittance app, initiates a cross-border supplier payment from a business banking platform, or receives a payout through a digital wallet, multiple API calls are executing simultaneously: verifying identity, screening against sanctions lists, fetching live exchange rates, selecting payment routes, and triggering disbursement. Understanding how these APIs work, how they connect, and where they create risk is no longer exclusively a developer concern — it is foundational knowledge for any operator building or scaling a global payment business in 2026.

In This Article

An API (Application Programming Interface) is a defined set of protocols and data formats that allows two software systems to communicate with each other. In payment contexts, APIs act as secure, standardised channels through which applications — a remittance app, a banking platform, a compliance screening service — exchange data and trigger actions in real time. Rather than requiring a human to manually log in to a bank portal to initiate a wire transfer or check an exchange rate, an API allows one system to request this from another automatically, receive a structured response, and act on it — all within milliseconds.

In international payments specifically, the API layer is where much of the actual complexity is managed. A cross-border transfer that appears simple from a user perspective — enter an amount, choose a currency, tap send — involves a sequence of API calls to external services: an identity verification provider to confirm the sender's details, a sanctions database to screen the transaction, a liquidity provider to fetch the current exchange rate, a payment network to route the transfer, and a payout partner to disburse funds to the recipient's account or mobile wallet. Each of these interactions happens through an API, often in parallel, often in under a second. The quality of this API architecture determines the speed, cost, reliability, and compliance integrity of the entire payment experience.

Figure 1: Scale indicators for API-driven international payment infrastructure in 2026.

The traditional architecture for international payments was built around correspondent banking relationships and batch processing systems. A payment initiated on Monday afternoon might be processed in overnight batches, forwarded through one or more correspondent banks, subjected to manual compliance review, and settled on Wednesday — with fees accumulating at each intermediary stop and visibility into payment status limited to periodic status messages. This architecture was not designed for the transaction volumes, speed expectations, or compliance rigour that the modern global payments market requires.

APIs changed this architecture fundamentally by enabling real-time, point-to-point communication between the services that make up a payment stack. Instead of passing a payment instruction through a chain of institutions, each of which processes it sequentially, an API-driven platform can orchestrate multiple services simultaneously. Identity verification, sanctions screening, FX rate fetching, and payment routing can execute in parallel rather than in sequence. The result is not just faster payment processing — it is a fundamentally different operational model where payment companies can compose payment capabilities from best-in-class specialist providers rather than building everything in-house or relying on the bundled services of a single correspondent bank.

This composability is what has enabled the remittance and cross-border fintech industry to expand so rapidly. A new operator can reach 100+ payout countries by integrating with an established payout API network, rather than spending years negotiating bilateral banking relationships with partner institutions in each market. For a detailed view of how API-based remittance infrastructure translates into commercial operational models, the remittance API integration guide provides an in-depth technical breakdown.

Walking through the API call sequence in a typical cross-border payment reveals both how much automation has been achieved and where the remaining complexity lies. Each step in the flow involves one or more API calls to external or internal services, with the responses from each step potentially influencing the logic applied at the next.

Figure 2: Six-stage API call sequence for a cross-border payment — from initiation through KYC, AML screening, FX conversion, routing, and final disbursement. Steps 02–04 typically execute in parallel.

The cross-border payment API ecosystem is not a single technology category — it is a collection of specialised API types, each serving a distinct function in the payment stack. Understanding the landscape helps payment operators and platform builders make better decisions about which APIs to build in-house, which to source from specialist providers, and how to architect integrations that are both functionally capable and resilient under load.

| API Type | Primary Function | Build vs. Buy | Latency Requirement | Regulatory Scope |

|---|---|---|---|---|

| Payment Initiation APIs | Accept and validate payment instructions from front-end applications | Typically built | <200ms | PSD2, Open Banking standards |

| KYC / Identity APIs | Verify customer identity via document checks, biometrics, database lookups | Buy (specialist) | <3 seconds | AML/CTF, data privacy regulations |

| AML / Sanctions APIs | Screen transactions against sanctions lists, PEP databases, risk rules | Buy (specialist) | <500ms | FATF, BSA, AMLD6, AUSTRAC |

| FX / Rate APIs | Fetch live exchange rates, lock rates, calculate conversion amounts | Buy (liquidity provider) | <100ms | FX conduct regulations by jurisdiction |

| Payment Routing APIs | Select optimal network route based on corridor, cost, speed parameters | Typically built or white-label | <200ms | Network-specific rules apply |

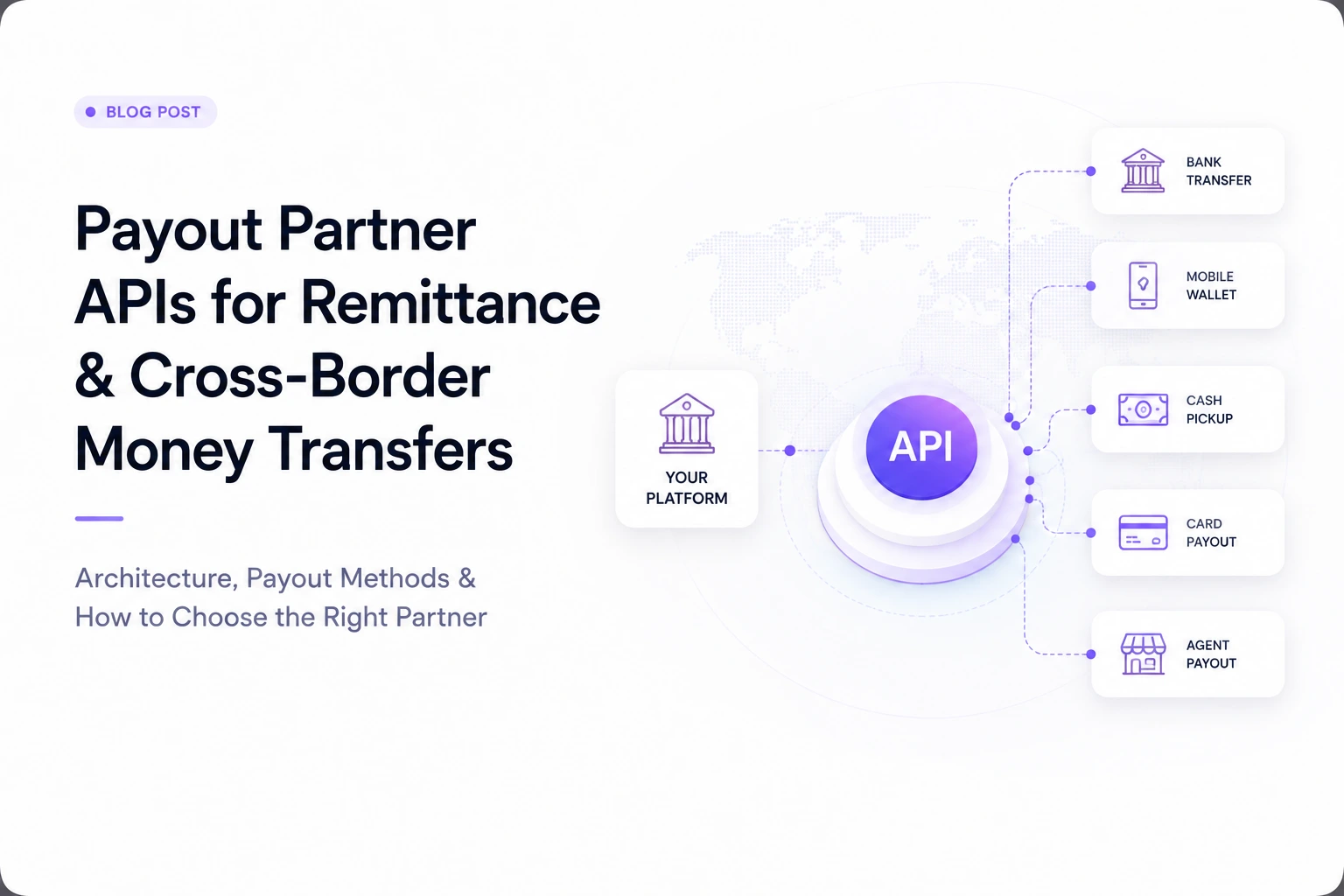

| Payout / Disbursement APIs | Disburse funds to bank accounts, wallets, mobile money, cash agents | Buy (aggregator or direct) | Seconds–minutes | Local payout network regulations |

| Open Banking APIs | Access bank account data and initiate payments with customer consent | Buy (bank or aggregator) | <2 seconds | PSD2, Open Banking UK, CDR (Australia) |

| Webhook / Notification APIs | Push real-time status updates to sender and recipient applications | Typically built | Near real-time | No specific regulation — best practice |

Figure 3: Payment API taxonomy for cross-border payment platforms. Build-vs-buy guidance is indicative — most operators build core orchestration logic and buy specialist compliance, FX, and payout capabilities.

The operational advantages of API-driven payment architecture over traditional correspondent banking and batch processing models are substantial and well-evidenced across the global fintech industry. They are not evenly distributed across all types of operators — the benefits are most pronounced for companies building from scratch or rebuilding legacy platforms, rather than large incumbent banks with deep existing infrastructure investments. For remittance companies, payment fintechs, and challenger banking platforms, however, API-first architecture provides a competitive structural advantage that is difficult to replicate through incremental improvement of older systems.

Speed is the most visible benefit. API-driven payment flows that coordinate verification, routing, and settlement in parallel can complete in seconds what batch-processing architectures took days to execute. This speed improvement is not purely about customer experience — it also reduces foreign exchange exposure windows, lowers the working capital locked in settlement float, and enables refund and error-correction processes to execute faster when problems occur. The transaction lifecycle automation guide covers how payment operators are implementing end-to-end automation across the full settlement cycle.

Cost reduction flows from automation eliminating manual processing steps. Each API call replaces a human action that previously cost staff time, introduced latency, and created error risk. Automated KYC reduces manual document review overhead. Automated AML screening reduces the false positive review burden when well-calibrated. Automated FX rate fetching eliminates the need for treasury staff to manually track and update exchange rates in transaction processing systems. At scale, these automation benefits compound significantly — the marginal cost per transaction on an API-driven platform is substantially lower than on a manually-assisted legacy system, which is why fintech remittance operators have been able to compete aggressively on price against incumbent money transfer operators with larger branch and agent networks.

Global scalability is the third structural benefit. A payment operator that has integrated with a payout API network covering 100+ countries can reach recipients in all those markets without establishing bilateral banking relationships in each jurisdiction. This dramatically reduces the time and capital required for geographic expansion — from years of banking negotiations to weeks of API integration work. For context on how this scalability translates into business model design for remittance operators, see the cross-border payment solutions guide for businesses.

Open Banking represents a structural shift in how payment APIs connect with traditional banking infrastructure. Under Open Banking frameworks — mandated by PSD2 in the European Union, the UK Open Banking standard, and the Consumer Data Right (CDR) framework in Australia — banks are required to expose standardised APIs that allow licensed third-party providers to access account data and initiate payments with the account holder's explicit consent. This regulatory mandate has created a new category of payment capability that sits between traditional banking and fully decoupled fintech infrastructure.

For cross-border payment operators, Open Banking APIs are particularly valuable for funding collection. Rather than requiring customers to push a bank transfer manually or pay by card with its associated processing fees, an Open Banking payment initiates a direct bank-to-bank transfer with the customer's consent, at near-zero incremental cost per transaction. This reduces the average cost of funding collection substantially for high-volume operators. Account verification — confirming that a bank account belongs to the claimed owner before sending a payment — is also available through Open Banking APIs, reducing the risk of misdirected payments and improving payout accuracy. The open banking benefits for remittance operators covers the specific implementation patterns and commercial advantages in detail.

API-driven architecture creates significant operational advantages, but it also introduces a distinct set of technical and regulatory challenges that must be addressed in platform design. Acknowledging these challenges is important because the rapid adoption of API-first payment models has sometimes outpaced the regulatory, security, and integration frameworks needed to make them operate safely at scale.

Figure 4: What API-driven architecture enables versus the challenges operators must actively manage in production payment environments.

Regulatory complexity is the most persistent challenge for API-based international payment platforms. Each jurisdiction in which a payment operator collects, routes, or disburses funds has its own AML requirements, KYC standards, data localisation rules, and licensing obligations. The API layer must implement jurisdiction-specific compliance logic — different transaction monitoring rules for US-origin flows versus EU-origin flows versus Australian flows — while presenting a consistent interface to the application layer above it. This is architecturally non-trivial, and it is one reason why compliance platform providers who can deliver pre-configured, jurisdiction-aware compliance API modules are increasingly valuable partners for operators building or scaling international payment infrastructure.

Cybersecurity at API endpoints is a critical ongoing operational concern. APIs that process payment instructions and access customer financial data are high-value attack targets. Authentication (OAuth 2.0, mTLS), rate limiting, API gateway monitoring, and regular penetration testing are not optional security controls for production payment APIs — they are baseline requirements. API abuse attacks — where fraudulent actors attempt to extract account data or trigger unauthorised payment instructions through poorly secured endpoints — represent a growing threat vector that payment security teams must actively monitor.

The trajectory of API-driven payment infrastructure points toward deeper automation, more sophisticated orchestration, and expanding the categories of value that can be transferred programmatically across borders. Embedded finance — where payment capabilities are built directly into non-financial platforms such as e-commerce marketplaces, logistics software, and enterprise ERP systems — will drive the next wave of API integration demand. Rather than users navigating to a separate payment app, embedded finance APIs bring payment execution into the workflow context where the commercial activity is happening.

Stablecoin payment APIs represent an emerging category that is already operational in some corridors. Platforms that can programmatically issue, transfer, and settle stablecoins as part of a cross-border payment flow — while maintaining full FATF Travel Rule compliance and AML screening — are building capabilities that reduce correspondent banking dependency for specific corridor and customer types. The intersection of stablecoin settlement APIs and traditional fiat payment APIs, managed through a single orchestration layer, is where some of the most commercially significant payment infrastructure development is happening in 2026.

Central Bank Digital Currencies (CBDCs) — already in pilot or live deployment across a growing number of jurisdictions — will eventually require API integration into cross-border payment stacks. CBDC payment APIs are still in early standardisation stages, but operators building payment infrastructure today should track CBDC developments in their primary operating jurisdictions as the interoperability standards that emerge will shape API design requirements over the next several years. For operators evaluating how API-first infrastructure choices integrate with broader platform architecture decisions, the Remittance-as-a-Service model overview explains how platform-level API connectivity translates into commercial remittance operations, and the payment gateway guide for remittance companies covers gateway API selection criteria in depth.

For remittance operators and fintech companies building international payment platforms, the decision of which API capabilities to build in-house versus integrate from a white-label infrastructure provider is one of the most consequential architectural choices they face. Building core orchestration logic, compliance workflows, and payout connectivity from scratch is a multi-year investment that diverts engineering resources from product differentiation. RemitSo's platform provides operators with a pre-integrated API stack that covers the full cross-border payment workflow — from KYC and AML screening through FX conversion, payment routing, and multi-corridor payout disbursement — accessible through a single integration layer.

The platform's compliance API infrastructure covers real-time sanctions screening across 40,000+ records and eight global lists, 55+ configurable transaction monitoring indicators, and KYC/eKYC workflows with tiered EDD capabilities. The payout connectivity layer reaches 100+ countries across bank transfer, mobile wallet, and cash pickup rails — without requiring the operator to build and maintain separate bilateral integrations for each payout market. For technical teams evaluating integration architecture, the platform supports standard REST API integration with webhook callbacks for real-time status notifications, ISO 20022 compatible messaging where applicable, and an operator dashboard for monitoring transaction flows, compliance alerts, and settlement status without requiring direct API interaction for routine oversight. Explore the full RemitSo platform feature set and API capabilities to evaluate how the infrastructure maps to your specific integration requirements.

RemitSo provides the complete API stack that remittance operators and payment fintechs need to launch and scale global cross-border payment operations — compliance built in from day one.

A payment API is a software interface that allows two or more applications to communicate and process financial transactions automatically. In cross-border payments, payment APIs handle the full transaction lifecycle: accepting payment instructions from the sender's application, verifying identity through KYC APIs, screening for AML and sanctions compliance, fetching live exchange rates through FX APIs, selecting payment routes through orchestration APIs, and triggering disbursement through payout APIs. Each API call exchanges structured data in a defined format — typically JSON over HTTPS — and returns a response that the calling system can act on without human intervention.

APIs improve international payments across four dimensions: speed (parallel API execution reduces settlement from days to seconds), cost (automation eliminates manual processing overhead and intermediary fees), transparency (real-time status APIs provide end-to-end payment tracking for senders and recipients), and scalability (API integration with global payout networks enables geographic expansion without bilateral banking agreements). APIs also improve compliance quality by enabling real-time AML screening and KYC verification that runs at transaction speed rather than on manual review cycles, reducing both compliance failure risk and false positive alert volumes when properly calibrated.

Well-implemented payment APIs are highly secure, but security is not an inherent property of the API format — it depends on how APIs are designed, deployed, and maintained. Secure payment APIs use OAuth 2.0 or mutual TLS (mTLS) for authentication, AES-256 encryption for data in transit and at rest, API gateways with rate limiting and request validation, real-time fraud monitoring at the API layer, and regular penetration testing of all exposed endpoints. PCI-DSS compliance requirements apply to APIs that handle payment card data. Operators using third-party payment APIs should evaluate the security certifications and architecture of their API providers — not just the functional capability — before deploying in production.

Open Banking APIs are standardised interfaces that banks are required to expose — under regulatory frameworks such as PSD2 in the EU and the Open Banking standard in the UK — allowing licensed third-party providers to access account data and initiate payments with explicit customer consent. In international payment contexts, Open Banking APIs are primarily used for funding collection (initiating a bank-to-bank transfer directly from the sender's account, avoiding card processing fees) and account verification (confirming account ownership before disbursing a payout). Open Banking reduces the funding cost for remittance operators and improves the accuracy of payout account verification compared to manual bank detail entry.

Yes, in many corridors. Real-time payment APIs connected to instant payment rails — such as SEPA Instant in Europe, UPI in India, PayNow in Singapore, Faster Payments in the UK, and RTP/FedNow in the United States — can complete end-to-end settlement within seconds for eligible transactions. The constraint is not the API architecture but the settlement infrastructure at the destination: real-time settlement is only possible where the receiving country's payment network supports it. For corridors served by legacy batch-processing banking infrastructure, settlement may still take hours or days regardless of how fast the sending-end API layer operates. Payout API aggregators typically provide estimated settlement time data per corridor and payout method, allowing operators to communicate accurate delivery expectations to customers.

Payment APIs for international transfers are most heavily used in fintech remittance platforms (where the entire business model depends on API-orchestrated cross-border payment flows), e-commerce marketplaces with international seller and buyer bases, digital banking and neobank platforms offering cross-border transfer features, SaaS platforms with global subscriber billing requirements, travel booking and hospitality platforms with multi-currency supplier payment needs, gig economy and freelance marketplace platforms disbursing earnings to workers in multiple countries, and enterprise software providers embedding payment capabilities into workflow platforms. Cryptocurrency exchanges also rely heavily on cross-border payment APIs for fiat on-ramp and off-ramp operations.

ISO 20022 is the global financial messaging standard being adopted across major payment infrastructures including SWIFT, SEPA, and most central bank real-time gross settlement systems. Unlike the legacy SWIFT MT message format, ISO 20022 uses a richer XML-based data structure that carries significantly more information alongside each payment — including structured beneficiary details, remittance information, purpose codes, and compliance attributes. For API-driven payment platforms, ISO 20022 compatibility enables richer data to travel alongside cross-border payments, improving straight-through processing rates (fewer transactions requiring manual investigation), better compliance screening outcomes, and cleaner reconciliation at the receiving end. The SWIFT network completed its migration to ISO 20022 for cross-border payments in 2025, making compatibility a practical requirement for operators connecting to major correspondent banking networks.

For most remittance startups and early-stage payment fintechs, a white-label platform with pre-integrated API capabilities is the faster and more capital-efficient route to market. Building a production-grade cross-border payment API stack from scratch — covering KYC integration, AML compliance, FX connectivity, multi-corridor payout routing, and real-time monitoring — typically takes 12–18 months and requires specialist engineering, compliance, and banking relationship resources that most startups do not have. A white-label platform compresses this to weeks of integration work and provides a compliance infrastructure baseline that would take years to build to equivalent depth. The trade-off is flexibility — white-label platforms have defined architectural constraints. Startups should evaluate whether the platform's API capabilities cover their primary use cases before committing, and assess what level of customisation is available as they scale.