One Compliance Failure Can Shut Down Your Entire Money Transfer Business. Here's How to Make Sure It Doesn't.

Not a market downturn. Not a funding drought. Not a stronger competitor. The single biggest existential threat to a money service business today is a compliance failure — one that regulators discover before you do.

It sounds dramatic until you look at what happened in 2025. A year in which a single exchange lost over half a billion dollars to one enforcement action. A year in which the UK’s financial regulator issued nine-figure penalties targeting the exact weaknesses most MSBs know they have but haven’t fixed yet. A year in which the global standard-setter for anti-money laundering rewrote its foundational recommendation to make it clear: paper compliance is no longer acceptable.

If you operate — or are planning to launch — a money transfer business in the cross-border remittance space, this blog is for you. We’re going to walk through what actually went wrong in the biggest enforcement actions of 2025, identify the pattern that connects them all, and show you what a compliance-first infrastructure looks like in practice.

The $504 Million Wake-Up Call

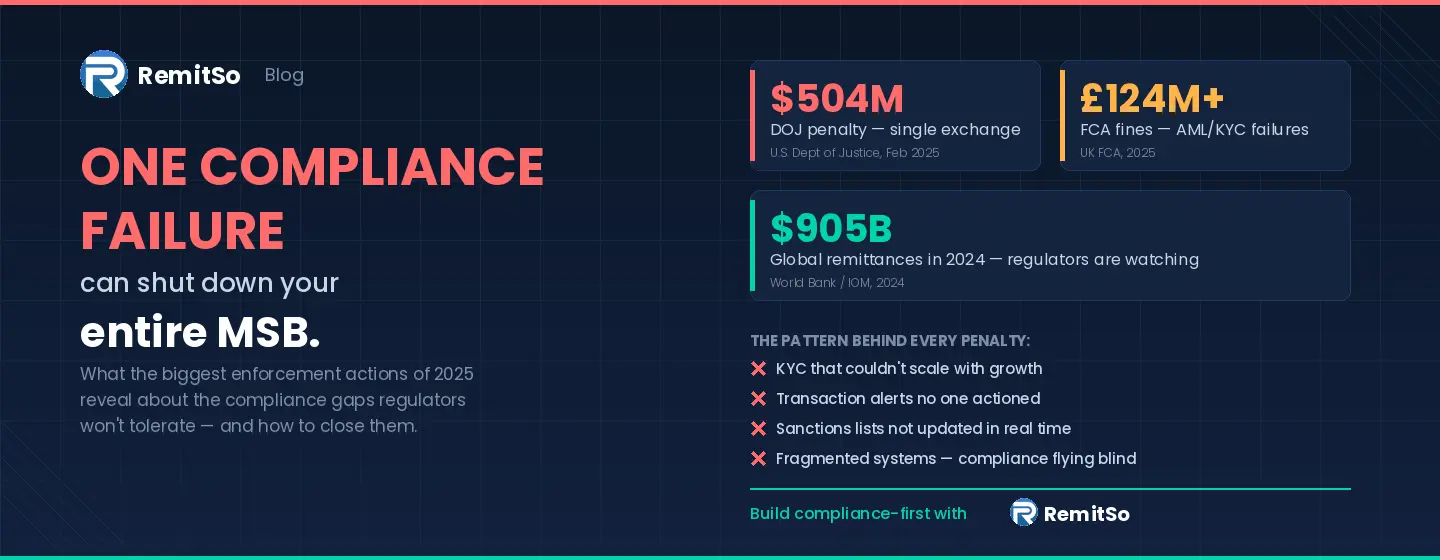

On February 24, 2025, the U.S. Department of Justice announced that a major cryptocurrency exchange had pleaded guilty to operating an unlicensed money transmitting business. The penalty: over $504 million — comprising $420.3 million in criminal forfeiture and $84.4 million in fines.

The exchange in question was one of the largest in the world. Billions of dollars in daily trading volume. A global brand. Sponsorship deals with Formula 1 teams. None of that mattered.

According to the DOJ’s press release, the platform had — for seven years — knowingly served U.S. customers without registering as a money services business with FinCEN. It failed to implement adequate know-your-customer controls. It didn’t file suspicious activity reports. Internal documents revealed that employees actively advised customers to falsify identification information to bypass compliance checks.

The result: Over $5 billion in suspicious transactions flowed through the platform undetected. The business didn’t fail because of a single bad actor. It failed because compliance was structurally absent from its growth model.

What makes this case instructive for MSBs isn’t the scale — it’s the pattern. The exchange was built to move money fast, not to move it safely. That distinction is precisely what regulators are now penalising.

Source: U.S. Department of Justice, Southern District of New York, Press Release, February 24, 2025

The UK’s £124 Million Enforcement Blitz

Across the Atlantic, the UK’s Financial Conduct Authority had its own reckoning in 2025. By year-end, the FCA had published over £124 million in fines — with the overwhelming majority linked to anti-money laundering and financial crime control failures.

The penalties weren’t limited to small or niche players:

- A major building society was fined for systemic weaknesses in transaction monitoring — controls that failed to flag millions of pounds in fraudulent activity, including payments linked to Covid support scheme abuse.

- A global bank was penalised for financial crime risk management gaps that persisted over several years, particularly in the oversight of high-value corporate banking relationships.

- A fast-growing digital bank was fined for letting rapid customer acquisition outpace the maturity of its compliance infrastructure — a failure the FCA described in stark terms.

Three very different institutions. Three very different business models. The same underlying story: compliance systems that could not keep up with the speed, scale, and complexity of the business they were supposed to protect.

The lesson for MSBs: If the FCA will fine a building society £44 million and a digital bank £21 million for these failures, smaller operators will not receive a lighter touch. The regulatory expectation is increasingly that all firms demonstrate proportionate compliance.

Source: UK Financial Conduct Authority, 2025 Fines

FATF’s February 2025 Update: Compliance Must Work in Practice

The Financial Action Task Force — the intergovernmental body that sets global AML standards — added further weight to this shift in February 2025, when it updated Recommendation 1 and its Interpretive Note.

The update reinforced a critical principle: AML, counter-terrorist financing, and counter-proliferation financing controls must be implemented through a proportionate, risk-based approach. Controls must be effective in practice, not merely documented in policy manuals.

FATF also drew an explicit link between financial inclusion and financial crime prevention. The updated guidance encourages countries and the private sector to bring more people into the formal financial system — arguing that this strengthens the effectiveness of AML controls by reducing the size of informal economies where criminals operate undetected.

For MSBs, this matters for two reasons. First, regulators globally will increasingly judge compliance programmes by their outcomes — not their documentation. Second, it validates the role that technology-enabled, compliance-first money transfer businesses can play in expanding financial access while maintaining integrity.

Source: FATF, Updated Recommendation 1 & Financial Inclusion Guidance, February 2025

The Pattern Behind Every Penalty

When you strip away the specifics — the jurisdictions, the firm names, the dollar amounts — a remarkably consistent pattern emerges. The same four failures appear in virtually every major AML enforcement action of 2025:

- KYC that couldn’t scale with growth — Customer due diligence that worked at low volumes but collapsed under growth. Exchanges that allowed accounts with minimal identity verification. MSBs that processed transfers without verifying source of funds for high-risk corridors.

- Transaction monitoring that generated alerts no one actioned — Systems that were technically operational but practically ineffective. Poorly calibrated thresholds. Generic rules. Overwhelmed compliance teams. Genuine suspicious activity drowning in false positives.

- Sanctions screening that wasn’t updated in real time — Firms that screened at onboarding but didn’t re-screen against updated lists. New designations published weekly across OFAC, EU, UN, and HMT went unmatched.

- Fragmented systems that left compliance teams flying blind — Customer data in one system, transaction data in another, alerts in a third, reporting in a fourth. No single view. No audit trail from trigger to resolution.

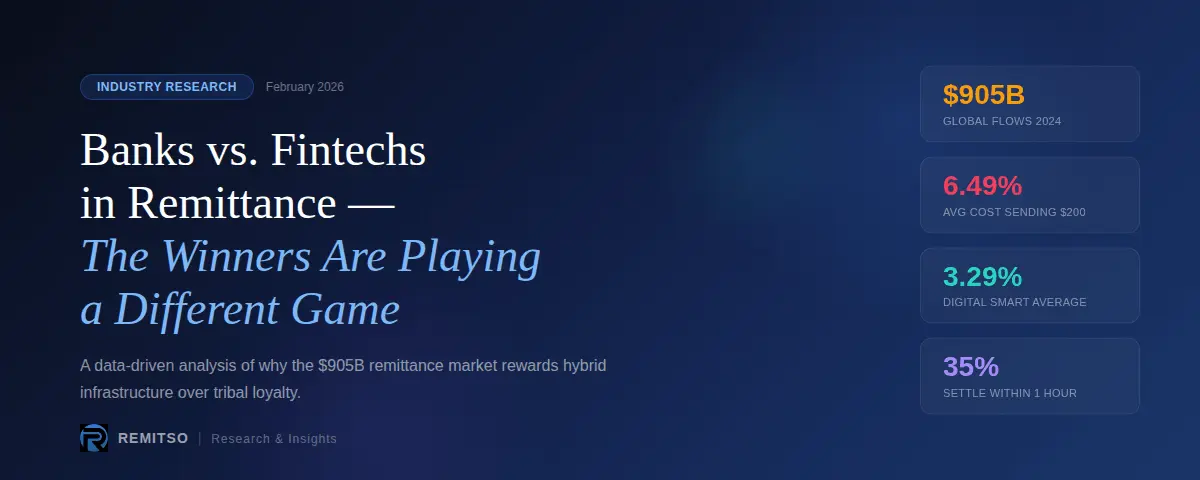

$905 Billion Under the Spotlight

The global remittance market hit $905 billion in 2024, according to World Bank estimates — a 4.6% increase over 2023. Remittances to low- and middle-income countries alone reached $685 billion, exceeding both foreign direct investment and official development assistance.

These volumes represent a lifeline for families, communities, and entire economies. But they also represent risk that regulators are keenly aware of. The cross-border money transfer corridor is, by its nature, exposed to the typologies regulators care most about: structuring, layering, sanctions evasion, trade-based money laundering, and the financing of terrorism.

The World Bank’s Remittance Prices Worldwide report for Q1 2025 shows the global average cost of sending $200 remains at 6.49% — more than double the UN Sustainable Development Goal target of 3%. Banks remain the most expensive channel at 14.55%. This means there is enormous market opportunity for technology-enabled MSBs that can move money faster, cheaper, and more transparently.

But that opportunity only exists for operators that can do it compliantly. The MSBs that will capture this market aren’t the ones with the lowest fees. They’re the ones that can demonstrate to regulators, banking partners, and customers that their compliance infrastructure is robust, scalable, and audit-ready.

Sources: World Bank / IOM Migration Data Portal; World Bank, Remittance Prices Worldwide, Issue 53, Q1 2025

Compliance Is Not a Cost Centre. It’s Your Operating System.

This is the mindset shift that separates the MSBs that survive from the ones that scale.

Too many money transfer businesses treat compliance as a burden to be minimised — a checkbox exercise to satisfy a regulator, a cost line to be squeezed. They hire a compliance officer, buy a screening tool, draft a policy, and move on. The result is a compliance function that looks adequate on paper but can’t withstand the first real stress test: a regulatory examination, a suspicious activity spike, or a banking partner’s enhanced due diligence review.

The operators that thrive take a fundamentally different approach. They build compliance into the architecture of the business — the onboarding flow, the transaction engine, the agent management system, the reporting layer. Compliance isn’t something that happens alongside the business; it’s how the business operates.

How RemitSo Helps MSBs Build Compliance-First Operations

At RemitSo, we’ve built an enterprise-grade platform specifically for the cross-border money transfer space. It’s designed for MSBs, fintechs, exchange houses, and banks that need to move money across borders compliantly, at scale.

Here’s how our infrastructure maps directly to the compliance challenges outlined above:

- Automated KYC & Onboarding Digital identity verification that scales with your customer base. Biometric verification, document upload, risk-based tiering, and real-time identity checks built into the customer journey — not bolted on afterwards. This directly addresses the most common enforcement finding of 2025: KYC processes that couldn’t keep up with growth.

- Real-Time AML Transaction Monitoring Continuous transaction screening — not in batches, not overnight, not weekly. Suspicious patterns flagged in real time, with configurable rules and thresholds calibrated to your specific risk profile and corridor mix. Your compliance team works from actionable alerts, not a backlog of unreviewed flags.

- Integrated Sanctions Screening Live checks against OFAC, EU, UN, and HMT sanctions lists — automatically updated as new designations are published. Screening at onboarding and on an ongoing basis, so you’re not relying on a point-in-time check from six months ago.

- Centralised Compliance Dashboard One view. Every customer. Every transaction. Every alert. Every report. No data silos. No toggling between systems. Our dashboard gives compliance officers, MLROs, and senior management a unified, real-time picture of the business’s risk posture.

- Audit-Ready Reporting Every decision, flag, escalation, and resolution is logged and traceable. When the regulator asks “why was this alert closed?” — you have the answer, with a timestamp and an audit trail. This is the difference between a finding and a clean bill of health.

- 100+ Country Payout Network Pre-integrated payout corridors so you can expand into new markets without months of manual partner due diligence and API integration per corridor. Scale your corridor coverage compliantly and quickly.

Build It Right From Day One

We built RemitSo because we saw the same story repeat itself too many times. Promising MSBs — with good teams, real customers, and genuine demand — either cutting corners on compliance to move fast, or drowning in manual processes trying to do it right.

Neither path leads to sustainable growth.

The enforcement actions of 2025 made one thing clear: regulators are not interested in your intentions. They’re interested in your systems, your controls, and your outcomes. The bar is rising. The penalties are real. And the opportunity — in a $905 billion market with transaction costs still double the global target — is enormous for operators that get it right.

Compliance isn’t what slows you down. It’s what lets you keep going.

Sources (Open-Access Government & International Organisation Data)

- U.S. Department of Justice, SDNY — Press Release, February 24, 2025 — justice.gov/usao-sdny

- UK Financial Conduct Authority — 2025 Fines — fca.org.uk/news/news-stories/2025-fines

- Financial Action Task Force (FATF) — Updated Recommendation 1 & Financial Inclusion Guidance, February 2025 — fatf-gafi.org

- World Bank — Remittance Prices Worldwide, Issue 53, Q1 2025 — remittanceprices.worldbank.org

- IOM Migration Data Portal — Remittances Overview — migrationdataportal.org/themes/remittances

- World Bank Blog — Remittance Flows to LMICs, December 2024 — blogs.worldbank.org