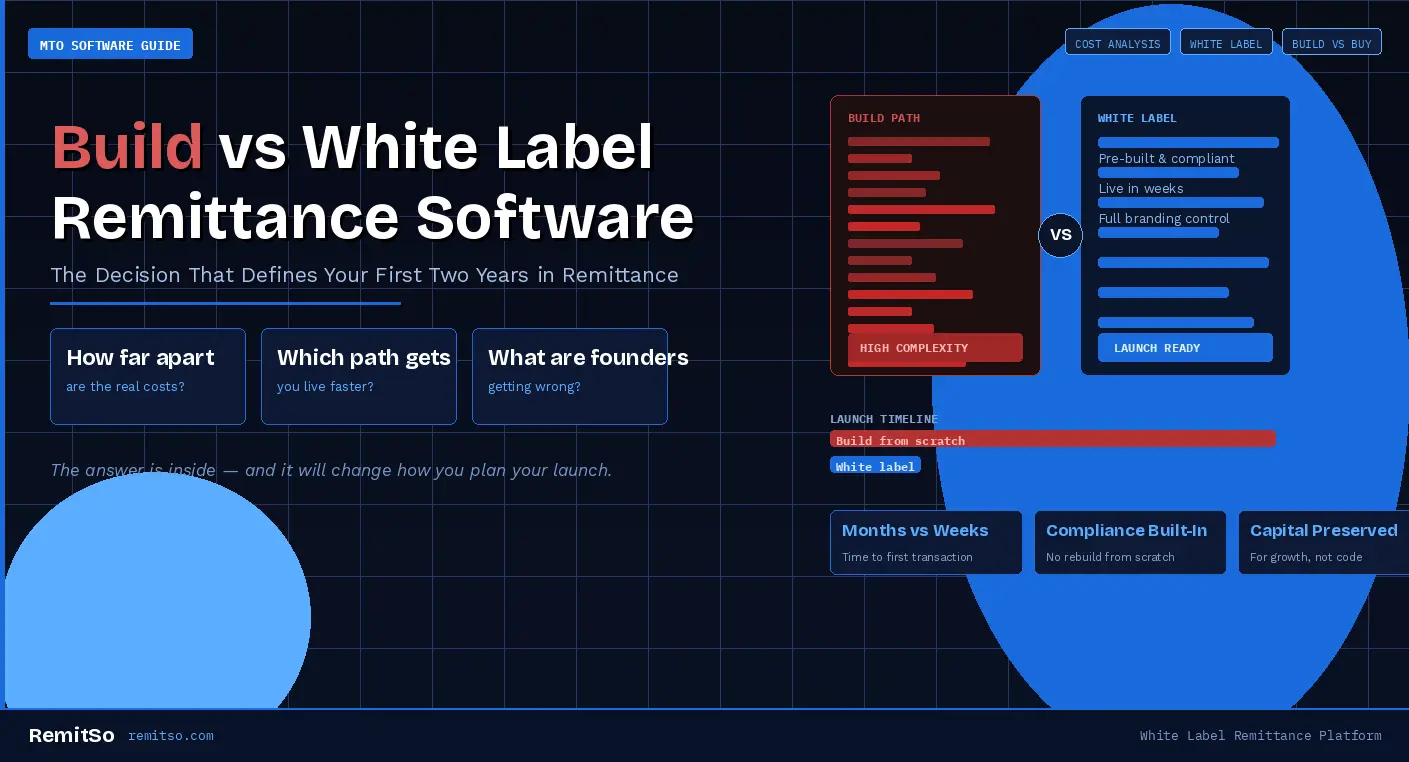

Every founder entering the remittance space faces the same foundational decision early: do we build our own platform, or do we launch on a white label solution? It feels like a strategic question, but it is equally — and perhaps more urgently — a financial one. The costs of getting this decision wrong are not abstract. They show up as missed market windows, compliance failures that halt operations, technical debt that compounds for years, and capital burn that leaves nothing for customer acquisition. This guide sets out the real, unvarnished cost comparison between building remittance software from scratch and launching on a white label platform — so you can make the decision with clear numbers, not assumptions.

In This Article

The build vs white label decision in remittance software is not a technology choice — it is a capital allocation choice. The path you take determines how your first £500,000 or $500,000 of operating capital is spent, how quickly you reach a revenue-generating state, and how much runway you have to acquire customers and prove the business model before your next funding decision or cash flow inflection point.

What makes this decision particularly consequential in remittance versus other fintech verticals is the regulatory complexity layered on top of the technical complexity. Building a payment or remittance platform isn't just a software engineering project — it's an engineering project that must simultaneously satisfy the requirements of financial regulators, anti-money laundering frameworks, sanctions screening obligations, and data protection laws across multiple jurisdictions. Each of these adds cost, time, and specialist expertise to the build path that many founders dramatically underestimate at the outset.

Founders who choose to build typically do so for one of three reasons: they believe their product requires capabilities that no white label platform can provide; they are concerned about long-term vendor dependency; or they underestimate the full cost of building. The first two reasons are legitimate considerations that deserve serious analysis. The third — which is the most common driver — is a planning failure that has ended many promising remittance businesses before they reached meaningful scale.

Let's be precise about what "building from scratch" actually means in the remittance context. A functional, compliant, production-ready remittance platform requires a minimum viable feature set that is more extensive than most founders initially scope. Stripping it down to the core, a launch-ready remittance platform needs: a customer-facing interface (web and mobile), a backend transaction engine, a compliance and AML rules engine, payout partner integrations, FX rate management, a back-office administration system, KYC and identity verification integration, banking and payment gateway integration, and the cloud infrastructure to run it all securely at production grade.

Each of these components has a development cost, an integration cost, and an ongoing maintenance cost. Here is a realistic breakdown of what building this stack costs in today's market, based on industry benchmarks for fintech engineering teams working at professional rates in the UK, Europe, and equivalent markets.

| Component | Estimated Cost Range | Notes |

|---|---|---|

| Core backend & transaction engine | $80,000–$150,000 | Senior engineers, 4–8 months build time |

| Web application (customer-facing) | $30,000–$60,000 | Full-stack frontend development |

| iOS & Android mobile apps | $60,000–$120,000 | Native or cross-platform, per app store guidelines |

| AML & compliance rules engine | $40,000–$80,000 | Requires specialist fintech compliance knowledge |

| KYC integration | $15,000–$30,000 | API integration + workflow design |

| Payout partner integrations | $25,000–$50,000 | Per partner, plus ongoing maintenance |

| Back-office admin panel | $20,000–$40,000 | Transaction management, reporting, controls |

| Cloud infrastructure setup | $10,000–$25,000 | Security architecture, compliance-grade hosting |

| Security audit & penetration testing | $15,000–$35,000 | Required pre-launch for regulatory approval |

| Total Year 1 Build Cost | $295,000–$590,000 | Before ongoing maintenance costs |

Figure 1: Realistic cost breakdown for building a remittance platform from scratch in Year 1

These figures represent professional-grade development at sustainable team rates. They do not include the cost of the engineering team's management overhead, the product manager needed to coordinate the build, the QA engineer required to validate a financial platform, or the DevOps specialist needed to maintain production infrastructure. Adding these roles to a build team — either as full-time hires or contractors — typically adds $80,000–$150,000 to Year 1 costs before a single customer transaction is processed.

The component costs above are the ones most founders eventually identify in their planning. What consistently catches build-path operators off guard are the costs that emerge during and after development — the expenses that don't appear in a software development statement of work but materialise inevitably in a regulated financial services context.

Figure 2: Four hidden cost categories in the build path that consistently derail MTO timelines and budgets

White label remittance platforms provide a pre-built, fully featured technology stack that an operator licenses, brands, and deploys as their own product. The cost structure is fundamentally different from the build path — shifting from large upfront capital expenditure to a more predictable combination of a setup fee and ongoing operational costs.

The pricing model for white label platforms varies significantly across providers. Some charge purely on a per-transaction basis. Others use a monthly subscription model. The most transparent and founder-friendly models combine a one-time implementation fee with a tiered monthly operational cost that scales with transaction volume — so the operator's platform costs are correlated with revenue rather than fixed regardless of performance.

| Cost Component | Typical Range (Market) | What It Covers |

|---|---|---|

| One-time setup / deployment fee | $5,000–$25,000 | Branding, configuration, cloud setup, app store submission |

| Monthly platform fee (early stage) | $99–$299/mo | Platform maintenance, back-office support, monitoring |

| Monthly platform fee (growth stage) | $299–$599/mo | Scales with transaction volume, includes dev support |

| Cloud infrastructure | At cost / pass-through | AWS or equivalent — full operator ownership |

| Third-party integrations (KYC, payout) | Vendor-direct pricing | Pre-integrated, operator pays provider directly |

| Estimated Year 1 Total Cost | $8,000–$30,000 | Including setup + 12 months operational fees |

Figure 3: Typical white label remittance platform cost structure — Year 1 total significantly lower than build path

The critical distinction is that the white label path shifts capital from platform development to business development. The $250,000–$500,000 that would otherwise be consumed building infrastructure can instead fund licensing, compliance operations, customer acquisition, corridor development, and the commercial relationships — banking, payout partnerships, FX providers — that actually determine whether the business succeeds in the market.

Every cost comparison between build and white label that focuses only on direct expenditure misses the most important number: the cost of time. In a competitive remittance corridor, every month you are not in market is a month your competitors are acquiring the customers you plan to serve. More critically, it is a month of operational expenditure — salaries, rent, licensing fees, professional services — with zero revenue to offset it.

Consider a simple model. An MTO with a team of four people, modest office costs, and professional services retainers is spending approximately $30,000–$50,000 per month before any customer revenue. If the build path takes 18 months to reach live transactions and the white label path takes 6 weeks, the difference is roughly 16 months of operational burn. At $40,000 per month, that is $640,000 in additional operating costs — before accounting for any difference in direct platform costs.

Figure 4: Time-to-market gap between build and white label paths — and the operational cost of that gap

Time-to-market also has a strategic cost that doesn't appear in any spreadsheet. The remittance market is not static. Corridors become more or less competitive. Regulatory windows open and close. Banking relationships that are available today may not be accessible in 18 months. Partnerships that make commercial sense now are time-sensitive. The operator who reaches market in 6 weeks can validate their commercial assumptions, iterate on pricing and corridors, and begin building transaction history — the data that banks and regulators use to assess the business — while the build-path operator is still in development.

One dimension of the cost comparison that deserves its own analysis is compliance infrastructure. This is the area where the gap between build and white label is perhaps most underappreciated — and where the cost of getting it wrong is highest.

A regulated remittance platform must implement a functioning AML transaction monitoring system, sanctions screening against current watchlists (OFAC, HMT, UN, EU), a customer risk rating framework, a suspicious activity reporting workflow, and audit trails that satisfy regulatory examination standards. Building each of these components from scratch requires not just software development but specialist compliance technology expertise — a combination that is expensive and genuinely scarce in the market.

Figure 5: Compliance infrastructure comparison — build from scratch vs white label platform approach

To make the comparison concrete and decision-useful, here is a three-year total cost of ownership model comparing a realistic build-from-scratch scenario against a white label deployment. These figures represent a mid-market MTO targeting one primary send market with three to five receive corridors, operating at professional standards with appropriate compliance infrastructure.

| Cost Category | Build From Scratch (3yr) | White Label Platform (3yr) |

|---|---|---|

| Platform development / setup | $295,000–$590,000 | $7,499–$25,000 |

| Ongoing engineering & maintenance | $180,000–$360,000 | $3,564–$17,964 |

| Compliance infrastructure build | $60,000–$120,000 | Included in platform |

| Cloud infrastructure (3yr) | $30,000–$80,000 | At cost / pass-through |

| Security audits (annual) | $45,000–$105,000 | Shared / reduced |

| Operational burn from delayed launch | $480,000–$960,000 | Minimal (weeks not months) |

| Estimated 3-Year Total | $1.1M–$2.2M+ | $50,000–$120,000 |

Figure 6: Three-year total cost of ownership comparison — build from scratch vs white label platform deployment

This guide has focused on the cost case for white label, but intellectual honesty requires acknowledging that building is the right choice in some circumstances. The decision framework should be clear rather than one-sided.

Figure 7: Five conditions that justify a build-from-scratch approach — all five should be present, not just one or two

Building makes strategic sense when all five of these conditions are present: the product genuinely requires technical capabilities unavailable in any white label platform; the business has already proven revenue at scale and is expanding rather than launching; there is an in-house engineering team with fintech compliance experience; regulatory approval is already secured; and the capital runway exceeds $2M with significant headroom after build costs. If any of these conditions is absent — particularly capital runway and engineering expertise — the risk-adjusted case for building is very difficult to justify.

A third path that many mature operators take is worth noting: launching on white label, proving the business model, and then migrating to proprietary infrastructure or purchasing the source code once transaction volumes justify the investment. This sequenced approach — white label first, build when profitable — is increasingly the strategy of well-capitalised operators who want both speed-to-market and long-term infrastructure independence.

One of the consistent frustrations founders encounter when evaluating white label remittance platforms is pricing opacity. Many providers require a sales call before disclosing any numbers, which makes early-stage financial planning unnecessarily difficult. The comparison above uses industry ranges, but actual pricing decisions require actual numbers.

RemitSo publishes its PaaS pricing transparently — a one-time platform deployment fee starting at $7,499 (covering web, iOS, and Android deployment, admin panel setup, and cloud configuration), followed by a monthly operational model that starts at $99 per month for back-office platform support and scales with transaction volume. The monthly tier model is explicitly designed so that platform costs are correlated with business scale — operators at early stages pay entry-level rates, and the cost structure grows only as the business generates the revenue to support it. Cloud infrastructure is passed through at cost with full operator ownership, and third-party integrations — KYC providers, payout networks — are pre-integrated and priced direct with the vendors.

For founders who reach a stage where infrastructure independence becomes a genuine strategic priority, RemitSo also offers source code licensing — allowing operators to transition from a managed platform to full codebase ownership when the business economics support it.

Building a production-ready remittance platform from scratch typically costs between $295,000 and $590,000 in direct development costs in Year 1 alone — covering the backend transaction engine, customer-facing web and mobile applications, AML and compliance rules engine, KYC integration, payout partner integrations, back-office admin panel, cloud infrastructure, and security auditing. This figure does not include the cost of product management, QA, DevOps, or ongoing maintenance after launch, which typically adds $60,000–$150,000 per year. When operational costs during the build period are factored in, the true 3-year cost of the build path typically exceeds $1M.

White label remittance platform costs vary significantly by provider. A one-time setup or deployment fee typically ranges from $5,000 to $25,000, covering branding, configuration, cloud setup, and app store submission. Ongoing monthly operational costs typically range from $99 to $499 per month depending on transaction volume and the level of support included. Total Year 1 costs — setup plus 12 months of monthly fees — typically fall between $8,000 and $30,000, making white label dramatically more capital-efficient than building from scratch, particularly at the launch and early-growth stage.

Building remittance software from scratch typically takes 12–24 months from project initiation to first live customer transaction, based on industry benchmarks for financial services platform development. This timeline accounts for development, compliance architecture, security auditing, regulatory review, and app store approval processes. A white label platform, by contrast, can typically be deployed and live within 4–8 weeks — a timeline gap of 10–18 months that represents significant additional operational costs and a major disadvantage in competitive market positioning.

No — the defining characteristic of white label software is that it is fully branded as the operator's own product. Customers see only the operator's brand, not the underlying platform provider. The operator owns the customer relationship, the customer data, and the brand identity. Leading white label platforms allow complete visual customisation — app icons, colour schemes, branding, and interface design — so that the product is indistinguishable from a bespoke build from the customer's perspective. Cloud infrastructure is also typically deployed under the operator's own accounts, ensuring full data sovereignty.

Yes — white label remittance platforms are designed specifically for use by regulated money transfer operators and comply with the technical requirements of FCA, FinCEN, AUSTRAC, FINTRAC, and equivalent regulatory frameworks. The compliance infrastructure — AML rules engine, sanctions screening, audit logging, customer risk rating — is pre-built and maintained by the platform provider. Importantly, regulators have become increasingly familiar with white label deployments, and platforms with a track record of existing licensed operator deployments provide stronger regulatory evidence than an untested bespoke build during the licensing process.

Yes — and this sequenced approach is increasingly common among well-capitalised operators. Launching on a white label platform allows an MTO to prove its business model, build transaction history, secure its regulatory position, and establish commercial relationships — all before committing to the capital and operational overhead of a proprietary build. Once the business reaches sufficient scale and generates the revenue to support a custom engineering investment, migration to a proprietary system or purchase of source code from the white label provider becomes a viable and rational next step. Many providers, including those offering source code licensing options, explicitly support this migration path.

When evaluating white label remittance platforms, the most important criteria are: pricing transparency (is the full cost structure published, or does it require a sales call?); compliance depth (does the platform include a production-grade AML engine, sanctions screening, and audit infrastructure?); existing operator track record (how many licensed operators are live on the platform, and in which jurisdictions?); infrastructure ownership (is cloud infrastructure deployed under your accounts with full data sovereignty?); time-to-market (what is the realistic deployment timeline based on existing client deployments?); and migration options (does the provider offer source code licensing for operators who want to transition to proprietary infrastructure?).

The 3-year total cost of ownership for a white label remittance platform — including setup fee, monthly operational fees, and cloud infrastructure pass-through — typically falls between $50,000 and $120,000 for a mid-market MTO operating at professional standards. This compares to an estimated $1.1M–$2.2M for the equivalent build-from-scratch path when development costs, ongoing engineering maintenance, compliance infrastructure build, and operational burn during the delayed launch period are all included. The capital difference — $1M+ over three years — represents the funds available for customer acquisition, corridor development, compliance operations, and commercial relationships when the white label path is chosen.