Transaction monitoring in Australia's cross-border payments sector is widely misunderstood — even by operators who have been AUSTRAC-regulated for years. The most common misconception is that filing Threshold Transaction Reports when cash reaches $10,000 AUD is the primary monitoring obligation. It is not. TTRs are the floor, not the ceiling. AUSTRAC's genuine expectation — backed by enforcement action against some of Australia's largest financial institutions — is a continuously operating, risk-based monitoring system that detects suspicious behaviour across the full range of transaction types, amounts, corridors, and customer profiles that a remittance or cross-border payment business handles every day. This guide explains what effective transaction monitoring actually looks like for Australian remittance operators and cross-border payment service providers, why threshold-only systems consistently fail in this sector, and how to build a monitoring programme that satisfies AUSTRAC's risk-based standard while remaining operationally realistic for a fast-moving payments business.

In This Article

Cross-border payment and remittance businesses occupy a unique position in the Australian financial crime risk landscape. They move money across jurisdictions by design — that is the entire value proposition. Every transaction by definition involves at least two countries, two regulatory frameworks, and a transfer of value that crosses the AML/CTF control boundary between them. The World Bank estimates that global remittance flows exceeded USD 800 billion annually in recent years, with Australia representing a significant sending market across corridors to South and Southeast Asia, the Pacific, the Middle East, and Africa. FATF consistently identifies money or value transfer services as one of the highest-risk categories of financial service for money laundering and terrorism financing exposure.

AUSTRAC's own National Risk Assessment identifies remittance and cross-border payment services as a priority sector precisely because of this structural exposure. The combination of high transaction volumes, multiple jurisdictions, diverse customer profiles, varied payment channels, and the frequent involvement of cash at origin or at payout creates a monitoring environment that is inherently more complex than domestic payment processing. A transaction monitoring system designed for a domestic bank's account-to-account transfers is structurally inadequate for a remittance operator processing hundreds of daily transfers across twenty corridors to counterparties with highly variable AML/CTF frameworks of their own.

Figure 1: Four structural characteristics of cross-border payments that create elevated ML/TF risk and demand monitoring beyond simple thresholds

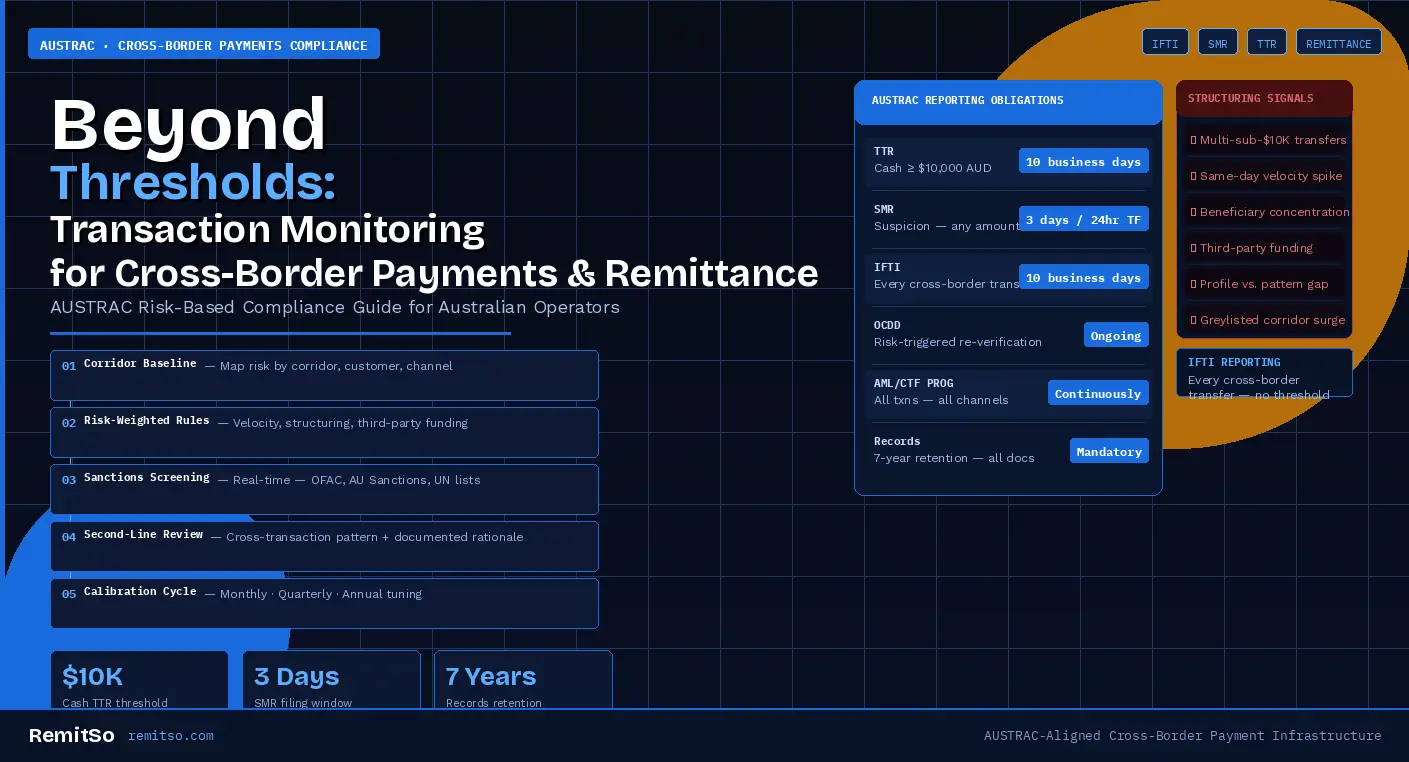

AUSTRAC's monitoring requirements for cross-border payment and remittance operators flow from the AML/CTF Act 2006 and the rules made under it. The core obligation is that reporting entities must have and comply with an AML/CTF programme that includes systems and controls for ongoing monitoring of their customers and transactions. The word "ongoing" is doing significant work in that requirement — it means monitoring must operate continuously, not just at onboarding or when a transaction hits a threshold.

| Obligation | Trigger | Timeframe | Filed With |

|---|---|---|---|

| Threshold Transaction Report (TTR) | Cash transaction of $10,000 AUD or more | Within 10 business days | AUSTRAC |

| Suspicious Matter Report (SMR) | Suspicion of ML, TF, or proceeds of crime — any amount | 3 business days (24 hrs for TF) | AUSTRAC |

| International Funds Transfer Instruction (IFTI) | Every cross-border electronic funds transfer — in or out | Within 10 business days | AUSTRAC |

| Ongoing Customer Due Diligence | Triggered by risk indicators, behaviour change, or periodic review | Risk-based — no fixed interval | Internal records — 7 years |

| AML/CTF Programme Monitoring | Continuously — all transactions, all channels | Ongoing | Internal — AUSTRAC examination |

Figure 2: AUSTRAC's core monitoring and reporting obligations for cross-border payment and remittance operators — triggers, timeframes, and filing requirements

The International Funds Transfer Instruction (IFTI) reporting obligation is one that many newer operators underestimate in its scope. Every cross-border electronic transfer — whether outbound from Australia or inbound — must be reported to AUSTRAC within ten business days. For a remittance operator processing hundreds of transfers daily, this is not an administrative footnote: it is a significant compliance infrastructure requirement. IFTI reports must include sender and receiver information, the originating and destination financial institutions, and the transfer amount and currency. AUSTRAC mines IFTI data extensively for financial intelligence — it is one of the primary datasets through which the regulator identifies emerging ML/TF patterns and typologies in the Australian cross-border payments market.

The SMR obligation is where most operators' monitoring programmes are most deficient. An SMR must be filed within three business days of forming a suspicion — not three days after a compliance review confirms the suspicion, and not three days after the transaction settles. The clock starts when any responsible person in the business forms a reasonable suspicion. A frontline staff member who identifies something wrong at the point of customer interaction has started the timer. This means the monitoring framework must be designed to capture and escalate suspicions rapidly — not to conduct lengthy investigations before deciding whether to report.

The appeal of a threshold-based monitoring model is obvious — it is simple to implement, easy to explain to staff, and generates a clear, auditable output in the form of TTR filings. But for cross-border payment and remittance operators, threshold monitoring is structurally inadequate as a primary compliance mechanism for three interconnected reasons.

Figure 3: Threshold-only monitoring vs risk-based monitoring — the structural differences that determine AUSTRAC compliance

The most critical failure mode of threshold monitoring in the remittance context is its blindness to structuring. Structuring — deliberately breaking a larger transfer into multiple smaller transactions to avoid the $10,000 reporting threshold — is one of the most well-documented ML techniques in the remittance sector. A customer who makes five transfers of $1,900 AUD on the same day to the same beneficiary through the same or related channels is conducting a transaction of $9,500 AUD in economic substance. A threshold-only model sees five small transactions. A risk-based model with velocity rules and linked-party analysis sees a structuring pattern that warrants investigation and potentially an SMR.

The second failure mode is channel blindness. The $10,000 threshold applies to cash transactions. But remittance fraud, trade-based money laundering, and terrorism financing do not limit themselves to cash. Digital transfers, bank-funded remittances, and card-funded payments all carry ML/TF risk — and a monitoring system anchored to a cash threshold entirely misses the risk profile of these payment channels. AUSTRAC examines the full monitoring programme, not just the TTR filing rate, and a programme with no controls on non-cash channels will not survive examination.

Most compliance teams approach transaction monitoring with the wrong first questions — focusing on what threshold to set, what system to buy, or how many staff to assign to alert review. These are operational questions that belong later in the design process. Before any monitoring rule is written, five foundational questions must be answered, because without these answers any system built will be calibrated to the wrong baseline and will generate alerts that are either meaningless or miss the genuine risks.

A remittance operator focused on Australia-to-Philippines transfers has a different transaction baseline from one focused on Australia-to-India or Australia-to-UAE. Average transaction sizes differ by corridor. Typical transfer frequencies differ by customer demographic. Payment method mix — cash, bank transfer, card — differs by customer type and corridor. Seasonal patterns during festival periods, harvest seasons, and family events differ by destination country. A monitoring framework built on generic industry benchmarks rather than the specific operator's own transaction data will be miscalibrated from day one. The starting point must always be a genuine analysis of your own historical transaction data, segmented by corridor, customer type, payment method, and time period.

Multiple transfers to the same beneficiary within a short window is entirely normal for a customer supporting family members abroad — and entirely consistent with structuring if the amounts are calibrated to sit just below a reporting threshold. The behaviour is identical; the context distinguishes risk from routine. A customer who regularly sends $500 per fortnight to the same beneficiary in the Philippines has a clear, stable pattern. A customer who sends $1,900 five times in one week for the first time, all to the same account, has a different profile entirely. Effective monitoring rules are designed around contextual deviation from established patterns, not around the surface behaviour in isolation.

The answer for most remittance operators is cross-transaction pattern analysis. Onboarding controls receive significant investment because they are visible — a customer must pass KYC before a transaction can proceed. Transaction-level screening against sanctions and PEP lists is well understood. But the analysis that connects individual transactions over time, across multiple customers, across multiple accounts, and across multiple corridors to identify coordinated patterns — layering, smurfing, trade-based ML, third-party funding arrangements — is where most operators' monitoring programmes have the largest gaps and where AUSTRAC's examination focus is increasingly directed.

Not all remittance corridors carry the same ML/TF risk. Transfers to FATF-greylisted jurisdictions, to countries with active terrorist financing designations, or to payout partners with documented AML control weaknesses require a higher level of monitoring scrutiny than transfers to well-regulated jurisdictions through well-screened payout networks. The monitoring system must apply corridor-level and counterparty-level risk weights — not treat a transfer to the Netherlands and a transfer to a greylisted jurisdiction as equivalent transactions requiring the same level of monitoring intensity.

If more than 85–90% of alerts are closed as false positives, the monitoring rules are miscalibrated. High false positive rates are not a sign of robust monitoring — they are a sign of poorly designed rules that create alert fatigue. Alert fatigue is one of the most dangerous compliance failure modes in high-volume operations, because it is the condition under which genuine suspicious activity is missed not through malice but through the sheer weight of false positives that compliance staff must process before reaching a genuine one. Monitoring quality is measured by the proportion of alerts that lead to a substantive compliance decision and the average time to that decision — not by alert volume.

A risk-based transaction monitoring framework for an Australian cross-border payment or remittance operator is built in five layers. Each layer addresses a distinct dimension of the monitoring challenge, and the value of the framework comes from how the layers interact — no single layer is adequate on its own.

Figure 4: Five-layer risk-based transaction monitoring framework for AUSTRAC-regulated cross-border payment and remittance operators in Australia

Effective red flag logic in the remittance sector is organised around a principle that compliance practitioners call "explainable risk." A transaction that is large, frequent, or going to a high-risk corridor may be entirely legitimate if the customer's profile, declared purpose, source of funds, and transaction history all tell a coherent, internally consistent story. A smaller transaction can be far higher risk if the surrounding context is incoherent, the customer is evasive, and the pattern across their account deviates sharply from their established baseline.

| Scenario | Characteristics | Risk Level | Required Action |

|---|---|---|---|

| Scenario A Regular family remittances |

Consistent corridor (AU→PH), fortnightly transfers, stable amounts, bank-funded, same verified beneficiary, customer profile consistent with declared employment income | Low — internally coherent, established pattern, no anomaly indicators | Standard ongoing monitoring. No immediate action unless pattern deviation occurs. |

| Scenario B Velocity spike with threshold adjacency |

5 transfers of $1,900 in 3 days to the same beneficiary — first time this pattern has appeared. Cash-funded. Customer gives inconsistent explanations across interactions. | High — structuring indicators, cash usage, profile-behaviour mismatch, evasive responses | Escalate to MLRO immediately. SMR to AUSTRAC likely required. Consider enhanced due diligence or transaction hold. |

| Scenario C Beneficiary concentration pattern |

Five unrelated customers, different profiles, all sending to the same beneficiary account in a FATF-greylisted jurisdiction within one week. None individually exceed TTR threshold. | High — coordinated layering indicators, greylisted corridor, no plausible commercial explanation for beneficiary concentration | Strong SMR candidate for all linked transactions. Internal investigation to establish whether accounts are connected. Consider referral to AUSTRAC relationship manager. |

Figure 5: Three practical remittance transaction scenarios — risk assessment logic under AUSTRAC's risk-based framework

Scenario C illustrates why cross-transaction pattern analysis is the most important and most commonly under-invested layer of remittance monitoring. None of the five individual transactions in Scenario C would trigger a TTR — they all fall below $10,000. None would necessarily trigger a single-transaction risk alert. But the pattern across all five — five different customers, one beneficiary account, one greylisted jurisdiction, one week — is a classic layering signal that is only visible if the monitoring system is connecting transactions across customers, not just analysing them individually. Threshold monitoring sees nothing. Risk-based cross-transaction analysis sees a priority SMR candidate.

Remittance and cross-border payment operators — including experienced, well-intentioned compliance teams — make a predictable set of monitoring mistakes. Identifying and fixing them proactively is substantially less costly than having them identified during an AUSTRAC examination.

Figure 6: Six of the seven most common transaction monitoring failures in Australian remittance operations — and what each one means under AUSTRAC examination

Building and maintaining an AUSTRAC-compliant transaction monitoring programme is one of the most operationally demanding challenges for cross-border payment and remittance businesses in Australia. The monitoring infrastructure must be real-time or near-real-time, risk-stratified by corridor and customer profile, capable of cross-transaction pattern analysis, integrated with sanctions and PEP screening, and backed by audit-grade documentation — all while the business continues to process transactions at volume across multiple corridors simultaneously.

This is precisely the operational environment that RemitSo's Remittance as a Service (RaaS) platform for Australia is designed for. RemitSo provides cross-border payment and remittance operators with the compliance infrastructure — transaction monitoring, AML/CTF programme management, IFTI reporting workflows, sanctions screening, and centralised audit documentation — that AUSTRAC examinations require, built into a platform designed specifically for the operational realities of high-volume cross-border payments. Whether you are launching a new remittance operation under Australia's licensing framework or scaling an existing MSB to handle greater volume and more corridors, the compliance infrastructure is not something that should be bolted on as an afterthought. It is the operational foundation that everything else depends on.

AUSTRAC requires all reporting entities — including remittance operators and cross-border payment service providers — to maintain an AML/CTF programme that includes ongoing transaction monitoring across all designated services and channels. The core monitoring-related reporting obligations are: Threshold Transaction Reports (TTRs) for cash transactions of $10,000 AUD or more, filed within ten business days; Suspicious Matter Reports (SMRs) filed within three business days of forming a suspicion of money laundering, terrorist financing, or proceeds of crime activity — with a 24-hour window for terrorism financing suspicions; and International Funds Transfer Instructions (IFTIs) filed within ten business days for every cross-border electronic transfer in or out of Australia. The TTR obligation is automatic and amount-triggered, but it represents only a fraction of the monitoring obligation. AUSTRAC's broader expectation is a continuously operating, risk-based programme that monitors behaviour, patterns, and anomalies across all transaction types and channels — not just cash above a threshold.

An International Funds Transfer Instruction (IFTI) is a report that must be submitted to AUSTRAC for every electronic transfer of funds into or out of Australia. This obligation applies to every cross-border transaction processed by a remittance operator, regardless of amount — there is no threshold. IFTIs must include the sender's and recipient's details, the originating and destination financial institutions, the transfer amount and currency, and the value date. For a remittance operator processing hundreds of transfers daily, IFTI reporting is a significant compliance infrastructure requirement. Beyond the reporting obligation itself, IFTI data is one of AUSTRAC's primary financial intelligence tools — the regulator mines the dataset to identify emerging ML/TF typologies and to benchmark individual operators' transaction patterns against the sector. When AUSTRAC conducts an examination, it can compare your IFTI submissions against your internal monitoring records and SMR history to identify gaps between what your monitoring should have detected and what was actually reported.

A Suspicious Matter Report must be filed with AUSTRAC when a reporting entity knows, suspects, or has reasonable grounds to suspect that a transaction or activity involves the proceeds of crime, is connected to money laundering, is connected to the financing of terrorism, or relates to a person or entity that may be subject to a sanctions obligation. The trigger is suspicion — not certainty — and the threshold is deliberately low. Common triggers in the remittance sector include structuring patterns where multiple sub-threshold transfers are made in a way that suggests deliberate avoidance of reporting obligations; transactions inconsistent with a customer's declared source of funds or profile; third-party payment arrangements without plausible commercial rationale; transfers to or from FATF-greylisted jurisdictions that are inconsistent with the customer's established pattern; and beneficiary concentration patterns where multiple unrelated customers send to the same destination account. An SMR must be filed within three business days of forming the suspicion — the investigation does not need to be complete before filing.

Structuring — also called "smurfing" — is the practice of deliberately breaking a larger transfer into multiple smaller transactions to avoid triggering the $10,000 AUD Threshold Transaction Report obligation or other internal monitoring thresholds. It is a standalone offence under the AML/CTF Act and one of the most common ML techniques documented in AUSTRAC's typologies for the remittance sector. Detecting structuring requires cross-transaction pattern analysis — not single-transaction monitoring. Detection rules typically include velocity checks that flag multiple transactions from the same customer within a defined time window; amount-pattern analysis that identifies repeated transactions at amounts just below reporting thresholds (e.g. $9,800, $9,900, or $1,900 repeated five times); and linked-party analysis that identifies structuring conducted across multiple accounts associated with the same individual, household, or beneficial owner. Threshold-only monitoring systems cannot detect structuring by design — it is a pattern that is only visible when transactions are analysed in aggregate across time.

Yes — and AUSTRAC's risk-based framework explicitly requires it. A remittance operator that applies the same monitoring intensity to all corridors regardless of the destination jurisdiction's AML/CTF framework strength, FATF designation status, and counterparty risk profile is not operating a risk-based programme. It is applying a flat, undifferentiated control that treats a transfer to a well-regulated EU jurisdiction and a transfer to a FATF-greylisted country as equivalent — which they are not. Corridor risk ratings should be based on FATF mutual evaluation findings and greylisting status, the AML framework maturity of the destination jurisdiction, the counterparty due diligence conducted on the payout partner or agent network in that corridor, and the historical ML/TF typologies documented by AUSTRAC and FATF for that corridor. Higher-risk corridors warrant lower transaction thresholds before monitoring rules trigger, higher monitoring intensity for patterned activity, and enhanced due diligence requirements for customers transacting in those corridors.

Transaction monitoring rules for remittance operators should be reviewed and recalibrated on three timescales simultaneously. Monthly quick checks during high-volume periods — such as Chinese New Year, Diwali, Eid, and major Pacific seasonal events — should identify which rules are generating disproportionate alert volumes and whether the false positive rate has spiked due to seasonal volume increases that the static rules are misclassifying. Quarterly tuning sessions should analyse the false positive rate across all rules, identify patterns in the reasons alerts are being closed without action, and update rules where the business's transaction profile has shifted. Annual full model reviews should be aligned to the enterprise-wide risk assessment update and should incorporate any new AUSTRAC typology guidance, any changes in the corridor and counterparty risk landscape, and any lessons from compliance examination findings — whether from the operator's own AUSTRAC engagement or from published enforcement action against comparable entities.

AUSTRAC requires remittance operators to retain AML/CTF records for a minimum of seven years. The records that must be kept include all customer identification and verification documentation collected during KYC onboarding; records of every designated service provided, including transaction details, amounts, parties, and routing information; all TTRs, SMRs, and IFTIs submitted to AUSTRAC; records of all transaction monitoring alerts generated, including the information considered in reviewing each alert and the rationale for the decision made; records of all customer risk assessments and any enhanced due diligence conducted; and records of AML/CTF programme reviews and updates. Records must be stored securely, in a format that is retrievable promptly on AUSTRAC request, and in a way that preserves evidentiary integrity for the full seven-year period. Electronic records are acceptable; paper is not required. What is required is that the information is complete, accurate, and retrievable — partial or corrupted records are treated as absent records from a compliance perspective.

Non-compliance with AUSTRAC's AML/CTF obligations can attract civil penalties calculated per contravention under the AML/CTF Act. AUSTRAC calculates penalties per breach — meaning systemic non-compliance across thousands of transactions can result in aggregate penalties that reach hundreds of millions of dollars, as demonstrated by enforcement action against major Australian financial institutions. Beyond civil penalties, AUSTRAC can issue enforceable undertakings requiring public commitment to a remediation programme, apply for remedial orders from the Federal Court, and share intelligence with the Australian Federal Police and the Australian Criminal Intelligence Commission where transaction patterns indicate serious financial crime. AUSTRAC's enforcement posture has intensified in recent years and the AML/CTF Amendment Act 2024 has expanded both the regulator's powers and its regulated population. For remittance and cross-border payment operators, the compliance cost of getting monitoring right is a fraction of the regulatory, reputational, and operational cost of getting it wrong.