Foreign exchange risk is the potential financial loss caused by fluctuations in currency exchange rates when a business operates across borders. It affects companies that buy, sell, invoice, or hold assets in foreign currencies — and it is growing in scope and impact as global trade, digital commerce, and cross-border payments expand rapidly. This guide explains what foreign exchange risk is, why it is increasing, how to classify and measure it, and which strategies and tools businesses should use to manage it effectively.

In This Article

Also known as FX risk, forex risk, or foreign currency risk, foreign exchange exposure arises whenever there is a timing gap between agreeing to a transaction and completing it. A business faces this risk when it imports goods priced in foreign currency, exports products internationally, pays overseas suppliers, receives cross-border payments, holds foreign currency balances, or operates foreign subsidiaries. If exchange rates move unfavourably during that gap, the final cost or value of the transaction changes — sometimes significantly enough to eliminate the margin on an otherwise profitable deal.

In practical terms, foreign exchange risk management is the structured process of identifying, measuring, and reducing the financial impact of currency volatility on business operations. According to the International Monetary Fund (IMF), global currency markets are among the most liquid and volatile financial systems, influenced by interest rates, geopolitical developments, inflation data, and central bank policy shifts. For internationally active businesses, FX volatility is an operational reality — not a theoretical concern.

Foreign exchange risk is growing because global trade, digital commerce, and cross-border payments are expanding rapidly. As international transactions increase, exposure to currency fluctuations becomes unavoidable for businesses of all sizes. Three structural factors are amplifying modern forex market risk management challenges in ways that were not present a decade ago.

Figure 1: Three structural factors driving increasing FX risk exposure for internationally active businesses of all sizes

Smaller businesses are more exposed to foreign exchange risk because they operate with tighter margins, limited capital buffers, and fewer treasury resources. Unlike large corporations with structured treasury departments and dedicated FX risk teams, SMEs often manage foreign exchange reactively — responding to rate movements rather than anticipating and managing them. This reactive approach consistently produces worse outcomes than even a basic structured programme.

Figure 2: How unmanaged SME FX exposure compares to outcomes achievable with a structured risk management programme

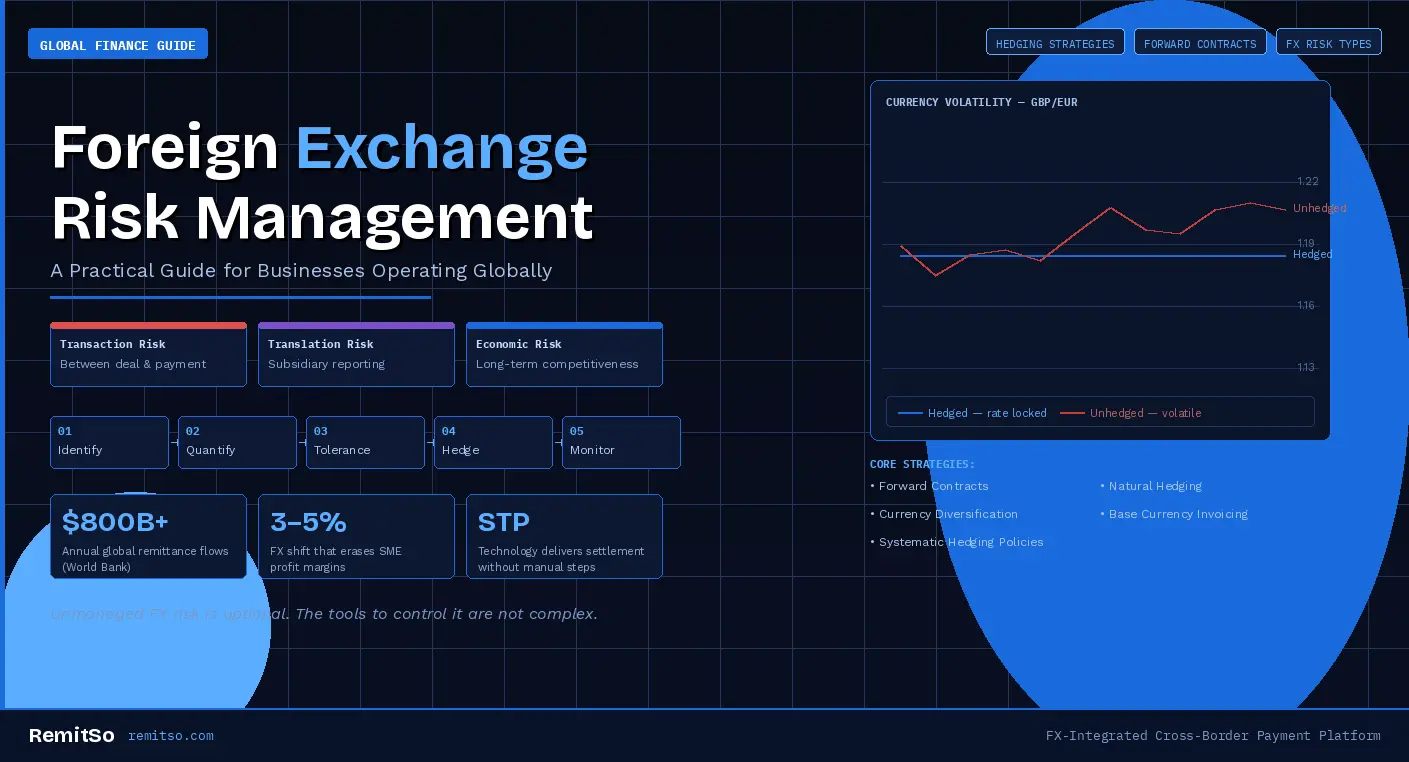

Consider a practical scenario that illustrates how transaction risk materialises. A business agrees to purchase €100,000 worth of goods at a rate of £1 = €1.15, giving an initial expected cost of £86,957. Two months later, when payment is due, the rate has moved to £1 = €1.10. The same payment now costs £90,909 — an unexpected increase of £3,952 with no change in the underlying commercial agreement, no supplier price increase, and no change in the product being purchased.

For a business generating £500,000 annually, this single rate movement represents nearly 1% of annual turnover lost to exchange rate movement rather than commercial underperformance. Across multiple transactions over a financial year, unmanaged FX exposure of this kind can meaningfully distort reported profitability — making what appeared to be a profitable year look marginal once currency losses are aggregated.

Understanding FX exposure begins with accurate classification. The three primary types of foreign exchange risk affect different aspects of financial operations, have different time horizons, and require different management approaches. A business may face all three simultaneously.

| Risk Type | When It Arises | Who It Affects | Primary Impact |

|---|---|---|---|

| Transaction Risk | Between agreeing to and completing a foreign-currency deal | Any business with cross-border transactions | Cash flow — directly affects actual payments received or made |

| Translation Risk | When consolidating foreign subsidiary accounts into home currency | Multinational organisations | Reporting — balance sheet, earnings statements, asset valuations |

| Economic Risk | Sustained long-term currency strength or weakness | Exporters, importers, globally competitive businesses | Strategy — pricing power, export competitiveness, long-term demand patterns |

Figure 3: The three types of foreign exchange risk — when each arises, who it affects, and its primary financial impact

Transaction risk is the most immediate and commonly managed form. Translation risk is primarily a reporting concern for multinationals consolidating subsidiary accounts in different currencies. Economic risk is the most strategic: if a domestic currency strengthens significantly, exports become more expensive for foreign buyers; if it weakens, imports become costlier. These risks can exist simultaneously — a business may face transaction risk on current invoices, translation risk from a foreign subsidiary, and economic risk from a long-term structural currency trend, all at the same time.

Foreign exchange risk management follows a structured five-step process designed to protect profitability and ensure financial stability across international operations. The process is cyclical — it does not end at implementation but requires ongoing monitoring and adjustment as currency markets move and the business's exposure profile changes with growth or new market entry.

Figure 4: The five-step structured process for managing foreign exchange risk in international business operations

A forward contract locks in a fixed exchange rate for a future transaction date. This provides budget certainty, protection from volatility, and a predictable cost structure for planned purchases or sales. Forward contracts are well-suited to large imports, scheduled quarterly payments, and fixed supplier agreements where the currency amount and timing are both known in advance. They are the most widely used hedging instrument for businesses with regular, predictable foreign currency obligations — and the most direct mechanism for eliminating transaction risk on a known future payment.

Natural hedging offsets currency inflows and outflows in the same currency without requiring a financial instrument. A business that both receives USD revenue and pays USD supplier invoices can match these flows, reducing or eliminating the need for currency conversion and lowering net transaction exposure. Natural hedging is highly cost-effective when cash flow timing can be aligned, and it is the first strategy businesses should consider before turning to financial instruments.

Operating across multiple currencies reduces concentration risk in any single currency pair. Diversification spreads exposure across several exchange rates so that adverse movement in one currency is not catastrophic to the overall position. For businesses with global customer bases or multi-jurisdiction operations, this structural diversification provides inherent FX resilience.

Where bargaining power allows, businesses can invoice international customers in their domestic currency. This transfers FX risk to the counterparty — though it may reduce competitiveness if customers prefer to transact in their own currency. The appropriate balance between currency convenience for the customer and FX risk retention by the business depends on market positioning and the competitive dynamics of each relationship.

Structured foreign exchange management policies provide the discipline that prevents reactive, ad hoc decision-making. A well-designed policy defines specific coverage thresholds — for example, hedge 100% of transactions above £20,000, hedge 75% of forecasted foreign revenue, and review coverage on a quarterly basis. Policy discipline removes the temptation to speculate on rate movements and ensures hedging decisions are made consistently, regardless of market conditions at any given moment.

Hedging is not universally appropriate. The decision to hedge must consider whether the cost of the hedge is proportionate to the risk being mitigated. Hedging is generally inappropriate when transactions are small and irregular, when the cost of the hedging instrument outweighs the potential FX loss, when currency inflows and outflows naturally offset each other and natural hedging is sufficient, or when cash flow timing is too uncertain to define reliable hedge parameters.

Over-hedging introduces complexity and additional expense without proportionate risk reduction. Effective foreign exchange risk management balances the cost of protection against the magnitude of exposure — and that balance point is different for every business, every transaction type, and every market environment. The goal is not to hedge everything — it is to hedge the right exposures to the right degree.

Technology is transforming how businesses manage foreign exchange and risk management processes. Modern digital platforms provide real-time FX rate tracking, multi-currency account management, automated settlement workflows, exposure dashboards, straight-through processing, and integrated compliance and reporting tools. Automation reduces manual errors, increases operational visibility, and makes structured FX management accessible to businesses that lack dedicated treasury teams.

The National Institute of Standards and Technology (NIST) emphasises that secure digital financial infrastructure must incorporate cybersecurity controls, data protection, and operational risk monitoring — disciplines that are increasingly integrated into modern FX management platforms. As cross-border commerce scales, digital infrastructure becomes essential to effective multi-currency account management and settlement workflow control.

Figure 5: Three operational capabilities that technology delivers for FX management that manual processes cannot replicate at scale

A resilient FX framework requires more than selecting individual hedging instruments. It requires a coherent plan that integrates exposure mapping, forecasting, hedging strategy, monitoring, and accounting alignment into a single operational programme. The following elements form the minimum viable framework for any business with material foreign currency exposure.

Begin by auditing exposure — mapping all currency cash flows expected over the next 12 months, by currency, counterparty, and timing. Then forecast currency requirements by aligning the cash flow map with procurement and sales projections. Define a hedging strategy by establishing clear coverage thresholds and the instruments that will be used to achieve them. Implement monitoring systems that track exposure weekly or monthly with the discipline to act when thresholds are breached. Finally, align with accounting standards — ensuring hedging policies integrate with the business's financial reporting requirements so that hedge instruments are correctly classified, documented, and disclosed in financial statements.

As international operations grow, businesses require infrastructure that integrates foreign exchange management, cross-border payment orchestration, compliance workflows, multi-currency account management, and real-time operational visibility into a single operational layer. Fragmented systems — separate FX providers, payment platforms, and compliance tools — introduce exactly the reconciliation gaps and exposure blind spots that structured FX management is designed to eliminate.

RemitSo's platform is designed to support businesses managing international payments and currency exposure within a structured, secure ecosystem. Rather than functioning as a standalone transfer tool, it integrates FX workflows, compliance monitoring, and payment automation into a single operational layer — helping organisations centralise oversight, improve settlement efficiency, and reduce the exposure gaps that arise when currency management and payment infrastructure operate in isolation from each other.

Foreign exchange risk management is the structured process of identifying, measuring, and mitigating financial losses caused by currency fluctuations in international business transactions. It involves mapping all foreign currency exposures, quantifying their potential impact on margins, defining an acceptable risk tolerance, selecting appropriate hedging or operational tools, and monitoring positions continuously as currency markets move. Effective FX risk management transforms currency volatility from an unpredictable threat into a manageable and measurable operational variable — one that can be budgeted for and controlled like any other business cost.

SMEs often operate with profit margins of 10–15%, which means a 3–5% adverse currency movement can eliminate an entire year's margin on an international contract. Unlike large corporations with structured treasury teams, SMEs typically manage FX reactively without formal policies — which consistently produces worse outcomes than even a basic structured programme. The combination of thin margins, limited capital buffers, and no dedicated FX expertise makes smaller businesses disproportionately vulnerable to exchange rate volatility compared to larger competitors who can absorb or hedge the same movements more effectively.

The three primary types of foreign exchange risk are transaction risk, translation risk, and economic risk. Transaction risk is the most common — it arises between agreeing to and completing a foreign-currency deal and directly affects cash flow. It can be managed with forward contracts or natural hedging. Translation risk arises when consolidating foreign subsidiary financials into the home currency and primarily affects multinational balance sheet and earnings reporting. Economic risk is long-term and strategic — sustained currency movements that affect export competitiveness, pricing power, and global demand patterns over time.

Forex market risk management protects profits by stabilising cash flow through locking in exchange rates on future transactions, offsetting exposures so that currency gains and losses cancel rather than compound, and reducing the uncertainty in cross-border transactions that makes budgeting unreliable. By eliminating the gap between the expected cost of an international transaction at the point of commercial agreement and its actual settlement cost weeks or months later, structured FX management ensures that the profitability assessed when a deal is agreed is not eroded by rate movements before the transaction closes.

Businesses should implement structured FX policies when they engage in recurring, predictable foreign currency transactions that materially impact profitability — meaning the potential currency loss on unmanaged exposures is large enough relative to operating margins to warrant a hedging cost. In practice, any business regularly importing or exporting in foreign currency should have at minimum a written FX policy that defines coverage thresholds, review frequency, and approved instruments. Waiting until an adverse currency move has already caused a loss is consistently the most expensive approach to FX risk management.

Multi-currency account management reduces FX exposure by allowing businesses to hold, receive, and pay in the same currency without unnecessary conversion. When a business receives USD from customers and can pay USD to suppliers from the same account, the conversion — and the FX risk it creates — is eliminated entirely for that matched pair. This is the operational mechanism of natural hedging at scale: matching receivables and payables in the same currency so that the net exposure requiring conversion and hedging is minimised. Digital platforms providing multi-currency accounts make this approach accessible to businesses of all sizes.

No — any business that imports, exports, or processes cross-border payments faces foreign exchange risk and benefits from structured management practices. The World Bank reports that global remittance flows exceed $800 billion annually, with trillions more in cross-border trade. Digital commerce has lowered the barrier to international selling so significantly that businesses often accumulate material FX exposure before implementing any formal management framework. The scale of the business determines the complexity of the programme required — not whether one is needed at all. Even a modest import-export operation with annual foreign currency transactions above £50,000 warrants a written FX policy.

Digital platforms automate rate tracking, settlement processing, compliance monitoring, and exposure reporting — improving accuracy and operational control while reducing the manual effort that creates errors and delays in traditional FX management. Modern FX infrastructure provides real-time visibility into currency positions, straight-through settlement that eliminates manual steps and the FX slippage they create, and integrated compliance workflows that satisfy AML, reporting, and audit requirements in parallel with the payment process. Technology makes structured FX management accessible to businesses without in-house treasury teams by replacing the need for specialist expertise with configurable system logic and automated rules.