Behind every remittance app and international payment platform lies one of the most operationally demanding businesses in fintech. This guide covers every major challenge — compliance, banking, FX, fraud, infrastructure, and more — and how modern operators navigate them.

The global cross-border payments industry is growing rapidly. Businesses and consumers now expect instant international money transfers, low fees, real-time tracking, and seamless digital experiences. But behind every successful remittance app or international payment platform lies a highly complex operational ecosystem — one that demands simultaneous mastery of regulatory compliance, foreign exchange, fraud prevention, banking relationships, payment infrastructure, and customer experience, all at once.

In This Guide

A cross-border payments business enables individuals or companies to send and receive money internationally. The category includes remittance companies and Money Transfer Operators (MTOs), fintech payment apps, Electronic Money Institutions (EMIs), Payment Institutions (PIs), digital wallets, B2B payment providers, and payout API companies. Their services span international money transfers, currency exchange, global payouts, merchant settlements, wallet services, and real-time payment processing.

Although the customer experience may appear simple — enter an amount, choose a destination, press send — the operational structure behind these services is extremely sophisticated. A single payment may touch several institutions, cross multiple regulatory jurisdictions, and require real-time compliance checks before reaching the final recipient. Every stage introduces its own set of challenges.

Unlike domestic payments, international transactions involve multiple currencies, different banking systems operating on different schedules, cross-border regulatory frameworks that do not align with each other, AML screening and sanctions checking at multiple points in the payment chain, correspondent banking networks, and local payout infrastructure that varies significantly by country. Companies entering this space often underestimate how many independent systems must work in coordination for a single payment to complete successfully.

| Payment Stage | Complexity Layer | Risk Type |

|---|---|---|

| Customer onboarding | KYC verification, identity checks | Compliance |

| Payment initiation | FX rate lock, fee calculation | FX / Commercial |

| AML screening | Transaction monitoring, sanctions check | Regulatory |

| Routing | Banking partner selection, corridor coverage | Operational |

| Currency conversion | FX liquidity, spread management | Financial |

| Settlement | Correspondent network, nostro funding | Liquidity |

| Last-mile delivery | Local rails, payout partner, beneficiary | Operational |

| Reconciliation | Multi-party ledger matching | Operational |

Figure 1: Each stage of an international payment introduces its own complexity layer and risk type — and all must work in coordination.

Compliance is the single biggest operational challenge for most cross-border payment companies. International payments are heavily regulated because they can be exploited for money laundering, terrorist financing, fraud, sanctions evasion, and cybercrime. Every licensed payment operator must maintain a functional AML program, a KYC onboarding process, transaction monitoring, sanctions screening, Travel Rule compliance for relevant transfers, and a framework for filing Suspicious Transaction Reports or Suspicious Activity Reports to the relevant regulator.

The deepest complexity is jurisdictional fragmentation. A remittance company operating globally may require licenses in dozens of countries, with each jurisdiction maintaining its own AML rules, reporting obligations, transaction thresholds, customer verification standards, and data privacy laws. The UK's FCA, the EU's competent authorities, FinCEN and state regulators in the USA, MAS in Singapore, AUSTRAC in Australia, and the UAE Central Bank all apply materially different standards. Managing these overlapping compliance obligations becomes an ongoing operational function in its own right. For a detailed breakdown of what's required, see our guide on compliance and risk management for money transfer businesses.

| Requirement | Purpose | Regulator Impact |

|---|---|---|

| KYC (Know Your Customer) | Verify customer identity before onboarding | All jurisdictions |

| AML Monitoring | Detect and report suspicious activity | All jurisdictions |

| Sanctions Screening | Block transactions involving prohibited parties | All jurisdictions |

| Transaction Monitoring | Identify high-risk or unusual behavior | All jurisdictions |

| Travel Rule Compliance | Share sender/receiver data above threshold | FATF members |

| STR / SAR Reporting | File reports on suspicious transactions | All jurisdictions |

Figure 2: Every licensed cross-border payment operator must maintain these compliance obligations — standards and thresholds vary by jurisdiction.

Many payment companies struggle to maintain stable banking partnerships. This issue — commonly called "de-risking" — occurs when banks terminate or decline business relationships with remittance companies and money services businesses due to AML concerns, compliance cost exposure, or regulatory pressure. Without banking partners, payment companies cannot hold client funds, access correspondent networks, or process transactions efficiently.

The problem compounds the fact that traditional correspondent banking networks are shrinking globally. Banks are exiting low-volume, high-complexity corridors — particularly in emerging markets and frontier economies where the compliance cost per transaction is high relative to revenue. This creates coverage gaps, increases costs where coverage remains, and slows settlement in affected corridors. Payment companies targeting these markets must invest heavily in alternative banking relationships and direct payout partner networks to compensate. Our guide on opening a business bank account for money services businesses covers what operators in the USA face specifically.

Cross-border payment companies constantly manage multiple currencies, creating continuous FX exposure. The core risk is straightforward: when a company quotes a transfer rate to a customer before settlement completes, any adverse market movement during the settlement window compresses margins or generates losses. At high transaction volumes, even small FX moves can have significant financial impact. For a detailed look at how to manage this, see our guide on foreign exchange risk management.

Liquidity management is the operational companion to FX risk. Payment companies must maintain pre-funded balances across multiple countries, currencies, banking partners, and settlement systems simultaneously. Under-funding a corridor means delayed payouts or failed settlements; over-funding ties up capital in low-yield positions. Getting this balance right at scale — across dozens of active corridors — requires treasury infrastructure, hedging tools, and real-time visibility into settlement positions that many startups in this space underestimate when building their initial operations.

Fraud remains one of the most persistent operational threats in international money movement. Cross-border payments are particularly attractive to criminals because of the international complexity, multi-jurisdiction oversight gaps, high transaction volumes, and increasingly fast digital onboarding processes that reduce the friction available for manual fraud review. For a comprehensive breakdown of the fraud landscape, see our guide on preventing cross-border payment fraud.

| Fraud Type | How It Works | Detection Difficulty |

|---|---|---|

| Identity theft | Stolen or fabricated identities used to open accounts | Medium |

| Account takeover | Unauthorized access to existing customer accounts | Medium |

| Mule accounts | Real accounts used to layer and move illicit funds | High |

| Synthetic identities | Fake identities built from combinations of real data | High |

| Transaction laundering | Disguised illegal payments routed through legitimate operators | High |

| Social engineering | Customers manipulated into authorising fraudulent transfers | Medium |

Figure 3: Fraud types by detection difficulty — mule accounts, synthetic identities, and transaction laundering are the hardest to catch with traditional rule-based systems.

Real-time payment systems create a particular challenge: once a payment settles in seconds, recovery of fraudulent funds becomes extremely difficult. Effective fraud prevention in this environment requires machine learning models, behavioural analytics, velocity checks, device intelligence, and real-time transaction monitoring — all running in parallel before settlement completes.

Running a global payment platform requires deep, reliable technical infrastructure across payment APIs, KYC systems, AML engines, FX conversion systems, payout integrations, fraud prevention tools, and regulatory reporting. Maintaining this infrastructure globally is both expensive and technically demanding — and the cost compounds with every new corridor, currency, or regulatory jurisdiction added.

A further complication is that many international payment systems still rely on legacy SWIFT messaging, batch settlement systems, manual reconciliation processes, and outdated banking technology at the correspondent level. Even if a fintech operator's own infrastructure is modern and API-native, they inevitably interface with partners running legacy systems — introducing delays and operational inefficiencies that the fintech itself cannot fully control. This is one of the key reasons why choosing the right payout partner network matters so much. For more on building this infrastructure correctly, see our guide to payout partner APIs for remittance and cross-border payments.

The "last mile" — the final stage where money reaches the recipient — remains one of the biggest global payment bottlenecks. Even when international payment rails are fast, local payout systems in destination markets may still impose significant delays. Local banking limitations, manual review requirements, regulatory checks, operating hour restrictions, FX controls, and beneficiary verification delays all affect how quickly funds clear into the recipient's account or mobile wallet.

The problem is most acute in the markets that matter most for remittances. Many high-volume destination corridors — rural Bangladesh, western Kenya, parts of West Africa and Southeast Asia — have local payment infrastructure that lags behind international rails by years. Payment companies must invest in multi-channel payout infrastructure — bank accounts, mobile wallets, cash pickup networks, and card payouts — to maximise coverage and minimise last-mile delivery time across all recipient profiles.

Compliance is not just operationally complex — it is expensive. Cross-border payment businesses spend heavily on AML software, KYC vendor integrations, dedicated compliance officers and MLRO appointments, external audits, regulatory filings, transaction monitoring infrastructure, and legal support across multiple jurisdictions. For startups in the early years of operation, compliance costs can consume a disproportionate share of revenue before transaction volumes reach the scale needed to distribute costs efficiently.

Licensing itself carries significant capital requirements. Most regulatory frameworks require minimum capital reserves, sometimes require physical office presence in the licensed jurisdiction, and impose security deposit or surety bond obligations. Annual compliance audits and regulatory reporting add ongoing overhead. Expansion into each new country typically requires repeating this process from scratch — meaning that a payment company operating across 10 jurisdictions is effectively managing 10 parallel compliance programmes simultaneously.

RemitSo's white-label platform includes built-in AML monitoring, automated KYC, and sanctions screening — so you launch with compliance infrastructure, not spreadsheets.

Customer expectations for international money transfers have been fundamentally reset by the fintech generation. Customers now expect instant or near-instant transfers, low or zero visible fees, complete transparency on exchange rates and total cost, mobile-first interfaces, and real-time tracking from initiation to delivery. The bar is set not by what traditional banks deliver, but by what the best fintech apps deliver — and catching up from a standing start is difficult.

The tension between customer experience and compliance is real. Customers want payments to complete immediately. Regulators require AML reviews, sanctions screening, fraud checks, and transaction monitoring — all of which consume time. The most operationally mature payment companies resolve this tension through automation: machine learning that completes compliance checks in milliseconds rather than minutes, automated KYC that onboards customers in under 15 seconds, and rules engines that escalate only the small percentage of transactions that genuinely require human review.

The cross-border payments industry is intensely competitive. Companies compete on exchange rates, transfer speed, user experience, payout corridor coverage, and pricing transparency simultaneously. Margins on high-volume consumer corridors have compressed significantly as more operators enter established routes, forcing continued investment in operational efficiency and product differentiation to maintain profitability. For more on managing FX margins competitively, see our guide to FX spread strategy for money transfer businesses.

The competitive pressure is compounded by technology democratisation. Open Banking frameworks, Banking-as-a-Service platforms, payout APIs, and embedded finance infrastructure have lowered the barriers to entering the payments space. This means the competitive set for any given corridor or customer segment is continuously expanding — including from adjacent categories like neo-banks, super apps, and large technology platforms adding payments to their existing services.

Cross-border payment companies handle highly sensitive data — identity documents, bank account details, transaction histories, and personal financial information at scale. This makes them persistent targets for data breaches, ransomware attacks, phishing campaigns, insider threats, and API abuse. A single significant breach can cause regulatory sanction, reputational damage, and customer attrition that takes years to recover from.

Data privacy compliance adds another layer of complexity. Businesses operating globally must comply with GDPR in Europe, PDPA in Singapore, CCPA in California, and an increasing number of data localisation laws in various countries — some of which require that customer data be stored and processed within the jurisdiction where it was collected. For a cross-border payment company with customers in twenty countries, managing this patchwork of data privacy obligations is a sustained operational function.

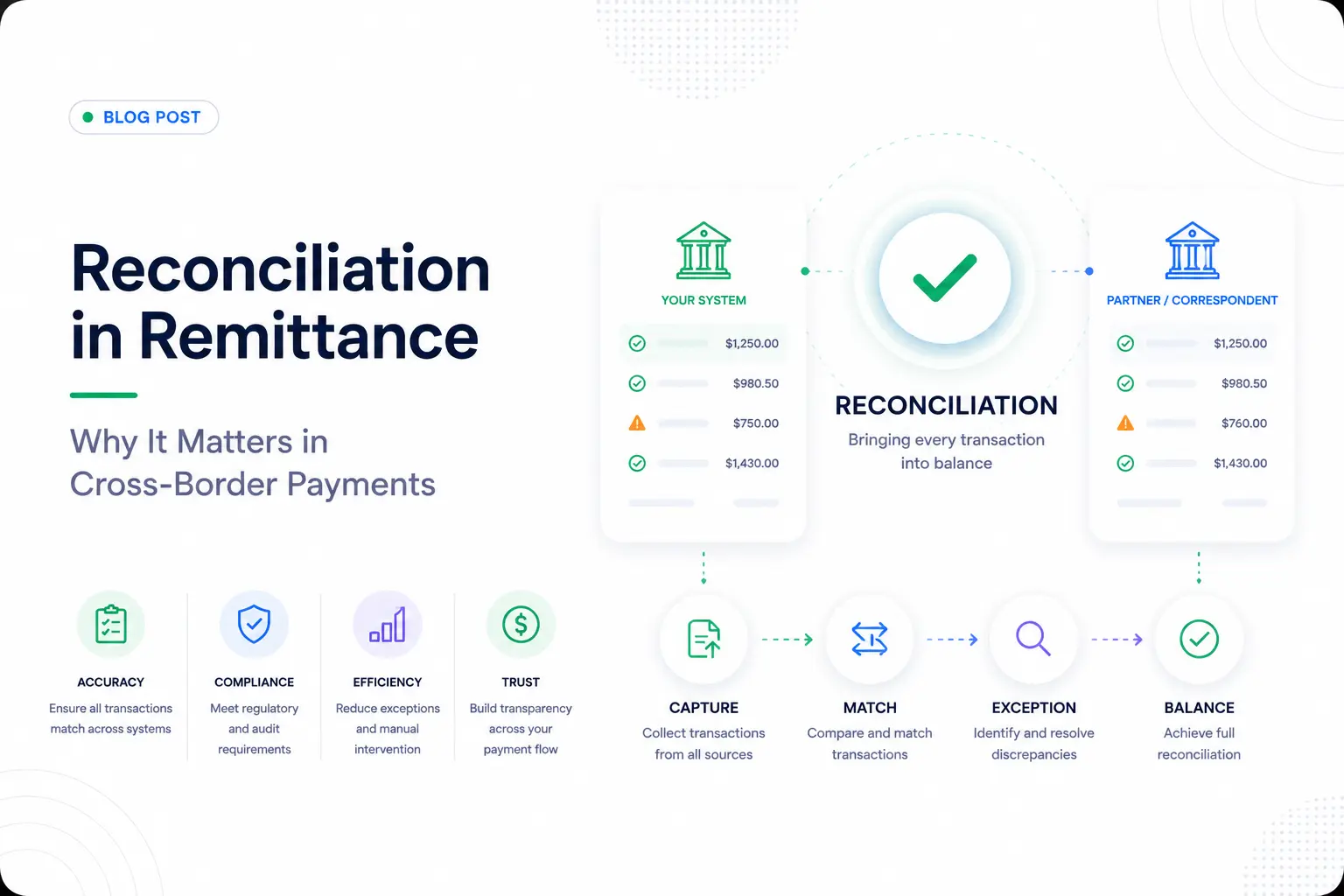

International payments involve multiple intermediaries — originating banks, correspondent banks, local partners, and beneficiary institutions — and reconciling positions across all of these parties is operationally intensive. Delayed settlements, mismatched records, failed transactions, and reconciliation errors create direct financial exposure and customer service burden. Manual reconciliation processes increase operational risk and staffing costs; automating them requires significant investment in reporting and data infrastructure. For more on how this works in practice, see our guide on remittance reconciliation.

As payment companies grow, operational complexity increases exponentially rather than linearly. Scaling to new corridors requires new licenses, new banking relationships, new payout partner integrations, and new compliance programmes. Scaling transaction volumes requires stronger fraud systems, more liquidity across more positions, and expanded compliance teams capable of reviewing the increased volume of flagged transactions. Growth without the infrastructure to support it has caused operational failures at several high-profile payment companies — and the failure modes tend to be compliance-related, which means regulatory consequences in addition to operational ones.

The most operationally mature cross-border payment companies have addressed these challenges through a combination of technology investment and infrastructure decisions that compound over time. API automation reduces manual operations and enables real-time integration with payout partners, compliance tools, and banking infrastructure. Open Banking connectivity improves funding speed and cost. AI-powered AML monitoring — running machine learning models trained on global transaction patterns — improves fraud detection accuracy while reducing the false positive rate that creates friction for legitimate customers. Cloud infrastructure provides the scalability to absorb volume spikes without service degradation.

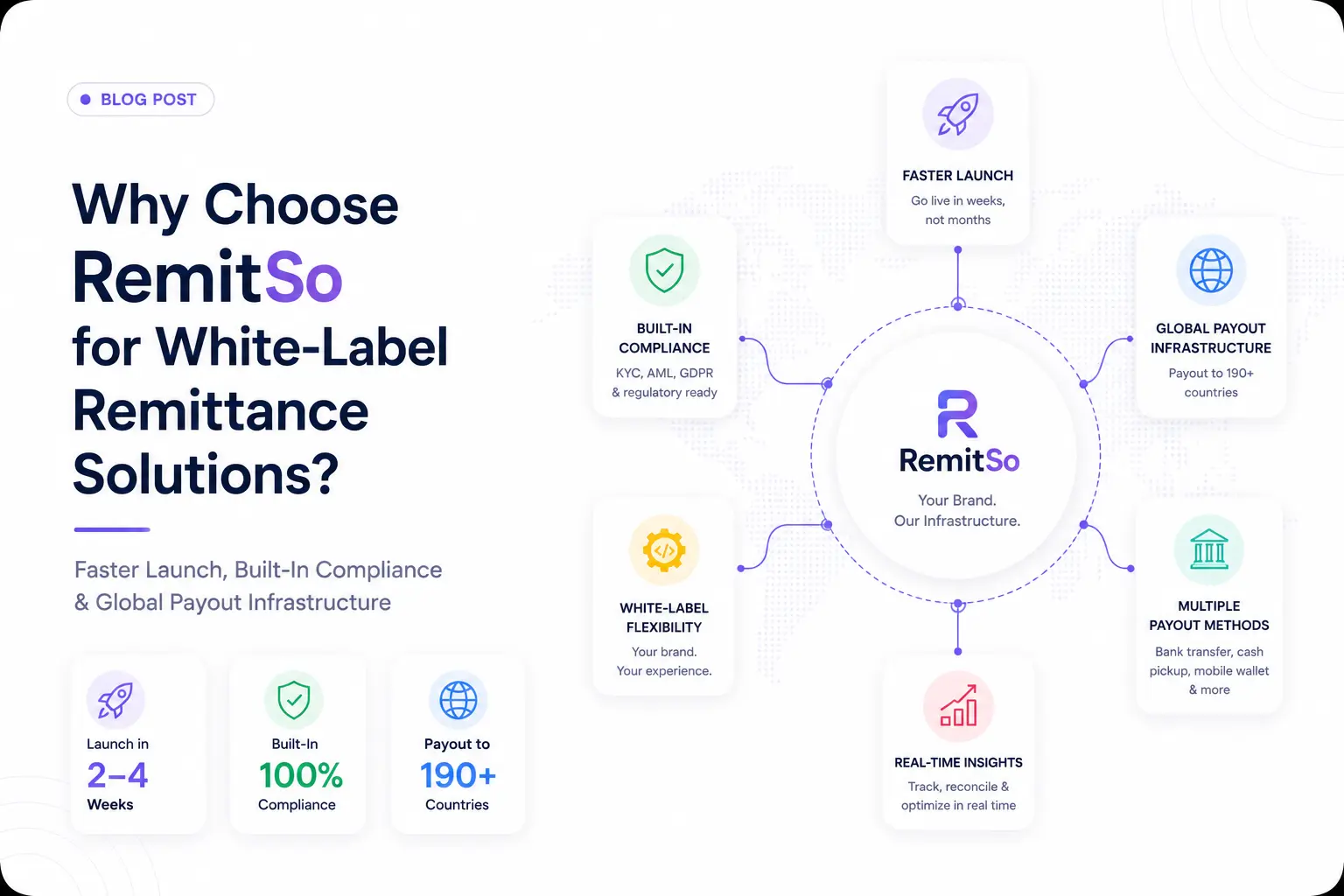

Many newer operators have accelerated this journey by launching on white-label platforms that provide pre-built compliance infrastructure, payout partner networks, and technical architecture from day one — rather than attempting to build every component independently. This approach compresses time to market from years to weeks and allows founders to focus on customer acquisition and corridor strategy rather than infrastructure build-out.

The industry is not standing still, and the challenge landscape continues to evolve. Real-time fraud prevention in instant payment environments will remain a technical arms race. Stablecoin and digital asset regulation is taking shape across major markets, creating new compliance questions for operators who want to offer crypto-enabled corridors. AI-driven cybercrime — including deepfake-based identity fraud and large language model-powered social engineering — is introducing fraud vectors that traditional detection systems were not designed to catch.

Travel Rule implementation is extending to more jurisdictions and lower thresholds, requiring payment operators to build data-sharing infrastructure between institutions. Global sanctions complexity is increasing as geopolitical fragmentation creates more overlapping and sometimes conflicting sanctions regimes that operators must screen against simultaneously. And data sovereignty requirements are tightening in multiple major markets, adding ongoing overhead to the already complex challenge of managing cross-border data flows in a regulated environment.

Despite the operational complexity, the industry continues growing because the structural demand drivers are strong and persistent. Rising global migration, the growth of cross-border e-commerce, SME international trade, the expansion of freelancer and gig economies, and rapid digital banking adoption across emerging markets all sustain demand for fast, affordable international payments. The operators who succeed are those who treat the operational complexity as a structural moat rather than a barrier — because every layer of compliance, technology, and banking infrastructure that is hard to build is equally hard for a competitor to replicate.

RemitSo gives you the platform, compliance infrastructure, and payout network to enter this market professionally — without building everything from scratch.

Cross-border payment companies must simultaneously manage regulatory compliance across multiple jurisdictions, AML and KYC obligations, fraud prevention, foreign exchange risk, liquidity across multiple currencies, banking partner relationships, cybersecurity, and customer experience — all in real time. Unlike domestic payment businesses, every international transaction introduces regulatory obligations in at least two jurisdictions, currency conversion risk, and a multi-party settlement chain that no single operator controls end to end. The complexity compounds with every new corridor, currency, or market added. Companies that scale successfully in this industry treat compliance, technology, and risk management as core infrastructure investment rather than overhead costs.

Regulatory compliance and AML obligation management remain the biggest operational challenges for most cross-border payment providers. The complexity of maintaining compliant operations across multiple jurisdictions — each with different AML rules, reporting thresholds, data privacy laws, and licensing requirements — creates a sustained operational burden that grows with every new market entered. Compliance failures carry the most severe consequences: regulatory sanctions, license suspension, and reputational damage that can permanently impair the business. As a result, compliance infrastructure tends to be the area where experienced operators invest most heavily, and where underprepared entrants most commonly fail.

Banks may terminate or decline relationships with remittance companies because of the perceived AML exposure associated with money services businesses, the compliance cost of monitoring high-volume, cross-border transaction flows, and the regulatory pressure that follows enforcement actions against banks found to have inadequate oversight of their MSB customers. From a bank's perspective, the revenue generated by a remittance company's account may not justify the compliance overhead and regulatory risk. De-risking is a structural industry problem — not specific to any individual operator — and has been documented extensively by the World Bank, FATF, and the Financial Stability Board. Addressing it requires remittance companies to demonstrate robust AML programmes and provide strong compliance documentation to prospective banking partners.

The last mile refers to the final stage of a cross-border payment — the step where funds are delivered to the recipient in their local market. Even when international payment rails are fast, local payout infrastructure in destination markets may impose significant delays due to local banking limitations, manual review requirements, regulatory checks, operating hour restrictions, FX controls, and beneficiary verification processes. The problem is most acute in high-volume remittance destination markets in South Asia, sub-Saharan Africa, and Southeast Asia, where local payment infrastructure lags international standards. Payment companies address this by building multi-channel payout capabilities — bank account transfers, mobile wallet payouts, cash pickup networks, and card payouts — so that each recipient can be reached through whichever channel delivers most efficiently in their location.

Compliance costs are high because payment operators must invest simultaneously in multiple distinct cost centres: AML monitoring software, KYC vendor integrations and identity verification services, dedicated compliance officers and an appointed MLRO in each licensed jurisdiction, external compliance audits, regulatory filing preparation, transaction monitoring infrastructure capable of processing high transaction volumes in real time, and legal support across multiple regulatory environments. Each new licensed jurisdiction adds another instance of this cost structure. For early-stage businesses before transaction volumes reach scale, compliance overhead can represent a significant share of total operating cost — which is one reason why white-label platforms with built-in compliance infrastructure have become an attractive alternative to building from scratch.

Fintechs improve cross-border payment operations through several converging technology approaches. API automation reduces manual operations and enables real-time integration with payout partners, banking infrastructure, and compliance tools. Open Banking frameworks provide direct, programmable access to bank account funding and payment initiation. AI-powered AML monitoring processes transactions at speed with machine learning models that identify suspicious patterns more accurately than static rule sets. Cloud infrastructure scales cost-efficiently with transaction volume rather than requiring large fixed investment. Real-time domestic payment rail integrations in destination markets — UPI, PIX, Faster Payments, InstaPay — reduce last-mile delivery times. Automated digital KYC onboards customers in seconds. Together these capabilities allow fintechs to operate more efficiently than legacy correspondent banking chains while maintaining the compliance standards regulators require.

Cross-border payment companies face several major fraud risk categories. Identity theft and synthetic identities — where criminals use stolen or fabricated identity data to open accounts — are persistent onboarding risks. Account takeover, where attackers gain unauthorised access to legitimate customer accounts through credential theft or phishing, is a major operational threat. Mule accounts, where real customers knowingly or unknowingly allow their accounts to be used to layer illicit funds, are particularly hard to detect because the account holder is genuine. Transaction laundering involves processing payments for undisclosed illegal activity through the platform. Social engineering fraud manipulates legitimate customers into authorising payments to fraudulent beneficiaries. Real-time payment systems amplify all of these risks because the window available for detection before settlement is measured in seconds rather than hours.

The future of cross-border payments is being shaped by several converging developments. Real-time payment rail interlinkage — connecting domestic instant payment systems across borders — is expanding the corridors where near-instantaneous cross-border settlement is possible for all operators. ISO 20022 adoption is standardising payment messaging with richer data, reducing manual exception handling. AI-driven compliance is improving AML accuracy and reducing false positive rates that create friction for legitimate customers. Embedded finance is integrating cross-border payment capabilities into platforms customers already use daily. Stablecoin and digital asset settlement is moving from experiment to regulated practice in several major markets. Travel Rule implementation is creating interoperable compliance data standards across jurisdictions. The net direction is toward a global payment ecosystem that is faster, cheaper, more inclusive, and more transparent — though the compliance and infrastructure investment required to participate in that ecosystem continues to grow.