Australia sent A$56.6 billion overseas in 2024. That number — equivalent to roughly 2.7% of GDP flowing out of the country in personal and family transfers — is not a fringe financial statistic. It is one of the defining features of a country where 31.5% of the population was born overseas, where the top five source countries for new migrants are also the top five destinations for outbound money, and where the gap between what banks charge for international transfers and what the best digital operators charge has never been wider. For anyone building a remittance business, investing in one, or trying to understand who the competition is and why — this is the market guide.

In This Article

Australia's remittance market is large, growing quickly, and structurally underserved in a way that creates durable opportunity for operators who can combine competitive pricing with strong compliance and a genuinely digital customer experience. The headline figure — A$56.6 billion in outbound remittances in 2024 — positions Australia among the world's largest per-capita remittance-sending countries. What makes that figure commercially interesting is not just the size but the trajectory: the formal outbound remittance market reached US$10.11 billion in 2024 (a 28.5% increase over 2023) and is forecast to grow at a 16.2% CAGR to reach US$18.46 billion by 2028, driven by sustained high immigration levels and the structural shift from cash and bank-channel remittances toward digital platforms.

| Metric | Figure | Source / Note |

|---|---|---|

| Total outbound remittances (2024) | A$56.6 billion (US$38.2 billion) | TechCabal / LemFi Australia market entry data, Feb 2026 |

| Formal outbound remittance market (2024) | US$10.11 billion — up 28.5% on 2023 | ResearchAndMarkets Australia International Remittance Market Report (formal/licensed channels) |

| Formal outbound CAGR (2024–2028) | 16.2% — reaching US$18.46 billion by 2028 | ResearchAndMarkets. Note: distinct from total A$56.6B figure which includes all channels including informal |

| Digital remittance market (2024) | US$386.6 million (online platform segment only) | Grand View Research / Horizon Databook — narrower definition covering app/web platforms only |

| Digital remittance market (2030 forecast) | US$991.8 million | 17.6% CAGR 2025–2030 — Grand View Research |

| Outward digital remittance share | 65.42% of digital segment (2024) | Grand View Research outward vs inward digital split |

| Inbound remittance market (2024) | US$1.73 billion — up 16.9% on 2023 | ResearchAndMarkets — forecast US$2.60 billion by 2028 at 10.6% CAGR |

| Migrant share of population | 31.5% (approximately 8.6 million people) | LemFi / ABS; following record net overseas migration 2022–2024 |

| Migrants' contribution to economy | A$480.5 billion annually | Migration contributes roughly 22% of GDP — the same population drives the remittance market |

Figure 1: Core Australia remittance market statistics — 2024 actual figures and 2026–2030 forecast trajectory

Three distinct market figures circulate in research on Australia's remittance market, and understanding what each measures is essential for interpreting them correctly. The total outbound figure (A$56.6 billion / US$38.2 billion) is the broadest measure — it includes every channel through which money leaves Australia: bank wire transfers, licensed digital platforms, agent networks, and informal channels. The formal outbound market (US$10.11 billion in 2024, per ResearchAndMarkets) covers only licensed, regulated channels — the addressable market for compliant operators. The digital platform segment (US$386.6 million, Grand View Research) is narrower still, covering only app and web-based transfer services. The gap between these figures is the conversion opportunity: the vast majority of Australia's outbound remittance volume still flows through channels where digital operators are not yet the primary provider. Each percentage point of channel shift toward digital represents tens of millions of dollars in transaction revenue moving toward operators with modern infrastructure.

Australia's remittance market is structurally different from most other high-income remittance-sending countries in one critical way: the immigration rate is extraordinarily high relative to the population. Australia's net overseas migration reached record levels in 2022 and 2023, and the 31.5% overseas-born population share places it among the most demographically diverse major economies in the world. This is not a temporary spike — it is the result of decades of immigration policy that has built a population with deep transnational financial ties that express themselves as remittance flows.

Figure 2: Four demographic factors that structurally sustain Australia's position as one of the world's highest per-capita remittance-sending markets

Corridor selection defines a remittance operator's competitive position more than any other single factor. The Australian market has a small number of extremely high-volume corridors — India and China together account for more than a quarter of all outbound remittances — and a longer tail of mid-volume corridors where competition is thinner and fees remain elevated. Understanding the specific competitive dynamics in each corridor is essential for operators deciding where to focus and how to price.

| Corridor | 2024 Volume | Share of Total | Primary Payout Methods | Competition | Operator Insight |

|---|---|---|---|---|---|

| Australia → India | US$7.3 billion | ~19% of total outbound | IMPS, UPI, NEFT, bank transfer | Very High — Wise, Remitly, InstaRem, OFX, CBA, NAB, all major players active | UPI delivery speed is the differentiator; operators who settle to UPI in under 2 hours have a measurable conversion advantage. Margin is thin — this is a volume corridor. |

| Australia → China | US$5.35 billion | ~14% of total outbound | Bank transfer (Union Pay), WeChat Pay, Alipay | High — but compliance complexity reduces field; UnionPay connectivity is a genuine barrier | Compliance-capable operators have structural advantage; WeChat Pay integration is a meaningful UX differentiator for younger Chinese-Australian senders. |

| Australia → Philippines | Major corridor — exact volume not independently verified at publication | Among top 5 outbound corridors | GCash, Palawan Express, bank, cash pickup | Medium-High — GCash integration is almost mandatory; operators without it lose a significant share of Filipino-Australian senders | Cash pickup remains important for recipients in provinces. GCash-capable operators with competitive rates and a Filipino-language UX have strong community loyalty advantages. |

| Australia → Vietnam | Significant — Vietnamese-Australian is one of the largest and oldest diaspora communities | Among top 5 outbound corridors | Bank transfer (Vietcombank, Techcombank), MoMo | Medium — strong Wise/Remitly presence but community-based operators still hold significant share | Vietnamese-Australian community is one of the oldest established diaspora groups; trust-based community operator relationships are durable in this corridor. |

| Australia → United Kingdom | Material — high volume driven by Anglo-Australian migration and business flows | Among top 6 outbound corridors | Faster Payments, BACS, bank transfer | High — GBP/AUD is among the most competitive exchange rate corridors globally | FX rate transparency is the primary competitive driver; high-value transfers (property transactions, business) are the margin opportunity. Low-fee digital providers dominate the regular transfer segment. |

| Australia → Pakistan | Growing — Pakistani-Australian diaspora has expanded significantly in recent immigration cohorts | Mid-tier outbound corridor | Bank transfer, JazzCash, EasyPaisa, cash | Medium — compliance complexity reduces competition from non-specialist operators | JazzCash and EasyPaisa mobile wallet integration is the product differentiator. Compliance-capable operators willing to serve this corridor retain good margins due to thinner competition. |

| Australia → Africa (Nigeria, Kenya, Ghana) | Emerging — Nigeria and Kenya corridors expanding rapidly; LemFi entered AU market in Feb 2026 citing this opportunity | Fastest-growing outbound segment by percentage | Bank transfer, mobile money (M-Pesa, OPay, MoMo) | Low-Medium — specialist operators only; established players thin | First-mover advantage still available in AU→Africa. Mobile money integration (M-Pesa, OPay) is essential. High compliance diligence required — but operators who do it correctly face far less competition. |

Figure 3: Australia's top remittance corridors — India and China volumes are independently verified; all other corridor volumes are qualitative assessments based on diaspora size and publicly available immigration data. Competitive assessment and operator insight represent editorial analysis.

The transition from bank-branch and cash-agent remittance to digital platforms is the defining structural story in Australia's remittance market right now. It is not a future trend — it is an ongoing reallocation of volume, customer relationship, and revenue from legacy channels to digital-native operators. The digital segment at US$386.6 million in 2024 will reach US$991.8 million by 2030 at a 17.6% CAGR. Every dollar of that growth represents a transaction that used to go through a bank or cash agent and is now going through a digital platform.

Figure 4: Channel shift in Australian remittances — the five legacy channels losing share and the five digital channels gaining it

One structural accelerant of the digital shift that is specific to Australia is the New Payments Platform (NPP) — Australia's real-time domestic payment infrastructure, launched in 2018. The NPP enables near-instant domestic AUD transfers between bank accounts, and since 2023 has been extended to support incoming international payments, significantly reducing the settlement time for inbound remittances. For outbound digital remittance operators, NPP connectivity means faster collection from sender bank accounts — removing the 1–2 day wait for funds to clear before the international transfer can be initiated. Operators integrated with the NPP deliver a materially faster customer experience than those collecting via traditional BSB/account number bank transfer.

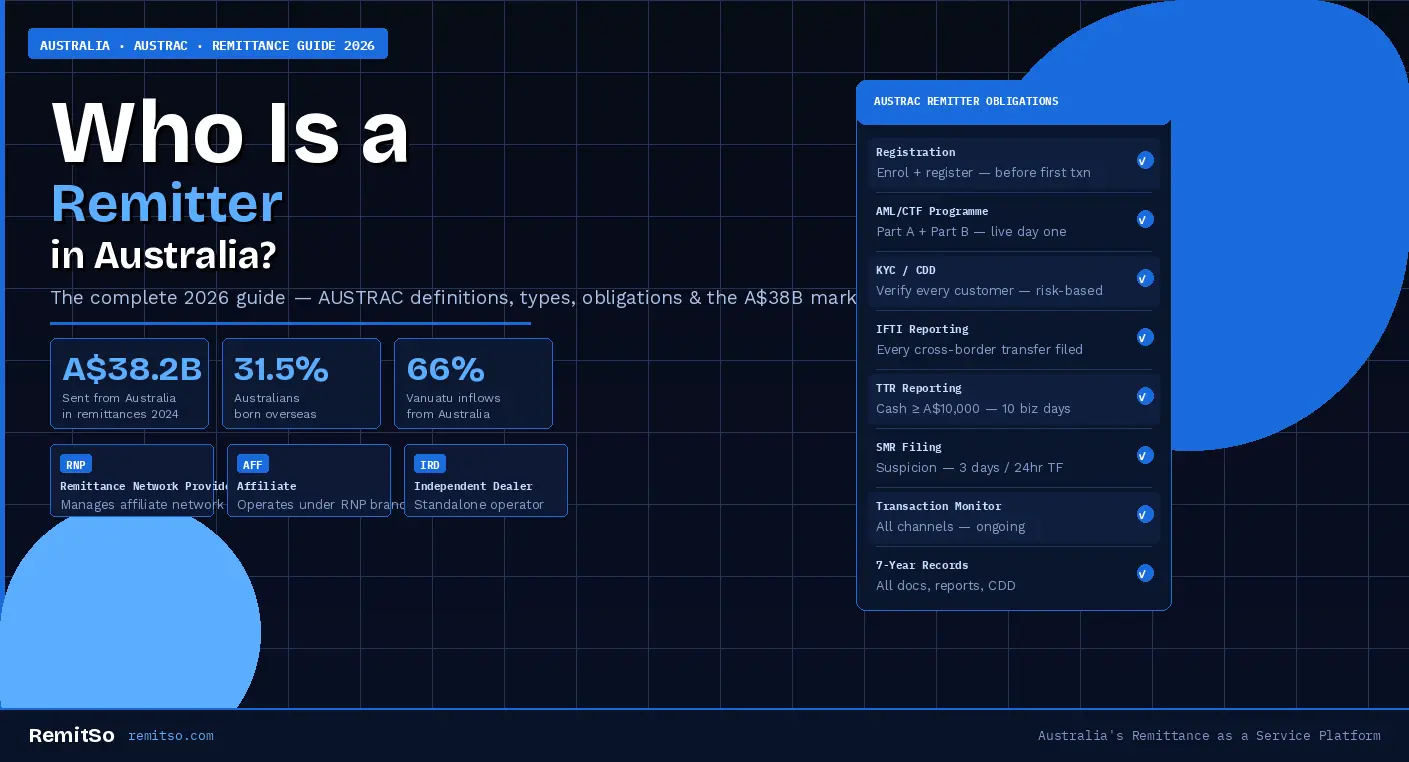

Australia's remittance regulation sits under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006, administered by AUSTRAC. The framework has remained relatively stable in its structure for years, but the AML/CTF Amendment Act 2024 — which came into full effect on 31 March 2026 — introduced the most significant changes to remittance regulation in a decade.

Figure 5: Four key components of Australia's AUSTRAC remittance compliance framework in 2026 — what changed with the AML/CTF Amendment Act and what remains constant

The Australian remittance market has a relatively concentrated competitive structure at the top — a small number of global digital platforms capture a disproportionate share of high-volume corridors — with a much more fragmented mid-tier of community-focused operators serving specific diaspora segments with corridor expertise and personal trust relationships that global platforms cannot easily replicate.

Wise dominates the India, China, UK, and US corridors on price transparency and brand recognition among financially aware migrants. Remitly leads on mobile UX and corridor depth, particularly in the Philippines and South Asian corridors. OFX and TorFX capture high-value transfers, particularly for business and property transactions where customers are willing to pay for FX rate guarantees and personalised service. InstaRem has a strong position with the Singapore-Australian business community and Indian diaspora. WorldRemit and Xoom serve the cash pickup and mobile money payout segments across African and Pacific corridors.

What the global players have not effectively captured is the community trust dimension — the operator whose agents are members of the community they serve, whose platform is localised to the sender's language, and whose customer service is accessible through the channels (WhatsApp, community forums) that the community actually uses. This is the durable competitive moat for smaller operators who choose to serve specific diaspora segments rather than trying to compete across all corridors simultaneously. It is also the reason that new entrants with genuine community distribution — a fintech built for the Filipino-Australian community, an operator with WhatsApp-based customer service for Pakistani-Australian senders — can build meaningful volume without competing directly with Wise on price.

Australia has a specific and documented problem with remittance costs to Pacific Island corridors — a problem that the Australian government's National Remittance Plan has explicitly committed to addressing. The G20 target of reducing average global remittance costs to below 3% and eliminating corridors with costs above 5% by 2030 is a target Australia has formally adopted, but progress toward it in the Pacific corridors specifically has been slow.

| Corridor Category | Typical Fee (Digital Operator) | Typical Fee (Bank Channel) | G20 3% Target Status | Key Driver of Cost |

|---|---|---|---|---|

| Australia → India | 0.3–0.8% total cost | 2.5–4% | ✓ Digital operators already below 3% | High competition has compressed digital margins to near-zero; revenue is volume-driven |

| Australia → China | 0.5–1.2% | 2–4% | ✓ Below 3% for digital | UnionPay settlement costs; compliance overhead for China-specific screening |

| Australia → Philippines | 1–2.5% | 3–6% | ✓/✗ Digital below 3%; bank channel above | Mobile wallet payout integration costs; cash pickup network fees |

| Australia → Pacific Islands | 3–6% | 7–15% | ✗ Still significantly above 3% | Limited banking correspondent relationships; small volume per corridor; de-banking risk for operators serving these corridors |

| Australia → Africa | 2–5% | 6–12% | ✗ Most corridors above 3% | Mobile money settlement complexity; compliance overhead; limited established operator competition |

| Australia → UK / USA | 0.2–0.8% | 1.5–3% | ✓ Well below target | Established major-currency infrastructure; high competition; near-commodity pricing |

Figure 6: Australian remittance cost landscape by corridor — digital operator fees, bank channel fees, and status against the G20 3% cost-reduction target

The cost data reveals a bifurcated market. The major-volume corridors — India, China, UK — have already reached or exceeded the 3% target for digital operators and are effectively price-competed to commodity levels. The underserved corridors — Pacific Islands, Africa, parts of Southeast Asia — remain well above the target, primarily because the operational complexity and compliance overhead of serving these corridors keeps the competitive field thin. For operators who can absorb that complexity — either through sophisticated compliance infrastructure or through a RaaS provider who has already built it — these high-margin corridors represent the most durable revenue opportunity in the Australian remittance market.

For a new operator or an existing operator considering expansion into Australia, the market opportunity is not in the corridors that Wise and Remitly have already optimised. It is in three specific areas of persistent inefficiency that large global platforms are structurally disadvantaged in addressing.

Figure 7: Three operator opportunity areas in the Australian remittance market where structural inefficiency creates durable margin and competitive differentiation

For operators building or expanding a remittance business in Australia, RemitSo's RaaS (Remittance as a Service) platform for Australia provides the compliance infrastructure, technology platform, and payout network that underpin a competitive, regulation-ready operation from Day 1. The platform is built for AUSTRAC compliance — IFTI reporting, AML/CTF programme tooling, 55-indicator transaction monitoring, and sanctions screening across 40,000+ records — so operators can focus on corridor selection, customer acquisition, and community distribution rather than building compliance infrastructure from scratch.

RemitSo operates as a Remittance Network Provider (RNP) in Australia, enabling affiliates to launch under its AUSTRAC registration while maintaining full brand independence. The white-label platform is deployable in weeks, not months, and the payout network covers the major Australian corridors — India, China, Philippines, Vietnam, Pakistan, and emerging African corridors — across bank transfer, mobile money (UPI, GCash, bKash, M-Pesa), and cash pickup delivery methods. Explore the RemitSo Australia RaaS platform →

Need Expert Guidance on Money Transmitter Compliance?

Australia sent A$56.6 billion (approximately US$38.2 billion) overseas in outbound remittances in 2024, according to data reported in conjunction with LemFi's February 2026 Australian market entry announcement. This figure positions Australia among the largest per-capita remittance-sending countries in the world, driven by a migrant population of approximately 8.6 million people — 31.5% of the total population — who maintain strong financial ties with their countries of origin. The formal outbound remittance market (licensed channels) reached US$10.11 billion in 2024, up 28.5% on the prior year, and is forecast to grow at a 16.2% CAGR through 2028 according to ResearchAndMarkets — driven by sustained high net overseas migration and the ongoing shift from bank and cash channels to digital platforms.

India is the largest single recipient of remittances from Australia, receiving approximately US$7.3 billion from Australian senders in 2024 — the highest verified figure for any single corridor. China is the second-largest recipient at US$5.35 billion, reflecting the large Chinese-Australian diaspora population. Together, India and China account for approximately 33% of all outbound remittances from Australia. Other major recipient countries include the Philippines, Vietnam, the United Kingdom, and Pakistan — all among Australia's largest diaspora source countries — though independently verified volume figures for these corridors are not publicly available at the time of publication. The composition of Australia's top remittance corridors closely mirrors the composition of its immigrant source countries: the countries from which most recent migrants have arrived are also the countries to which the most money is sent.

The cheapest way to send money from Australia for most corridors is through a specialist digital remittance platform rather than a bank. For the highest-volume corridors — Australia to India and Australia to China — digital operators like Wise, InstaRem, and Remitly regularly offer total costs (fee plus exchange rate margin) below 1%, compared to 2.5–4% at bank branches. The best rate for any specific corridor at any given moment depends on the operator, the transfer size, and the payout method — bank transfer payouts are typically cheaper than cash pickup. For Pacific Island and African corridors, costs remain higher across all channels due to the limited payout network infrastructure, but digital operators still consistently beat bank rates. Comparing total cost (the amount the recipient actually receives) rather than just the advertised fee is the most accurate way to evaluate different options.

Australia's digital remittance market (online platform segment) is growing at a CAGR of 17.6% from 2025 to 2030, according to Grand View Research. The market generated US$386.6 million in 2024 and is forecast to reach US$991.8 million by 2030. The broader formal outbound remittance market — covering all licensed channels — reached US$10.11 billion in 2024 and is forecast to grow at 16.2% CAGR to US$18.46 billion by 2028, per ResearchAndMarkets. Outward digital remittance is the larger and faster-growing digital segment, accounting for 65.42% of the digital market in 2024. This growth is being driven by three factors: continued high immigration adding new digital-native senders; the ongoing channel shift from bank and cash agent remittance to digital platforms as customers discover the cost and speed advantage; and the integration of mobile wallet payout methods (UPI for India, GCash for the Philippines, M-Pesa for African corridors) that make digital remittance accessible in recipient countries even where traditional banking infrastructure is limited.

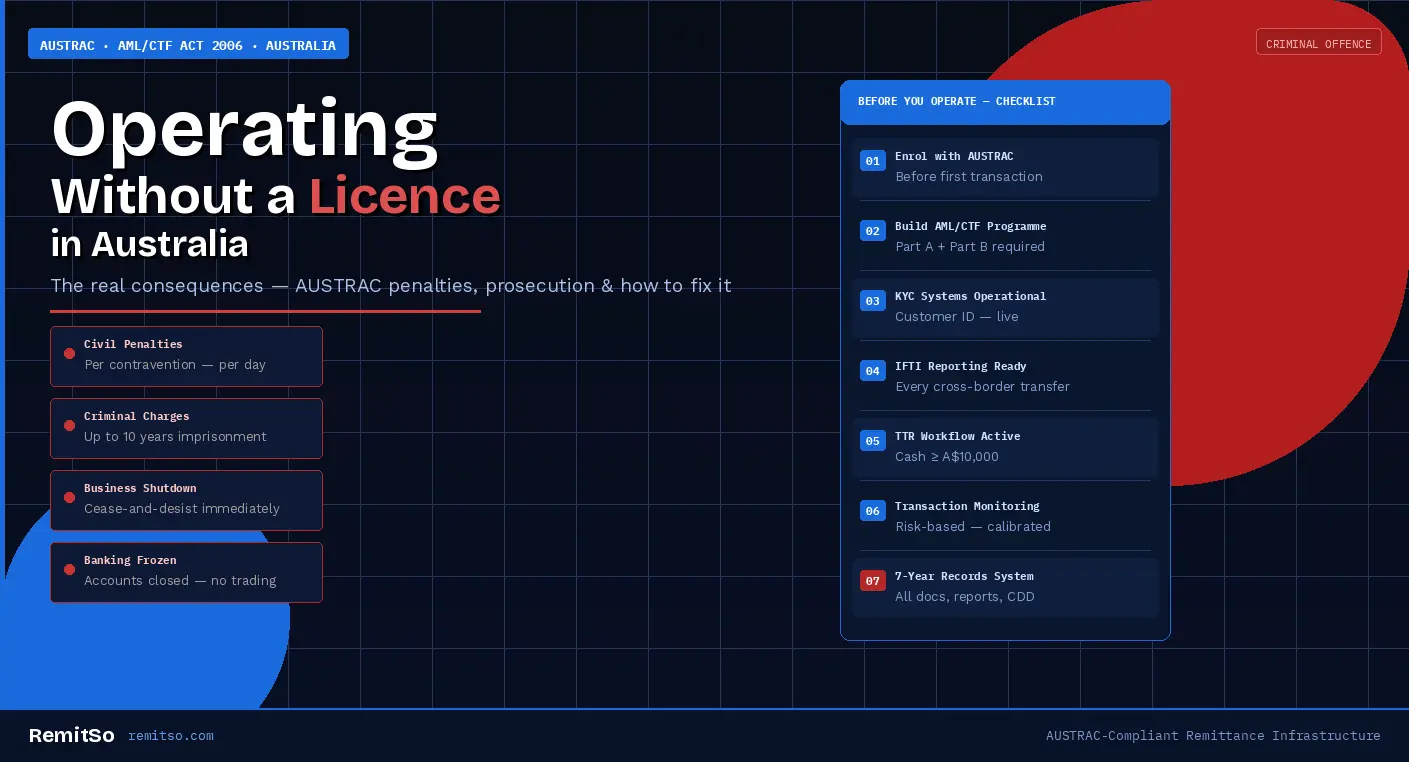

AUSTRAC requires all remittance service providers in Australia to register before providing any remittance services — operating without registration is a criminal offence under the AML/CTF Act with penalties of up to 10 years imprisonment and significant civil fines. Registered operators must maintain a documented AML/CTF Programme (covering both the risk-based systems and controls in Part A, and the customer identification and verification procedures in Part B), report every international funds transfer instruction (IFTI) to AUSTRAC within 10 business days, report cash transactions of A$10,000 or more as Threshold Transaction Reports (TTRs), lodge Suspicious Matter Reports (SMRs) when suspicion is formed, conduct ongoing customer due diligence and transaction monitoring, and retain records for seven years. The AML/CTF Amendment Act 2024, effective 31 March 2026, introduced new registration requirements and safe harbour provisions for reliance on third-party customer due diligence.

Remittance fees on Australian-to-Pacific Island corridors remain among the highest in the world — typically 3–6% for digital operators and 7–15% or more for bank channels — for several structural reasons. Pacific Island banking systems have limited correspondent banking relationships, meaning the international settlement chain is longer and more expensive than for major-currency corridors. Transaction volumes per corridor are relatively small, which means the fixed compliance and operational costs of serving each corridor are spread across fewer transactions. De-banking risk — the risk that correspondent banks will exit relationships with operators serving high-risk corridors — has historically made some financial institutions reluctant to support Pacific Island remittance, reducing competitive pressure on fees. The Australian government has committed to addressing Pacific corridor costs through its National Remittance Plan, including exploring infrastructure-level solutions that could reduce the correspondent banking dependency that drives costs.

The Australian remittance market is served by a mix of global digital platforms, specialist Australian operators, and the major banks. Among digital platforms, Wise (formerly TransferWise) leads on price transparency and brand recognition across major corridors including India, China, and the UK. Remitly has a strong position in mobile-first transfers particularly to the Philippines and South Asian corridors. OFX (formerly OzForex) and TorFX serve the higher-value transfer segment, including business payments and property transactions. InstaRem has a strong position with the Indian-Australian and Singapore-Australian communities. WorldRemit and Western Digital (Xoom) provide cash pickup and mobile wallet payouts in African and Pacific corridors. Among Australian banks, the Big 4 (Commonwealth Bank, Westpac, ANZ, NAB) all offer international transfers but have largely ceded the competitive pricing ground to digital specialists, with fee removal initiatives having failed to recover significant digital market share.

Australia is one of the most commercially attractive remittance markets for new operators in 2026 for several reasons. AUSTRAC's registration-based framework — while rigorous — is faster to navigate than the FCA in the UK or the multi-state MSB licensing system in the US, making regulatory entry achievable within weeks for well-prepared operators using the RNP affiliate model. The market is structurally large (A$56.6B in 2024), growing rapidly (18% CAGR), and demographically driven by sustained high immigration that continuously adds new senders. The underserved corridor opportunity — Pacific Islands, Africa, and emerging diaspora communities — offers margins that the major-corridor competition has eliminated in India and China. And the digital shift, still only capturing a fraction of total outbound volume, means the conversion opportunity is significant. Operators who enter with a compliance-ready platform, a genuine corridor specialisation, and a community-first distribution strategy are entering a market that rewards exactly those qualities.